hhacct7smch21管理会计.docx

《hhacct7smch21管理会计.docx》由会员分享,可在线阅读,更多相关《hhacct7smch21管理会计.docx(62页珍藏版)》请在冰豆网上搜索。

hhacct7smch21管理会计

Chapter21

Cost-Volume-Profit(CVP)Analysis

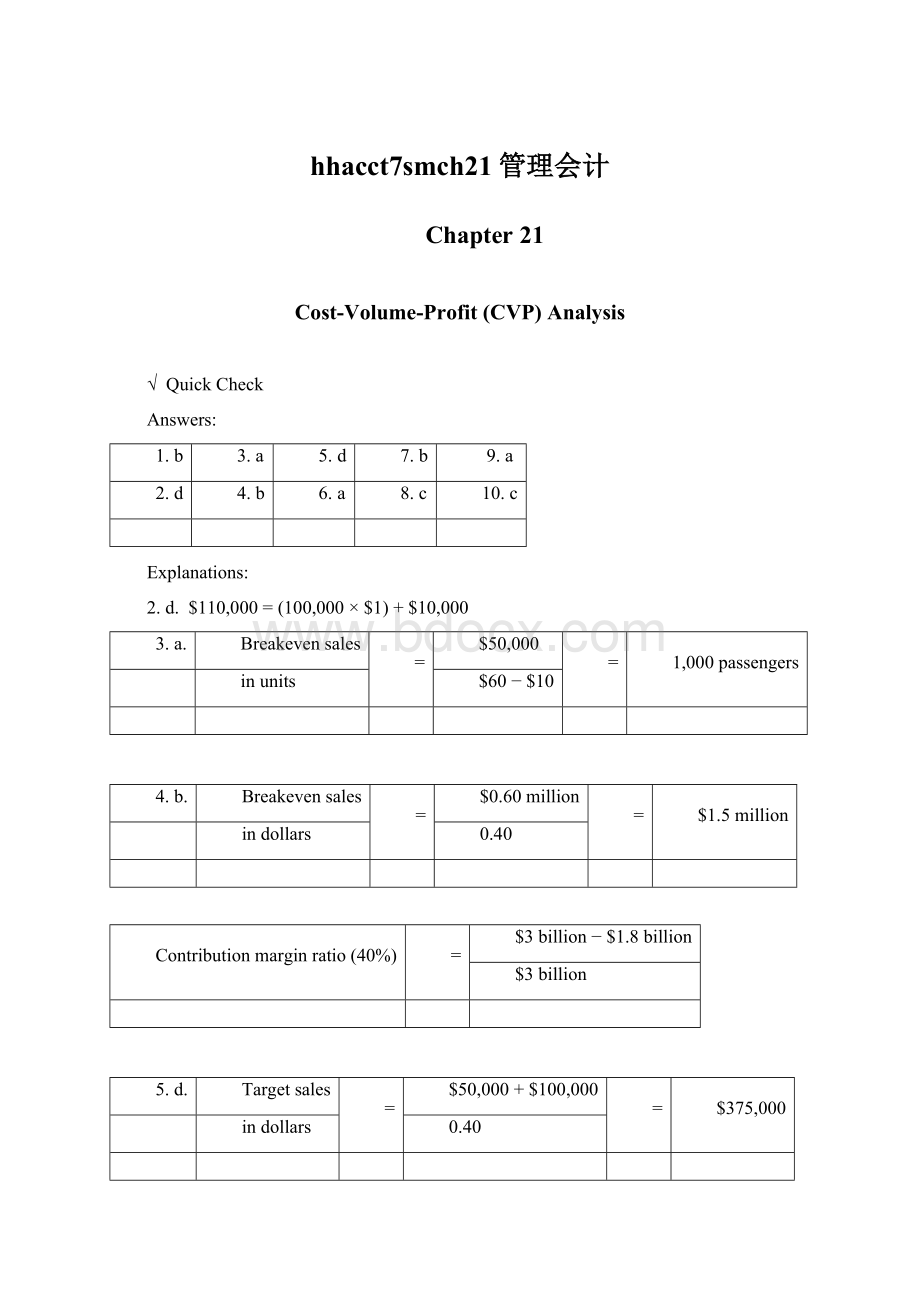

√QuickCheck

Answers:

1.b

3.a

5.d

7.b

9.a

2.d

4.b

6.a

8.c

10.c

Explanations:

2.d.$110,000=(100,000×$1)+$10,000

3.a.

Breakevensales

=

$50,000

=

1,000passengers

inunits

$60−$10

4.b.

