第二章 回归分析.docx

《第二章 回归分析.docx》由会员分享,可在线阅读,更多相关《第二章 回归分析.docx(35页珍藏版)》请在冰豆网上搜索。

第二章回归分析

第二节回归分析

2.1regress命令

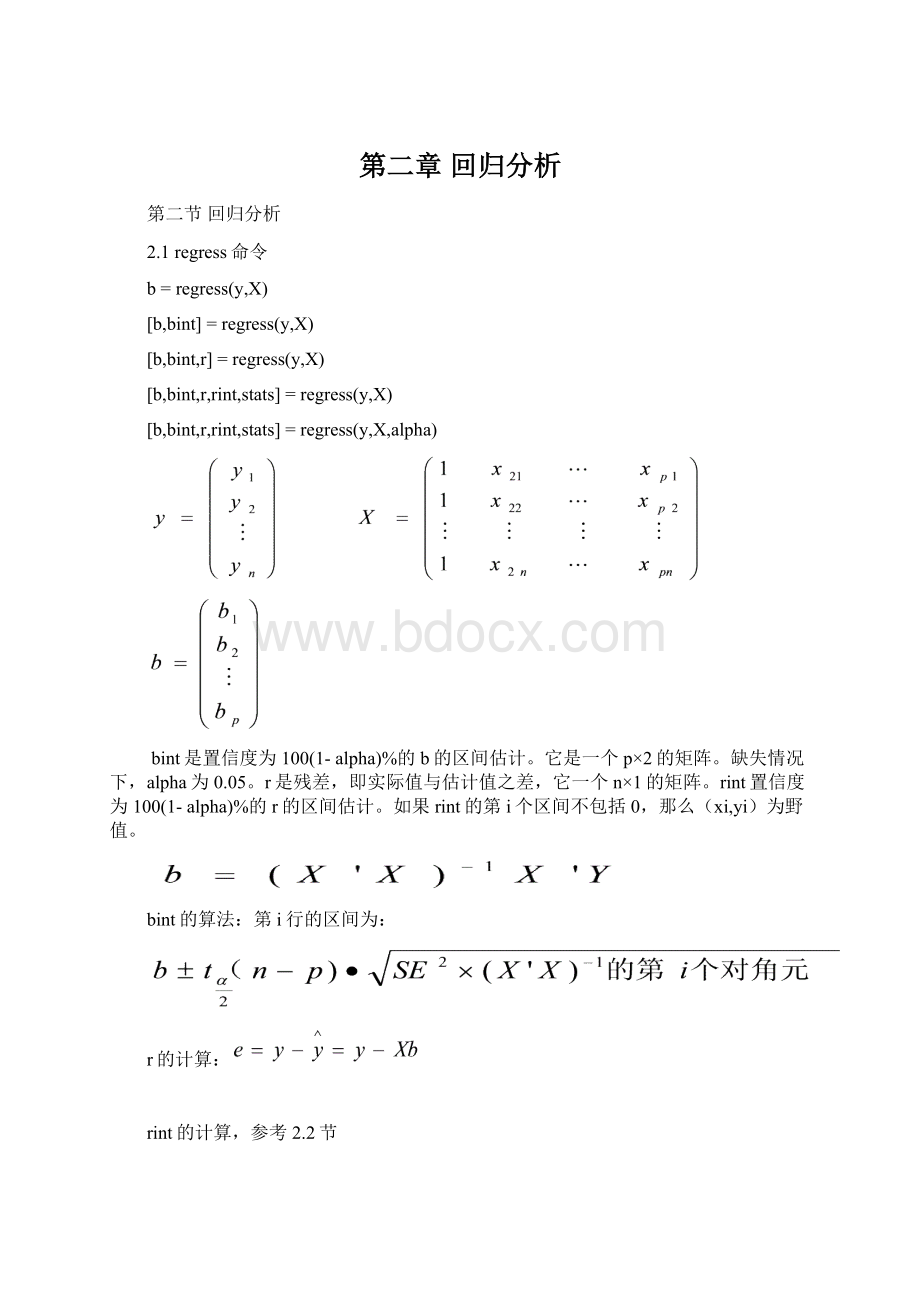

b=regress(y,X)

[b,bint]=regress(y,X)

[b,bint,r]=regress(y,X)

[b,bint,r,rint,stats]=regress(y,X)

[b,bint,r,rint,stats]=regress(y,X,alpha)

bint是置信度为100(1-alpha)%的b的区间估计。

它是一个p×2的矩阵。

缺失情况下,alpha为0.05。

r是残差,即实际值与估计值之差,它一个n×1的矩阵。

rint置信度为100(1-alpha)%的r的区间估计。

如果rint的第i个区间不包括0,那么(xi,yi)为野值。

bint的算法:

