中级计量经济学第四章习题以及解答思路EViews.docx

《中级计量经济学第四章习题以及解答思路EViews.docx》由会员分享,可在线阅读,更多相关《中级计量经济学第四章习题以及解答思路EViews.docx(20页珍藏版)》请在冰豆网上搜索。

中级计量经济学第四章习题以及解答思路EViews

第4章

习题一

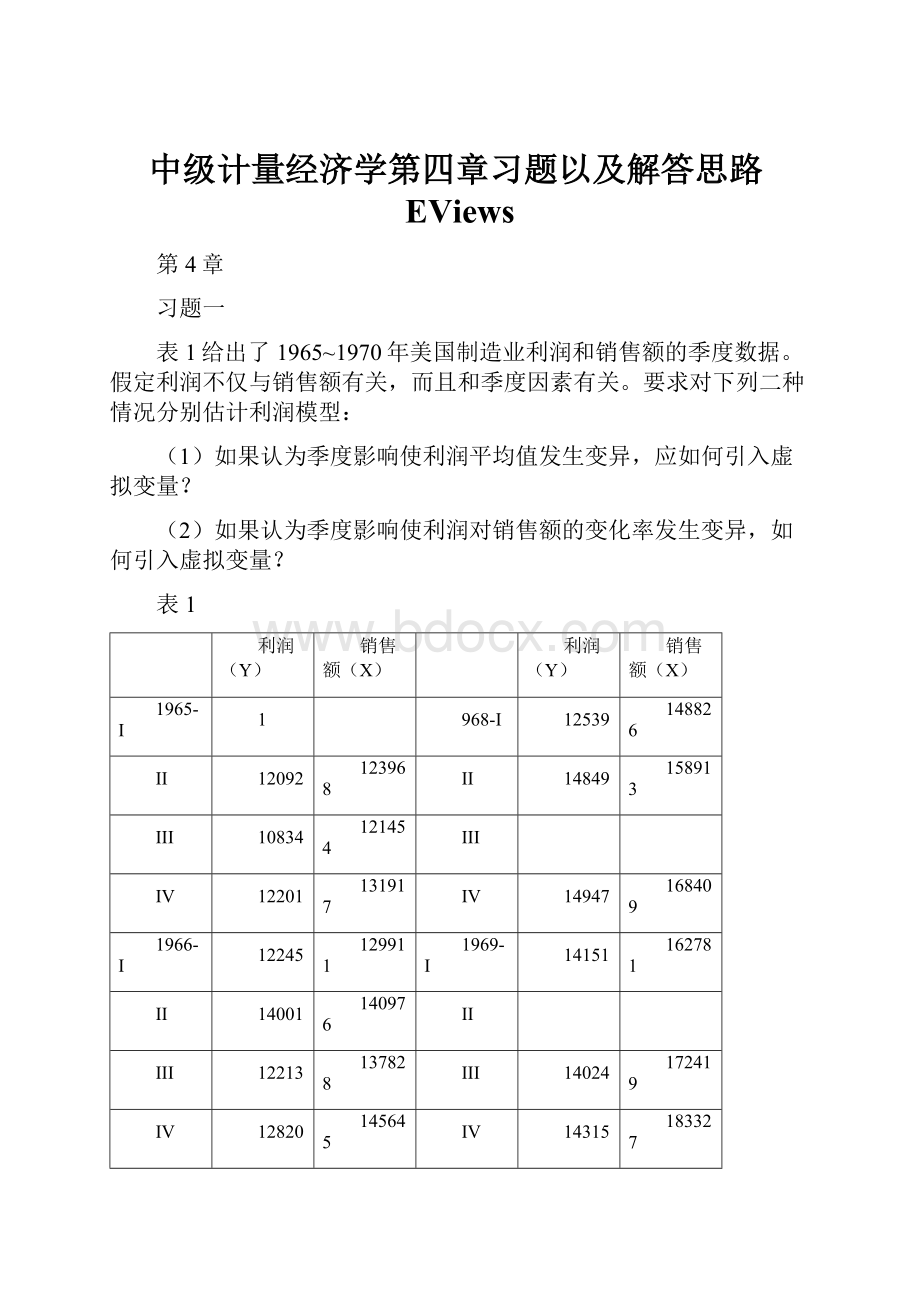

表1给出了1965~1970年美国制造业利润和销售额的季度数据。

假定利润不仅与销售额有关,而且和季度因素有关。

要求对下列二种情况分别估计利润模型:

(1)如果认为季度影响使利润平均值发生变异,应如何引入虚拟变量?

