会计学原理练习题综合Word文档下载推荐.docx

《会计学原理练习题综合Word文档下载推荐.docx》由会员分享,可在线阅读,更多相关《会计学原理练习题综合Word文档下载推荐.docx(99页珍藏版)》请在冰豆网上搜索。

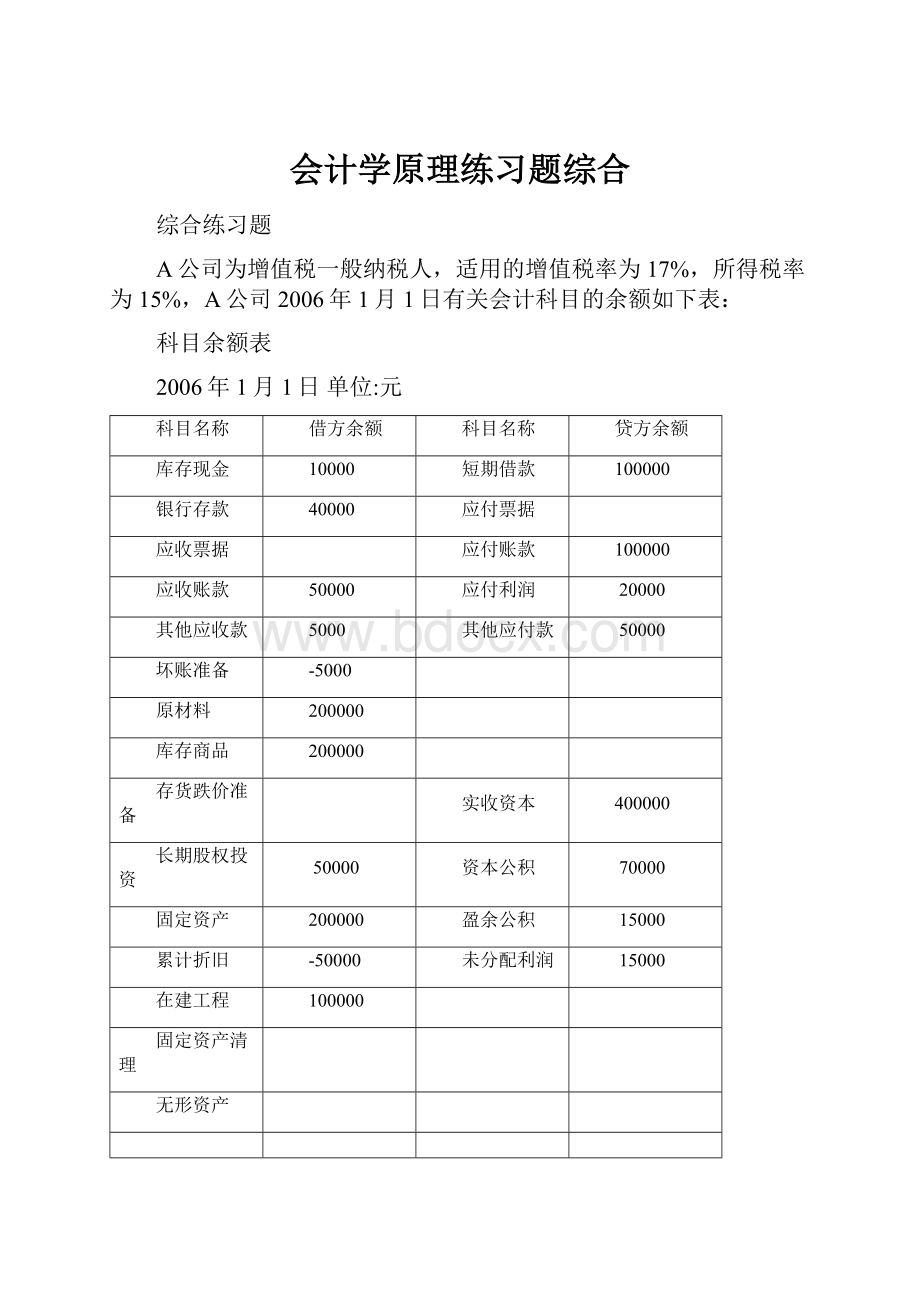

累计折旧

-50000

未分配利润

在建工程

固定资产清理

无形资产

资产合计

800000

负债与所有者权益合计

1.A公司2006年发生的经济业务如下:

(1)从银行取得6个月借款150000元,存入银行。

(2)从银行提取现金50000元备用。

(3)用银行存款偿还短期借款100000元。

(4)销售产品一批,销售价款468000元(含应收取的增值税额),产品实际成本200000元。

产品已发出,货款银行已收300000元,余款未收。

(5)用银行存款支付利息10000元,计入当期损益。

(6)用银行存款支付工资100000元。

其中,销售人员工资20000元;

生产人员工资40000元;

车间管理人员工资20000元;