Breakevensales

=

$0.60million

=

$1.5million

indollars

0.40

Contributionmarginratio(40%)

=

$3billion−$1.8billion

$3billion

5.d.

Targetsales

=

$50,000+$100,000

=

$375,000

indollars

0.40

Contributionmarginratio(40%)

=

$60−$36

$60

9.a.Marginofsafety($0)=Expectedsales($800,000*)−

breakevensales($800,000)

*($600,000+$700,000+$900,000+$800,000+$1,000,000)/5=$800,000

10.c.

Breakevensales

=

$50,000

=

1,250passengers

intotalunits

$40*

625regular

625discount

*Weighted-average

=

($60−$10)+($40−$10)

=

$40

contributionmargin

2

perunit

√ShortExercises

(5-10min.)S21-1

F

1.Depreciationonroutersusedtocutwoodenclosures

V

2.Woodforspeakerenclosures

F

3.Patentsoncrossoverrelays

V

4.Crossoverrelays

V

5.Grillcloth

V

6.Glue

F

7.Qualityinspector’ssalary

(5-10min.)S21-2

F

1.Buildingrent

F

2.Toys

F

3.Playgroundequipment

V

4.Afternoonsnacks

F

5.Sally’ssalary

V

6.Wagesofafter-schoolemployees

V

7.Drawingpaper

F

8.Tablesandchairs

(5-10min.)S21-3

Req.1

a.Callfor20minutes

$5.00+(20×$0.35)

$5.00+$7.00=$12.00

b.Callfor40minutes

$5.00+(40×$0.35)

$5.00+$14.00=$19.00

c.Callfor80minutes

$5.00+(80×$0.35)

$5.00+$28.00=$33.00

(continued)S21-3

Req.2

(5-10min.)S21-4

Req.1

Variablecostperunit

=

Changeintotalcost÷Changein

volumeofactivity

=

($2,400−$2,200)÷(1,000machine

hours−500machinehours)

=

$200÷500hours=$.40permachine

hour

Req.2

Totalfixedcost

=

Totalmixedcost−Totalvariablecost

=

$2,400−($.40×1,000machinehours)

=

$2,400−$400=$2,000

Inthisexamplethehighestcostandvolumewerechosentocalculatethetotalfixedcost,butthelowestcostandvolumealsocouldbeusedtocalculatethe$2,000totalfixedcost:

Totalfixedcost

=

Totalmixedcost−Totalvariablecost

=

$2,200−($.40×500machinehours)

=

$2,200−$200=$2,000

(5-10min.)S21-5

Incomestatementapproach:

Salesrevenue

−

Variablecosts

−

Fixed

=

Operating

costs

income

SalepriceUnits

perunit×sold

−

VariablecostUnits

−

Fixed

=

Operating

perunit×sold

costs

income

($60×Unitssold)

−

($20×Unitssold)

−

$275,000

=

$0

($60−$20)×Unitssold

−

$275,000

=

$0

$40

×

Unitssold

=

$275,000

Unitssold

=

6,875tickets

Alternative:

Shortcutcontributionmarginapproach:

Unitssold

=

Fixedcosts+Operatingincome

(tobreakeven)

Contributionmarginperunit

=

$275,000+0

$40*

=

6,875tickets

*Contributionmargin

=

$60sale

−

$20variablecost

perperson

price

perperson

Proof:

Salesrevenue(6,875×$60)................................…..

$412,500

Variablecosts(6,875×$20)........................…..........

137,500

Contributionmargin............................................…..

275,000

Fixedcosts........................................…………..........

(275,000)

Operatingincome......................................……….…

$0

(continuesS21-4)(5min.)S21-6

Req.1

Contributionmarginratio

Contributionmarginperperson

=

$40*

Salepriceperperson

$60

=

0.66667

*Saleprice($60)minusvariablecostperperson($20)

Req.2

Breakeven

=

Fixedcosts+Operatingincome

salesindollars

Contributionmarginratio

=

$275,000+$0

0.66667

=

$412,500

(10min.)S21-7

Req.1

Salesrevenue

−

Variablecosts

−

Fixed

=

Operating

costs

income

SalepriceUnits

perunit×sold

−

VariablecostUnits

−

Fixed

=

Operating

perunit×sold

costs

income

($50×Unitssold)

−

($20×Unitssold)

−

$275,000

=

$0

($50−$20)×Unitssold

−

$275,000

=

$0

$30

×

Unitssold

=

$275,000

Unitssold

=

9,167tickets

9,167tickets×$50=$458,350

Reducingthesalepriceincreasesthebreakevenpoint.

Alternatively,

Contribution

=

Contributionmarginperunit

marginrat

升级会员

升级会员