(2)如果认为季度影响使利润对销售额的变化率发生变异,如何引入虚拟变量?

表1

利润(Y)

销售额(X)

利润(Y)

销售额(X)

1965-I

1

968-I

12539

148826

II

12092

123968

II

14849

158913

III

10834

121454

III

IV

12201

131917

IV

14947

168409

1966-I

12245

129911

1969-I

14151

162781

II

14001

140976

II

III

12213

137828

III

14024

172419

IV

12820

145645

IV

14315

183327

1967-I

1

970-I

12381

170415

II

12615

145126

II

III

11014

141536

III

12174

176712

IV

12730

151776

IV

10985

180370

Quarterly65-70

Quick-EquationEstimation

Ycx@seas

(1)@seas

(2)@seas(3)

DependentVariable:

Y

Method:

LeastSquares

Date:

11/26/14Time:

18:

38

Sample:

1965Q11970Q4

Includedobservations:

24

Variable

Coefficient

Std.Error

t-Statistic

Prob.

C

6868.015

1892.766

3.628559

0.0018

X

0.038265

0.011483

3.332252

0.0035

@SEAS

(1)

-182.1690

654.3568

-0.278394

0.7837

@SEAS

(2)

1140.294

630.6806

1.808038

0.0865

@SEAS(3)

-400.3371

636.1128

-0.629349

0.5366

R-squared

0.525596

Meandependentvar

12838.54

AdjustedR-squared

0.425721

S.D.dependentvar

1433.284

S.E.ofregression

1086.160

Akaikeinfocriterion

17.00174

Sumsquaredresid

Schwarzcriterion

17.24716

Loglikelihood

-199.0208

F-statistic

5.262563

Durbin-Watsonstat

0.388380

Prob(F-statistic)

0.005024

T和P在5%情况下都不通过,第二季度相对还好一点

假设第二季度显著,结果的经济含义是什么?

Ycx@seas

(2)@seas(3)@seas(4)

DependentVariable:

Y

Method:

LeastSquares

Date:

11/26/14Time:

18:

47

Sample:

1965Q11970Q4

Includedobservations:

24

Variable

Coefficient

Std.Error

t-Statistic

Prob.

C

6685.846

1711.618

3.906155

0.0009

X

0.038265

0.011483

3.332252

0.0035

@SEAS

(2)

1322.463

638.4258

2.071444

0.0522

@SEAS(3)

-218.1681

632.1991

-0.345094

0.7338

@SEAS(4)

182.1690

654.3568

0.278394

0.7837

R-squared

0.525596

Meandependentvar

12838.54

AdjustedR-squared

0.425721

S.D.dependentvar

1433.284

S.E.ofregression

1086.160

Akaikeinfocriterion

17.00174

Sumsquaredresid

Schwarzcriterion

17.24716

Loglikelihood

-199.0208

F-statistic

5.262563

Durbin-Watsonstat

0.388380

Prob(F-statistic)

0.005024

第二季度依旧显著影响

四种都试一下(去掉一个季节),选一个最显著的

124

DependentVariable:

Y

Method:

LeastSquares

Date:

11/26/14Time:

18:

51

Sample:

1965Q11970Q4

Includedobservations:

24

Variable

Coefficient

Std.Error

t-Statistic

Prob.