行政管理人员工资20000元。

代扣代缴个人所得税5000元,用银行存款支付。

(7)用库存现金支付管理费用22490元。

(8)按前述工资总额的8%提取职工福利费,按工资总额的2%提取工会经费。

(9)收到原材料一批,货款(含增值税额)117000元,用银行存款支付100000元,余款未付。

(10)生产领用材料一批,价款200000元。

(11)用银行存款购入一台计算机,价款10000元,已投入使用。

(12)计算本期应交城建税510元。

(13)计提固定资产折旧30000元,其中20000元为生产用固定资产折旧为20000元,其余为管理用固定资产折旧。

(14)用银行存款交纳增值税51000元、城建税510元、企业所得税3000元。

(15)结转制造费用、完工产品生产成本(无期初在产品、本期生产的产品全部完工入库)。

(16)应收账款今年还应计提坏账准备9000元,其他应收款今年还应计提坏账准备1000元(上年末应收账款计提坏账准备5000元,其他应收款未计提坏账准备)。

(17)计提存货跌价准备3000元。

(18)将各项收支结转本年利润。

(19)计算并结转应交所得税。

(20)提取法定盈余公积10000元,提取任意盈余公积5000元。

(21)向股东分配现金股利50000元,其中已用银行存款支付30000元,其他尚未支付。

(22)结转本年净利润,将利润分配各账户余额结转未分配利润明细账户。

2.要求:

根据上述资料编制会计分录。

3.将上述分录过入分类账并计算本期发生额与期末余额。

4.编制2006年12月31日的发生额与余额试算平衡表。

5.编制A公司2006年12月31日的资产负债表和2006年度的利润表。

(1)借:

银行存款150000

贷:

短期借款150000

(2)借:

库存现金50000

银行存款50000

(3)借:

短期借款100000

银行存款100000

(4)借:

银行存款300000

应收账款168000

主营业务收入400000

应交税金——应交增值税(销项税额)68000

借:

主营业务成本200000

库存商品200000

(5)借:

财务费用10000

银行存款10000

(6)借:

应付职工薪酬100000

应交税费——个人所得税5000

银行存款95000

银行存款5000

销售费用20000

生产成本40000

制造费用20000

管理费用20000

(7)借:

管理费用22490

库存现金22490

(8)借:

销售费用2000

生产成本4000

制造费用2000

管理费用2000

应付职工薪酬8000

其他应付款2000

(9)借:

原材料100000

应交税费——应交增值税(进项税额)17000

应付账款17000

(10)借:

生产成本200000

原材料200000

(11)借:

固定资产10000

(12)借:

营业税金及附加510

应交税费——应交城市维护建设税510

(13)借:

管理费用10000

累计折旧30000

(14)借:

应交税费——应交增值税(已交税金)51000

应交税费——应交城市维护建设税510

应交税费——应交所得税3000

银行存款54510

(15)借:

生产成本42000

制造费用42000

库存商品286000

生产成本286000

(16)借:

资产减值损失10000

坏账准备10000

(17)借:

资产减值损失3000

存货跌价准备3000

(18)借:

本年利润400000

本年利润300000

营业税金及附加510

销售费用22000

管理费用54490

财务费用10000

资产减值损失13000

(19)借:

所得税费用15000

应交税费——应交所得税15000

本年利润15000

(20)借:

利润分配——提取法定盈余公积10000

——提取任意盈余公积5000

盈余公积15000

(21)借:

利润分配——应付利润50000

应付利润50000

借:

(22)借:

利润分配——未分配利润65000

——应付利润50000

2006年12月31日单位:

37510

150000

35490

117000

218000

应付职工薪酬

8000

应付股利

40000

-15000

应交税费

42000

52000

286000

-3000

210000

30000

-80000

35000

944000

资产负债表

编制单位:

A公司2006年12月31日单位:

资产

期末数

负债和所有者权益

期末数

流动资产:

流动负债:

货币资金

73000

短期借款

150000

应收账款

203000

应付账款

117000

其他应收款

5000

应付职工薪酬

8000

存货

383000

应交税费

42000

应付利息

流动资产合计

664000

应付股利

40000

非流动资产:

其他应付款

52000

长期股权投资

50000

流动负债合计

409000

长期负债:

长期借款

130000

应付债券

长期应付款

长期负债合计

负债合计

在建工程

100000

所有者权益:

无形资产

400000

资本公积

70000

非流动资产合计

280000

盈余公积

30000

未分配利润

35000

所有者权益合计

535000

资产合计

944000

合计

利润表

A公司2006年12月单位:

项目

本月数

一、营业收入

减:

营业成本

200000

营业税金及附加

510

销售费用

22000

管理费用

54490

财务费用

10000

资产减值损失

13000

加:

投资收益

二、营业利润

营业外收入

营业外支出

三、利润总额

所得税费用

15000

四、净利润

85000

五、每股收益

(一)基本每股收益

(二)稀释每股收益

True/FalseQuestions

1.

Accountingrecordsarealsoreferredtoasthebooks.

TRUE

3.

Preparationofatrialbalanceisthefirststepintheanalyzingandrecordingprocess.

FALSE

4.