第i行的区间为:

r的计算:

rint的计算,参考2.2节

stats包括四项

1、可决系数

2、F值

3、F值对应的p值

注意这里是右侧检验的P值。

4、残差的方差

例子:

年次

1

2

3

4

5

6

7

8

9

10

销售量

Y

百件

10

10

15

13

14

20

18

24

19

23

居民人均收入

X2

百元

5

7

8

9

9

10

10

12

13

15

单价

X3

元

2

3

2

5

4

3

4

3

5

4

z=[10101513142018241923

578991010121315

2325434354];

z1=z';y=z1(:

1);X=[ones(size(z,2),1)z1(:

[2,3])];

[b,bint,r,rint,stats]=regress(y,X,0.05)

b=

4.5875

1.8685

-1.7996

bint=

-1.371310.5463

1.23092.5060

-3.5327-0.0664

r=

-0.3307

-2.2681

-0.9361

0.5941

-0.2054

2.1265

1.9261

2.3896

-0.8797

-2.4162

rint=

-4.09963.4382

-6.18571.6495

-4.98283.1106

-2.93584.1241

-4.77874.3678

-2.05186.3048

-2.37556.2277

-1.16435.9434

-4.90303.1435

-5.12370.2912

stats=

0.879325.50370.00063.8685

下面讨论各值是怎么计算的:

b的计算:

b=inv(X'*X)*X'*y

b=

4.5875

1.8685

-1.7996

r的计算:

r=y-X*b

r=

-0.3307

-2.2681

-0.9361

0.5941

-0.2054

2.1265

1.9261

2.3896

-0.8797

-2.4162

rint的计算:

rint等于:

在本例中:

引用2.2节的studres

studres=

-0.2075

-1.3690

-0.5470

0.3980

-0.1062

1.2035

1.0588

1.5900

-0.5171

-2.1103

rint等于:

rint=[r-tinv(0.975,7)*r./studresr+tinv(0.975,7)*r./studres]

rint=

-4.09963.4382

-6.18571.6495

-4.98283.1106

-2.93584.1241

-4.77874.3678

-2.05186.3048

-2.37556.2277

-1.16435.9434

-4.90303.1435

-5.12370.2912

也可按此计算:

rint=[r-tinv(0.975,7)*sqrt(s2_i).*sqrt(1-leverage)r+tinv(0.975,7)*sqrt(s2_i).*sqrt(1-leverage)]

rint=

-4.09963.4382

-6.18571.6495

-4.98283.1106

-2.93584.1241

-4.77874.3678

-2.05186.3048

-2.37556.2277

-1.16435.9434

-4.90303.1435

-5.12370.2912

SE平方的计算:

sum(r.^2)/7

ans=

3.8685

bint的计算:

bint=[b+tinv(0.975,7)*sqrt(diag(3.8685*inv(X'*X)))b-tinv(0.975,7)*sqrt(diag(3.8685*inv(X'*X)))]

bint=

10.5463-1.3713

2.50601.2309

-0.0664-3.5327

R2的计算:

R2=1-sum(r.^2)/(var(y)*(length(y)-1))

R2=

0.8793

F值的计算:

F=(R2/2)/((1-R2)/(10-3))

F=

25.5037

F值对应的P值

P=1-fcdf(25.5037,2,7)

P=

6.1045e-004

还可绘制残差图

rcoplot(r,rint)

每条线的上下两端对应于rint,中间的圆卷点对应于r。

如果某条线不通过中间的白线(即X轴),那么所对应的(xi,yi)为野值。

这个图中所有线条都通过X轴。

预测:

假设在未来五年,居民人均收入以4.5%的速度递增,而单价以1%的速度递减。

x1

(1)=15;

>>x2

(1)=4;

>>fori=1:

5

x1(i+1)=1.045*x1(i);

x2(i+1)=0.99*x2(i);

y(i+1)=4.5875+1.8685*x1(i+1)-1.7996*x2(i+1);

end

yf=[x1;x2;y]

yf=

Columns1through4

15.000015.675016.380417.1175

4.00003.96003.92043.8812

026.749828.139129.5869

Columns5through6

17.887818.6927

3.84243.8040

31.096132.6693

最后一行为未来五年的预测值(0除外)。

2.2regstats线性回归诊断

2.2.1命令:

regstats(responses,data,model)

responses:

因变量,y它是n×1的列向量。

n为观察值个数。

data:

自变量,它是n×m的矩阵,m为自变量个数,注意它不包括全为1的列向量。

model:

modelcanbeoneofthefollowingstrings

'linear':

Includesconstantandlinearterms(default).包括常数项和各变量。

'interaction':

Includesconstant,linear,andcrossproductterms.如自变量有两个时,X1,X2,则包括常数项、X1,X2,还有X1×X2。

'quadratic':

