中级财务会计英文版课后答案chap06.docx

《中级财务会计英文版课后答案chap06.docx》由会员分享,可在线阅读,更多相关《中级财务会计英文版课后答案chap06.docx(10页珍藏版)》请在冰豆网上搜索。

中级财务会计英文版课后答案chap06

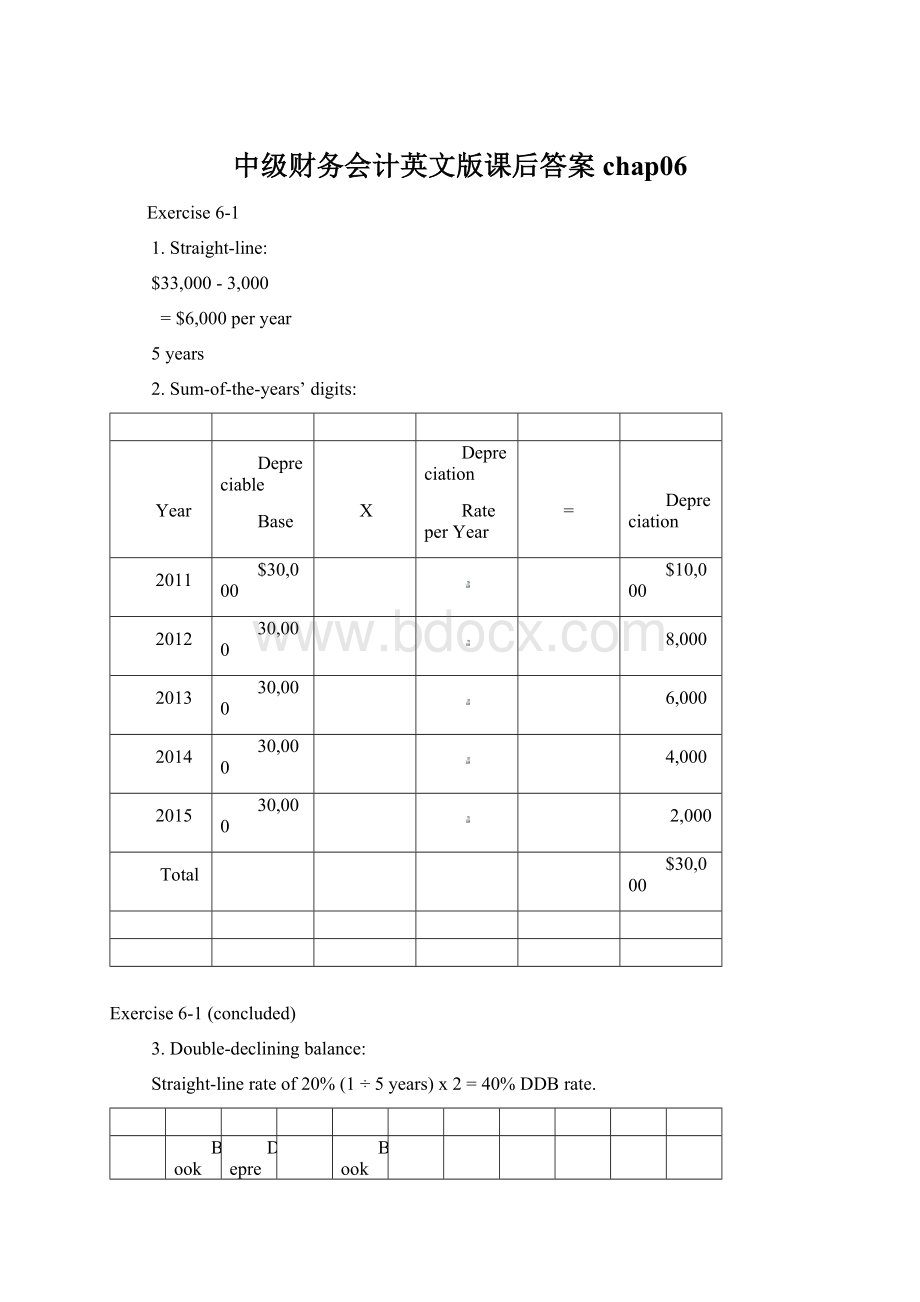

Exercise6-1

1.Straight-line:

$33,000-3,000

=$6,000peryear

5years

2.Sum-of-the-years’digits:

Year

Depreciable

Base

X

Depreciation

RateperYear

=

Depreciation

2011

$30,000

$10,000

2012

30,000

8,000

2013

30,000

6,000

2014

30,000

4,000

2015

30,000

2,000

Total

$30,000

Exercise6-1(concluded)

3.Double-decliningbalance:

Straight-linerateof20%(1÷5years)x2=40%DDBrate.