Sourcedocumentsprovideevidenceofbusinesstransactionsandarethebasisforaccountingentries.

5.

Itemssuchassalestickets,bankstatements,checks,andpurchaseordersaresourcedocuments.

6.

Anaccountisarecordofincreasesanddecreasesinaspecificasset,liability,equity,revenue,orexpenseitem.

7.

Acustomer'

spromisetopayiscalledanaccountpayabletotheseller.

9.

Asprepaidexpensesareused,theexpiredcostsoftheassetsbecomeexpenses.

10.

Landandbuildingsaregenerallyrecordedinthesameledgeraccount.

FALSe

13.

Cashwithdrawnbytheownerofaproprietorshipshouldbetreatedasanexpenseofthebusiness.

15.

Thechartofaccountsisalistofalltheaccountsusedbyacompanyandincludesanidentificationnumberassignedtoeachaccount.

16.

Anaccountbalanceisthedifferencebetweenthedebitsandcreditsforanaccountincludinganybeginningbalance.

18.

Inadouble-entryaccountingsystem,thetotalamountdebitedmustalwaysequalthetotalamountcredited.

19.

Increasesinliabilityaccountsarerecordedasdebits.

20.

Debitsincreaseassetandexpenseaccounts.

21.

Creditsalwaysincreaseaccountbalances.

FALS

23.

Doubleentryaccountingrequiresthateachtransactionaffect,andberecordedin,atleasttwoaccounts.

24.

Arevenueaccountnormallyhasadebitbalance.

25.

Accountsarenormallydecreasedbydebits.

26.

Theowner'

swithdrawalaccountnormallyhasacreditbalancesinceitisanequityaccount.FALSE

28.

Anowner'

scapitalaccountnormallyhasadebitbalance.

29.

Adebitentryisalwaysfavorable.

30.

Atransactionthatdecreasesanassetaccountandincreasesaliabilityaccountmustalsoaffectoneormoreotheraccounts.

31.

Atransactionthatincreasesanassetanddecreasesaliabilitymustalsoaffectoneormoreotheraccounts.

34.

Ifacompanypurchaseslandpayingcash,thejournalentrytorecordthistransactionwillincludeadebittoCash.

IfacompanyprovidesservicestoacustomeroncreditthesellingcompanyshouldcreditAccountsReceivable.

Whenacompanybillsacustomerfor$600forservicesrendered,thejournalentrytorecordthistransactionwillincludea$600debittoServicesRevenue.

37.

Thedebtratiohelpstoassesstheriskacompanyhasoffailingtopayitsdebtsandishelpfultobothitsownersandcreditors.

38.38.

Thehigheracompany'

sdebtratiois,thehighertheriskofacompanynotbeingabletomeetitsobligations.

Thedebtratioiscalculatedbydividingtotalassetsbytotalliabilities.

FALSE40.

Acompanythatfinancesarelativelylargeportionofitsassetswithliabilitiesissaidtohaveahighdegreeoffinancialleverage.

41.

Ifacompanyishighlyleveraged,thismeansthatithasrelativelylowriskofnotbeingabletorepayitsdebt.

42.

HamiltonIndustrieshasliabilitiesof$105millionandtotalassetsof$350million.Itsdebtratiois40.0%.

FALSE$105million/$350million=30.0%

43.

Highfinancialleverageisalwaysbadforacompany'

sowners.

44.

Acompoundjournalentryaffectsnomorethantwoaccounts.

45.

Postingisthetransferofjournalentryinformationtotheledger.

46.

Transactionsarefirstrecordedintheledger.

47.

Thejournalisknownasabookoforiginalentry.

48.

Ajournalgivesacompleterecordofeachtransactioninoneplace,andshowsthedebitsandcreditsforeachtransaction.

AICPAFN:

DecisionMaking

Difficulty:

Easy

LearningObjective:

C1

49.

Thejournalisknownasthebookoffinalentrybecausefinancialstatementsarepreparedfromit.

Hard

50.

Atrialbalancethatbalancesisnotproofofcompleteaccuracyinrecordingtransactions.

P2

51.

Thetrialbalanceisalistofallaccountsandtheirbalancesatapointintimetakenfromtheledger.

52.

Generally,theorderingofaccountsinatrialbalancetypicallyfollowstheiridentificationnumberfromthechartofaccounts,thatis,assetsfirst,thenliabilities,thenowner'

scapitalandwithdrawals,followedbyrevenuesandexpenses.

AACSB:

Analytic

Medium

53.

Thetrialbalancecanserveasareplacementforthebalancesheet,sincedebitsmustequalwithcredits.

54.

Atrialbalancethatisinbalanceisproofthatnoerrorsweremadeinjournalizingthetransactions,postingtotheledger,andpreparingthetrialbalance.

55.

Ifcashwasincorrectlydebitedfor$100insteadofcorrectlycreditedfor$100,thecashaccountisoutofbalanceby$100.

56.

Thebalancesheetprovidesalinkbetweenbeginningande

升级会员

升级会员