Includesinteractionsandsquaredterms.如自变量有两个时,X1,X2,则包括常数项、X1,X2,还有X1·X2、X12、X22。

'purequadratic':

Includesconstant,linear,andsquaredterms。

如自变量有两个时,X1,X2,则包括常数项、X1,X2,还有X12、X22。

regstats(responses,data,model)此命令将打开一个用户界面,包括以下20个统计量:

可参见《市场调查与分析》柯惠新丁立宏编著中国统计出版社2000.3第十二章

《统计手册》茆诗松主编科学出版社2003.1第十章

《统计建模与R软件》薛毅陈立萍清华大学出版社2007.4第六章

参考网站:

(1)QRDecomposition(Q)《矩阵论》程云鹏P206

X=Q×R,X包括全为1的列向量。

X为n×p的矩阵。

[Q,R]=qr(X,0)Q是n×p的矩阵,且满足Q'*Q=I

(2)QRDecomposition(R)

[Q,R]=qr(X,0)R是p×p的上三角形矩阵。

(3)RegressionCoefficients

beta=R\(Q'*y)即beta=inv(R)*(Q'*y)

把X=Q×R代入beta=inv(X'*X)*X'*y即得上式。

(4)FittedValuesoftheResponse

=X*beta=X*inv(X'*X)*X'*y

(5)Residuals

(6)MeanSquaredError

(7)CovarianceMatrixofEstimatedCoefficients

(8)Hat(Projection)Matrix(帽子矩阵)

hatmat=Q*Q'yhat=hatmat*y

hatmat为n×n矩阵

将X=Q×R代入yhat=X*beta=X*inv(X'*X)*X'*y得:

yhat=Q*Q'*y

hatmat为投影矩阵。

(9)Leverage(中心化杠杆值)

leverage=diag(hatmat)=diag(Q*Q'),它是n×1的列向量,n个值取值范围为[0,1],第i值是度量第i的观察值在模型中的作用大小,如果第i个值越大,则在模型中的作用越大。

用leverage是寻找强影响点的一个办法。

所谓强影响点是指在模型中的作用特别大的点,就是说删除该点和不删除该点所得到的回归系数会有很差异的点。

理想的中心化杠杆值是每个杠杆值都具有相同的影响力,即所有的杠杆值都接近p/n,如果某个观测点的杠杆值大于等于2p/n,就认为它是一个强影响点。

(10)Delete-1Variance

它是除去第i个数据点后误差的方差的估计。

它是n×1的列向量。

s2_i=((n-p)*mse-r.*r./(1-h))./(n-p-1)

1)nisthenumberofobservations.

2)pisthenumberofunknowncoefficients.

3)mseisthemeansquarederror.

4)risthevectorofresiduals.

5)histheleveragevector.

(11)Delete-1Coefficients

它是把第j个观察值删除后,所得回归系数矩阵。

它为p×n的矩阵,它的第j列对应的列向量是删除第i个观察值所得的回归系数。

b_i(:

j)=beta-Rinv*(Q(j,:

).*r(j)./(1-h(j)))'

1)RinvistheinverseoftheRmatrix.

2)risthevectorofresiduals.

3)histheleveragevector.

(12)StandardizedResiduals

standres=r./sqrt(mse*(1-h))

1)risthevectorofresiduals.

2)mseisthemeansquarederror.

3)histheleveragevector.

Standres为n×1的列向量。

用它可以诊断异常点,异常点是指明显远离主体数据的观察点,表现为标准化残差(内学生化残差)过大的观测量,一般认为标准化残差绝对值大于2或3,则认为是异常点。

经典假设满足时,Standres(i)i=1、2、3…n,可近似看成独立同分布的,均服从标准正态分布

N(0,1)的随机变量。

如果大约有95%的点落在±2内,且没有任何明显的变化趋势,说明回归的基本假定满足,模型对于数据的拟合效果较好。

(13)StudentizedResiduals

studres=r./sqrt(s2_i*(1-h))

1)risthevectorofresiduals.

2)s2_iisthedelete-1variance.

3)histheleveragevector.

studres(i)i=1、2、3…n,经典假设满足时,服从自由度为n-p的t分布。

给定显著性水平

时,

则认为是异常点。

当n-p>30时,一般认为观察值所对应的学生化残差绝对值大于2或3,则认为是异常点。

(14)ScaledChangeinRegressionCoefficients

Thescaledchangeinregressioncoefficientsisap-by-nmatrix.Eachcolumncontainsthescaledchangeintheestimatedcoefficients,beta,causedbydeletingthecorrespondingobservation.

d=sqrt(diag(Rinv*Rinv'));

dfbetas(:

j)=(beta-b_i(:

j))./(sqrt(s2_i(j).*d(j))

1)RinvistheinverseoftheRmatrix.

2)b_iisthematrixofdelete-1coefficients.