C

6467.678

1789.178

3.614888

0.0018

X

0.038265

0.011483

3.332252

0.0035

@SEAS

(1)

218.1681

632.1991

0.345094

0.7338

@SEAS

(2)

1540.632

628.3419

2.451900

0.0241

@SEAS(4)

400.3371

636.1128

0.629349

0.5366

R-squared

0.525596

Meandependentvar

12838.54

AdjustedR-squared

0.425721

S.D.dependentvar

1433.284

S.E.ofregression

1086.160

Akaikeinfocriterion

17.00174

Sumsquaredresid

Schwarzcriterion

17.24716

Loglikelihood

-199.0208

F-statistic

5.262563

Durbin-Watsonstat

0.388380

Prob(F-statistic)

0.005024

134

DependentVariable:

Y

Method:

LeastSquares

Date:

11/26/14Time:

18:

52

Sample:

1965Q11970Q4

Includedobservations:

24

Variable

Coefficient

Std.Error

t-Statistic

Prob.

C

8008.309

1827.543

4.382009

0.0003

X

0.038265

0.011483

3.332252

0.0035

@SEAS

(1)

-1322.463

638.4258

-2.071444

0.0522

@SEAS(3)

-1540.632

628.3419

-2.451900

0.0241

@SEAS(4)

-1140.294

630.6806

-1.808038

0.0865

R-squared

0.525596

Meandependentvar

12838.54

AdjustedR-squared

0.425721

S.D.dependentvar

1433.284

S.E.ofregression

1086.160

Akaikeinfocriterion

17.00174

Sumsquaredresid

Schwarzcriterion

17.24716

Loglikelihood

-199.0208

F-statistic

5.262563

Durbin-Watsonstat

0.388380

Prob(F-statistic)

0.005024

(2)

Y=c+βx+α1D1X+α2D2X+α3D3X

D1=1(第一季度)0(其他)

Ycx@seas

(1)*x@seas

(2)*x@seas(3)*x

DependentVariable:

Y

Method:

LeastSquares

Date:

11/26/14Time:

19:

00

Sample:

1965Q11970Q4

Includedobservations:

24

Variable

Coefficient

Std.Error

t-Statistic

Prob.

C

6965.852

1753.642

3.972220

0.0008

X

0.037363

0.011139

3.354215

0.0033

@SEAS

(1)*X

-0.000893

0.004259

-0.209588

0.8362

@SEAS

(2)*X

0.007712

0.003962

1.946502

0.0665

@SEAS(3)*X

-0.002291

0.004041

-0.566985

0.5774

R-squared

0.528942

Meandependentvar

12838.54

AdjustedR-squared

0.429771

S.D.dependentvar

1433.284

S.E.ofregression

1082.323

Akaikeinfocriterion

16.99466

Sumsquaredresid

Schwarzcriterion

17.24009

Loglikelihood

-198.9359

F-statistic

5.333675

Durbin-Watsonstat

0.418713

Prob(F-statistic)

0.004722

DependentVariable:

Y

Method:

LeastSquares

Date:

11/26/14Time:

19:

10

Sample:

1965Q11970Q4

Includedobservations:

24

Variable

Coefficient

Std.Error

t-Statistic

Prob.

C

8008.309

1827.543

4.382009

0.0003

X

0.038265

0.011483

3.332252

0.0035

@SEAS

(1)

-1322.463

638.4258

-2.071444

0.0522

@SEAS(3)

-1540.632

628.3419

-2.451900

0.0241

@SEAS(4)

-1140.294

630.6806

-1.808038

0.0865

R-squared

0.525596

Meandependentvar

12838.54

AdjustedR-squared

0.425721

S.D.dependentvar

1433.284

S.E.ofregression

1086.160

Akaikeinfocriterion

17.00174

Sumsquaredresid

Schwarzcriterion

17.24716

Loglikelihood

-199.0208

F-statistic

5.262563

Durbin-Watsonstat

0.388380

Prob(F-statistic)

0.005024

DependentVariable:

Y

Method:

LeastSquares

Date:

11/26/14Time:

19:

11

Sample:

1965Q11970Q4

Includedobservations:

24

Variable

Coefficient

Std.Error

t-Statistic

Prob.