Year

BookValueBeginning

ofYearX

Depreciation

Rateper

Year=

Depreciation

BookValue

EndofYear

2011

$33,000

40%

$13,200

$19,800

2012

19,800

40%

7,920

11,880

2013

11,880

40%

4,752

7,128

2014

7,128

40%

2,851

4,277

2015

4,277

*

1,277*

3,000

Total

$30,000

*Amountnecessarytoreducebookvaluetoresidualvalue

4.Units-of-production:

$33,000-3,000

=$.30permiledepreciationrate

100,000miles

Year

Actual

Miles

DrivenX

Depreciation

Rateper

Mile=

Depreciation

BookValue

Endof

Year

2011

22,000

$.30

$6,600

$26,400

2012

24,000

.30

7,200

19,200

2013

15,000

.30

4,500

14,700

2014

20,000

.30

6,000

8,700

2015

21,000

*

5,700*

3,000

Totals

102,000

$30,000

*Amountnecessarytoreducebookvaluetoresidualvalue

Exercise6-2

1.Straight-line:

$115,000-5,000

=$11,000peryear

10years

2.Sum-of-the-years’digits:

Sum-of-the-digitsis([10(10+1)]÷2)=55

2011$110,000x10/55=$20,000

2012$110,000x9/55=$18,000

3.Double-decliningbalance:

Straight-linerateis10%(1÷10years)x2=20%DDBrate

2011$115,000x20%=$23,000

2012($115,000-23,000)x20%=$18,400

4.Onehundredfiftypercentdecliningbalance:

Straight-linerateis10%(1÷10years)x1.5=15%rate

2011$115,000x15%=$17,250

2012($115,000-17,250)x15%=$14,663

5.Units-of-production:

$115,000-5,000

=$.50perunitdepreciationrate

220,000units

201130,000unitsx$.50=$15,000

201225,000unitsx$.50=$12,500

Exercise6-3

1.Straight-line:

$115,000-5,000

=$11,000peryear

10years

2011$11,000x3/12=$2,750

2012$11,000x12/12=$11,000

2.Sum-of-the-years’digits:

Sum-of-the-digitsis{[10(10+1)]/2}=55

2011$110,000x10/55x3/12=$5,000

2012$110,000x10/55x9/12=$15,000

+$110,000x9/55x3/12=4,500

$19,500

3.Double-decliningbalance:

Straight-linerateis10%(1÷10years)x2=20%DDBrate

2011$115,000x20%x3/12=$5,750

2012$115,000x20%x9/12=$17,250

+($115,000-23,000)x20%x3/12=4,600

$21,850

or,

2012($115,000-5,750)x20%=$21,850

4.Onehundredfiftypercentdecliningbalance:

Straight-linerateis10%(1÷10years)x1.5=15%rate

2011$115,000x15%x3/12=$4,313

2012$115,000x15%x9/12=$12,937

+($115,000-17,250)x15%x3/12=3,666

$16,603

Or,

2012($115,000-4,313)x15%=$16,603

Exercise6-3(concluded)

5.Units-of-production:

$115,000-5,000

=$.50perunitdepreciationrate

220,000units

201110,000unitsx$.50=$5,000

201225,000unitsx$.50=$12,500

Exercise6-4

Buildingdepreciation:

$5,000,000-200,000

=$160,000peryear

30years

Buildingadditiondepreciation:

RemainingusefullifefromJune30,2011is27.5years.

$1,650,000

=$60,000peryear

27.5years

2011$60,000x6/12=$30,000

2012$60,000x12/12=$60,000

Exercise6-6

Requirement1

1.Straight-line:

$260,000-20,000

=$40,000peryear

6years

2011$40,000x8/12=$26,667

2012$40,000x12/12=$40,000

2.Sum-of-the-years’digits:

Sum-of-the-years’digitsis([6(6+1)]÷2)=21

2011$240,000x6/21x8/12=$45,714

2012$240,000x6/21x4/12=$22,857

+$240,000x5/21x8/12=38,095

$60,952

3.Double-decliningbalance:

1/6(thestraight-linerate)x2=1/3DDBrate

2011$260,000x1/3x8/12=$57,778

2012$260,000x1/3x4/12=$28,889

+($260,000–86,667)x1/3x8/12=38,518

$67,407

or,

2012($260,000–57,778)x1/3=$67,407

Exercise6-9

Requirement1

Asset

Cost

Residual

Value

Depreciable

Base

Estimated

Life(yrs.)

Depreciation

perYear

(straightline)

Stoves

$15,000

$3,000

$12,000

6

$2,000

Refrigerators

10,000

1,000

9,000

5

1,800

Dishwashers

8,000

500

7,500

4

1,875

Totals

$33,000

$4,500

$28,500

$5,675

$5,675

Gr

升级会员

升级会员