3)s2_iisthevectorofdelete-1variances.

它是计算当某个观测点被排除后的回归系数的标准变化值,一般认为标准变化值大于

的点可能就是强影响点。

(15)ChangeinFittedValues

Thechangeinfittedvaluesisann-by-1vector.Eachelementcontainsthechangeinafittedvaluecausedbydeletingthecorrespondingobservation.

dffit=r.*(h./(1-h))

1)risthevectorofresiduals.

2)histheleveragevector.

表示删除某观察值后预测值的变化值。

(16)ScaledChangeinFittedValues

Thescaledchangeinfittedvaluesisann-by-1vector.Eachelementcontainsthechangeinafittedvaluecausedbydeletingthecorrespondingobservation,scaledbythestandarderror.

dffits=studres.*sqrt(h./(1-h))

1)studresisthevectorofstudentizedresiduals.

2)histheleveragevector.

它是计算当某个观察点被排除后的预测值的预测值的标准变化值,一般认为标准变化值的绝对值大于

的点可能就是强影响点。

(17)ChangeinCovariance

covr=1./((((n-p-1+studres.*studres)./(n-p)).^p).*(1-h))

它是n×1的列向量。

1)nisthenumberofobservations.

2)pisthenumberofunknowncoefficients.

3)studresisthevectorofstudentizedresiduals.

4)histheleveragevector.

(18)Cook'sDistance

cookd=r.*r.*(h./(1-h).^2)./(p*mse)risthevectorofresiduals.

1)histheleveragevector.

2)mseisthemeansquarederror.

3)pisthenumberofunknowncoefficients.

cookd是n×1的列向量,如果第i个值大于0.5,则第i个观察值可能为强影响点。

(19)Student'ststatistics

1)beta--Regressioncoefficientestimates

2)se--Standarderrorsfortheregressioncoefficientestimates

3)t--tstatisticsfortheregressioncoefficientestimates,eachoneforatestthatthecorrespondingcoefficientiszero

4)dfe--Degreesoffreedomforerror

5)pval--p-valuesforeachtstatistic,whichiscalculatedbythefollowingcode:

beta=R\(Q'*y)

se=sqrt(diag(covb))

t=beta./se

dfe=n-p

pval=2*(tcdf(-abs(t),dfe))

(20)Fstatistic

1)sse--Errorsumofsquares

2)ssr--Regressionsumofsquares

3)dfe--Errordegreesoffreedom

4)dfr--Regressiondegreesoffreedom

5)f--Fstatisticvalue,foratestthatallregressioncoefficientsotherthantheconstanttermarezero

6)pval--p-valuefortheFstatistic,whichiscalculatedbythefollowingcode:

sse=norm(r).^2

ssr=norm(yfit-mean(yfit)).^2

dfe=n-p

dfr=p-1

f=(ssr/dfr)/(sse/dfe)

pval=1-fcdf(f,dfr,dfe)

例子:

年次

1

2

3

4

5

6

7

8

9

10

销售量

Y

百件

10

10

15

13

14

20

18

24

19

23

居民人均收入

X2

百元

5

7

8

9

9

10

10

12

13

15

单价

X3

元

2

3

2

5

4

3

4

3

5

4

z=[10101513142018241923

578991010121315

2325434354];

z1=z';y=z1(:

1);X=z1(:

[2,3]);

regstats(y,X,'linear')

在用户界面里全部选中得:

Q=

-0.3162-0.5449-0.1902

-0.3162-0.31790.0288

-0.3162-0.2043-0.4207

-0.3162-0.09080.6204

-0.3162-0.09080.2478

-0.31620.0227-0.2017

-0.31620.02270.1710

-0.31620.2497-0.3554

-0.31620.36330.3131

-0.31620.5903-0.2132

R=

-3.1623-30.9903-11.0680

08.80911.8163

002.6835

beta=

4.5875

1.8685

-1.7996

covb=

6.3503-0.3247-0.7947

-0.32470.0727-0.1108

-0.7947-0.11080.5372

yhat=

10.3307

12.2681

15.9361

12.4059

14.2054

17.8735

16.0739

21.6104

19.8797

25.4162

r=

-0.3307

-2.2681

-0.9361

0.5941

-0.2054

2.1265

1.9261

2.3896

-0.8797

-2.4162

mse=

3.8685

leverage=

0.4331

0.2019

0.3187

0.4932

0.1696

0.1412

0.1297

0.2887

0.3300

0.4939

sum(leverage)

ans=

3.0000

hatmat=

Columns1through8

0.43310.26770.29130.03150.10240.12600.05510.0315

0.26770.20190.15280.14670.13600.08700.09770.0104

0.29130.15280.3187-0.14240.01430.18020.02340.1985

0.03150.1467-0.14240.49320.2620-0.02720.2040-0.1

升级会员

升级会员