C

6965.852

1753.642

3.972220

0.0008

X

0.035072

0.011790

2.974675

0.0078

@SEAS

(1)*X

0.001398

0.004241

0.329736

0.7452

@SEAS

(2)*X

0.010003

0.004068

2.458823

0.0237

@SEAS(4)*X

0.002291

0.004041

0.566985

0.5774

R-squared

0.528942

Meandependentvar

12838.54

AdjustedR-squared

0.429771

S.D.dependentvar

1433.284

S.E.ofregression

1082.323

Akaikeinfocriterion

16.99466

Sumsquaredresid

Schwarzcriterion

17.24009

Loglikelihood

-198.9359

F-statistic

5.333675

Durbin-Watsonstat

0.418713

Prob(F-statistic)

0.004722

DependentVariable:

Y

Method:

LeastSquares

Date:

11/26/14Time:

19:

11

Sample:

1965Q11970Q4

Includedobservations:

24

Variable

Coefficient

Std.Error

t-Statistic

Prob.

C

6965.852

1753.642

3.972220

0.0008

X

0.036471

0.012353

2.952415

0.0082

@SEAS

(2)*X

0.008604

0.004237

2.030539

0.0565

@SEAS(3)*X

-0.001398

0.004241

-0.329736

0.7452

@SEAS(4)*X

0.000893

0.004259

0.209588

0.8362

R-squared

0.528942

Meandependentvar

12838.54

AdjustedR-squared

0.429771

S.D.dependentvar

1433.284

S.E.ofregression

1082.323

Akaikeinfocriterion

16.99466

Sumsquaredresid

Schwarzcriterion

17.24009

Loglikelihood

-198.9359

F-statistic

5.333675

Durbin-Watsonstat

0.418713

Prob(F-statistic)

0.004722

习题二

表2给出了某地区某行业的库存

和销售

的统计资料。

假设库存额依赖于本年销售额与前三年的销售额,试用Almon变换估计以下有限分布滞后模型:

表2

库存Y

(万元)

销售额X

(万元)

库存Y

(万元)

销售额X

(万元)

1980

11267

8827

1990

17053

13668

1981

12661

9247

1991

19491

14956

1982

12968

9579

1992

21164

15483

1983

12518

9

9

16761

1984

13177

10

9

17852

1985

13454

10265

1995

25411

17620

1986

13735

10299

1996

25611

18639

1987

14553

11

0

20672

1988

15011

11677

1998

30218

23799

1989

15846

12445

1999

36784

27359

Y=α+α0ΣXt-i+α1ΣXt-i+α2ΣXt-i+μt

↑3,i=0笔记11,26)

在最上面输入

genrz0=x+x(-1)+x(-1)+x(-3)

genrz1=x(-1)+2*x(-2)+3*x(-3)

genrz2=x(-1)+4*x(-2)+9*x(-3)

ycz0z1z2

DependentVariable:

Y

Method:

LeastSquares

Date:

11/26/14Time:

19:

38

Sample(adjusted):

19831999

Includedobservations:

17afteradjustments

Variable

Coefficient

Std.Error

t-Statistic

Prob.

C

-1928.495

503.5272

-3.829972

0.0021

Z0

0.344027

0.091848

3.745615

0.0024

Z1

0.815758

0.351519

2.320667

0.0372

Z2

-0.339041

0.128632

-2.635739

0.0206

R-squared

0.996564

Meandependentvar

20467.29

AdjustedR-squared

0.995771

S.D.dependentvar

6997.995

S.E.ofregression

455.0907

Akaikeinfocriterion

15.28119

Sumsquaredresid

2692398.

Schwarzcriterion

15.47724

Loglikelihood

-125.8902

F-statistic

1256.768

Durbin-Watsonstat

1.985515

Prob(F-statistic)

0.000000

YcPDL(x,3,2)

重新回归

DependentVariable:

Y

Method:

LeastSquares

Date:

11/26/14Time:

19:

46

Sample(adjusted):

19831999

Includedobservations:

17afteradjustments

Variable

Coefficient

Std.Error

t-Statistic

Prob.

C

-1784.821

498.4654

-3.5806

升级会员

升级会员