chap020ise.docx

《chap020ise.docx》由会员分享,可在线阅读,更多相关《chap020ise.docx(21页珍藏版)》请在冰豆网上搜索。

chap020ise

CHAPTER20:

OPTIONSMARKETS:

INTRODUCTION

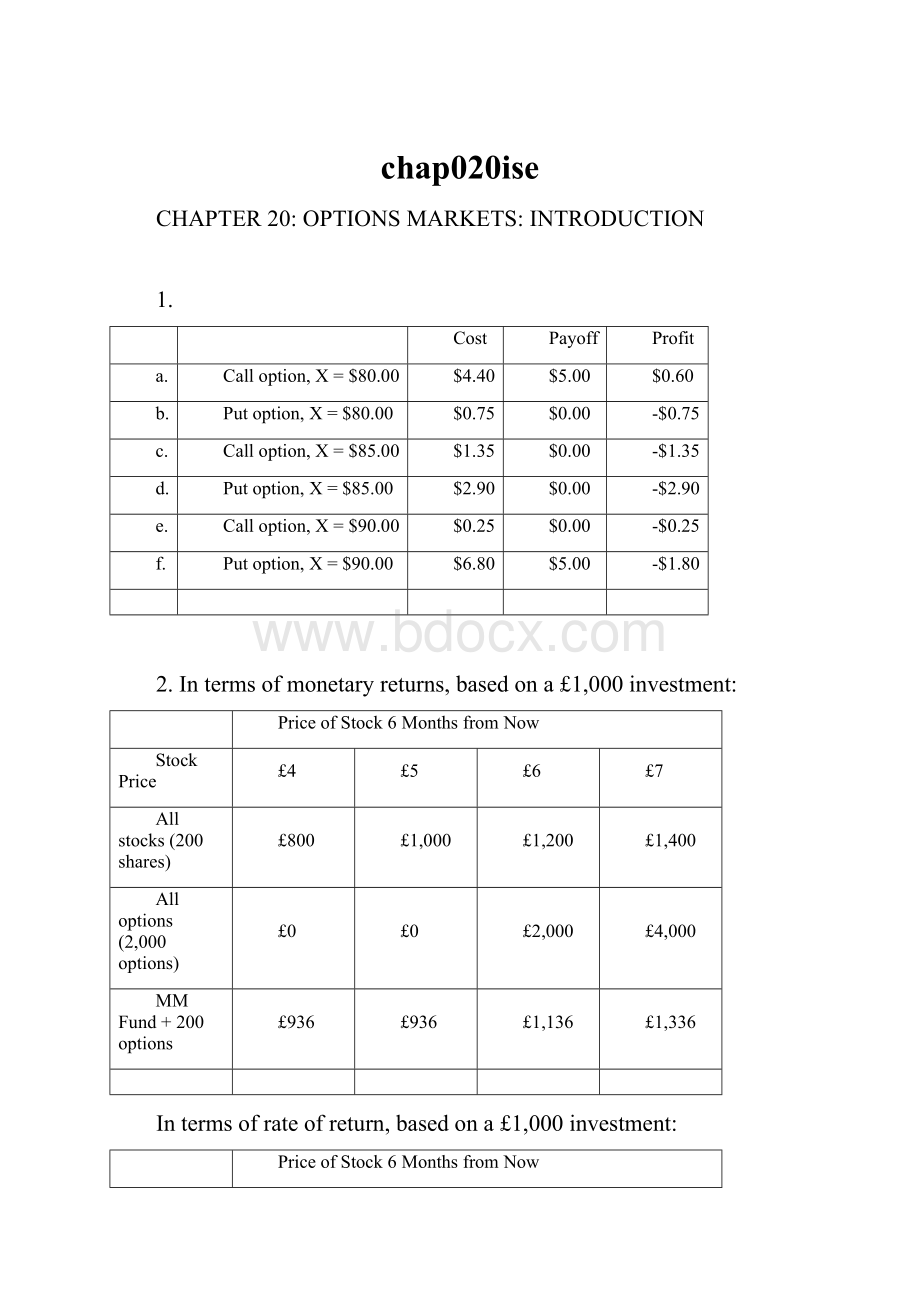

1.

Cost

Payoff

Profit

a.

Calloption,X=$80.00

$4.40

$5.00

$0.60

b.

Putoption,X=$80.00

$0.75

$0.00

-$0.75

c.

Calloption,X=$85.00

$1.35

$0.00

-$1.35

d.

Putoption,X=$85.00

$2.90

$0.00

-$2.90

e.

Calloption,X=$90.00

$0.25

$0.00

-$0.25

f.

Putoption,X=$90.00

$6.80

$5.00

-$1.80

2.Intermsofmonetaryreturns,basedona£1,000investment:

PriceofStock6MonthsfromNow

StockPrice

£4

£5

£6

£7

Allstocks(200shares)

£800

£1,000

£1,200

£1,400

Alloptions(2,000options)

£0

£0

£2,000

£4,000

MMFund+200options

£936

£936

£1,136

£1,336

Intermsofrateofreturn,basedona£1,000investment:

PriceofStock6MonthsfromNow

StockPrice

£4

£5

£6

£7

Allstocks(200shares)

-20%

0%

20%

40%

Alloptions(2,000options)

-100%

-100%

100%

300%

MMFund+200options

-6.4%

-6.4%

13.6%

33.6%

3.a.Fromput-callparity:

P=C–S0+[X/(1+rf)T]=2–20+[20/(1.10)1/4]=C$1.53

b.Purchaseastraddle,i.e.,bothaputandacallonthestock.Thetotalcostofthestraddleis:

C$2+C$1.53=C$3.53

Thisistheamountbywhichthestockwouldhavetomoveineitherdirectionfortheprofitonthecallorputtocovertheinvestmentcost(notincludingtimevalueofmoneyconsiderations).Accountingfortimevalue,thestockpricewouldhavetomoveineitherdirectionby:

C$3.53⨯1.101/4=C$3.62

4.a.Fromput-callparity:

C=P+S0–[X/(l+rf)T]=560+7,000–[7,000/(1.10)1/4]=¥724.82

b.Sellastraddle,i.e.,sellacallandaputtorealizepremiumincomeof:

¥724.82+¥560=¥1,284.82

Ifthestockendsupat¥7,000,bothoftheoptionswillbeworthlessandyourprofitwillbe¥1,284.82.Thisisyourmaximumpossibleprofitsince,atanyotherstockprice,youwillhavetopayoffoneitherthecallortheput.Thestockpricecanmoveby¥1,284.82ineitherdirectionbeforeyourprofitsbecomenegative.

c.Buythecall,sell(write)theput,lend:

¥7,000/(1.10)1/4

Thepayoffisasfollows:

Position

ImmediateCF

CFin3months

ST≤X

ST>X

Call(long)

C=724.82

0

ST–7,000

Put(short)

–P=560.00

–(7,000–ST)

0

Lendingposition

7,000

7,000

Total

C–P+

ST

ST

Bytheput-callparitytheorem,theinitialoutlayequalsthestockprice:

S0=¥7,000

Ineitherscenario,youendupwiththesamepayoffasyouwouldifyouboughtthestockitself.

5.a.

Outcome

ST≤X

ST>X

Stock

ST+D

ST+D

Put

X–ST

0

Total

X+D

ST+D

b.

Outcome

ST≤X

ST>X

Call

0

ST–X

Zeros

X+D

X+D

Total

X+D

ST+D

ThetotalpayoffsforthetwostrategiesareequalregardlessofwhetherSTexceedsX.

c.Thecostofestablishingthestock-plus-putportfoliois:

S0+P

Thecostofestablishingthecall-plus-zeroportfoliois:

C+PV(X+D)

Therefore:

S0+P=C+PV(X+D)

Thisresultisidenticaltoequation20.2.

6.a.Bywritingcoveredcalloptions,Jonesreceivespremiumincomeof€30,000.If,inJanuary,thepriceofthestockislessthanorequalto€45,thenJoneswillhavehisstockplusthepremiumincome.Butthemosthecanhaveatthattimeis(€450,000+€30,000)becausethestockwillbecalledawayfromhimifthestockpriceexceeds€45.(Weareignoringhereanyinterestearnedoverthisshortperiodoftimeonthepremiumincomereceivedfromwritingtheoption.)Thepayoffstructureis:

StockpricePortfoliovalue

lessthan€4510,000timesstockprice+€30,000

greaterthan€45€450,000+€30,000=€480,000

ThisstrategyofferssomeextrapremiumincomebutleavesJonessubjecttosubstantialdownsiderisk.Atanextreme,ifthestockpricefelltozero,Joneswouldbeleftwithonly€30,000.Thisstrategyalsoputsacaponthefinalvalueat€480,000,butthisismorethansufficienttopurchasethehouse.

b.Bybuyingputoptionswitha€35strikeprice,Joneswillbepaying€30,000inpremiumsinordertoinsureaminimumlevelforthefinalvalueofhisposition.Thatminimumvalueis:

(€35⨯10,000)–€30,000=€320,000

Thisstrategyallowsforupsidegain,butexposesJonestothepossibilityofamoderatelossequaltothecostoftheputs.Thepayoffstructureis:

StockpricePortfoliovalue

lessthan€35€350,000–€30,000=€320,000

greaterthan€3510,000timesstockprice–€30,000

c.Thenetcostofthecollariszero.Thevalueoftheportfoliowillbeasfollows:

StockpricePortfoliovalue

lessthan€35€350,000

between€35and€4510,000timesstockprice

greaterthan€45€450,000

Ifthestockpriceislessthanorequalto€35,thenthecollarpreservesthe€350,000principal.Ifthepriceexceeds€45,thenJonesgainsuptoacapof€450,000.Inbetween€35and€45,hisproceedsequal10,000timesthestockprice.

Thebeststrategyinthiscasewouldbe(c)sinceitsatisfiesthetworequirementsofpreservingthe€350,000inprincipalwhileofferingachanceofgetting€450,000.Strategy(a)shouldberuledoutsinceitleavesJonesexposedtotheriskofsubstantiallossofprincipal.

Ourrankingwouldbe:

(1)strategyc;

(2)strategyb;(3)strategya.

7.a.

Position

STX1STX2

X2X3Longcall(X1)

0

ST–X1

ST–X1

ST–X1

Short2calls(X2)

0

0

–2(ST–X2)

–2(ST–X2)

Longcall(X3)

0

0

0

ST–X3

Total

0

ST–X1

2X2–X1–ST

(X2–X1)–(X3–X2)=0

b.

Position

STX1STX2X2X2XX2X2X2X2X2

X2Buycall(X2)

0

0

ST–X2

Buyput(X1)

X1–ST

0

0

Total

X1–ST

0

ST–X2

8.

Position

STX1STX2XX2

X2Buycall(X2)

0

0

ST–X2

Sellcall(X1)

0

–(ST–X1)

–(ST–X1)

Total

0

X1–ST

X1–X2

9.Thefarmerhastheoptiontosellthecroptothegovernmentforaguaranteedminimumpriceifthemarketpriceistoolow.IfthesupportpriceisdenotedPSandthemarketpricePmthenthefarmerhasaputoptiontosellthecrop(theasset)atanexercisepriceofPSevenifthepriceoftheunderlyingasset(Pm)islessthanPS.

10.Thebondholdershave,ineffect,madealoanwhichrequiresrepaymentofBdollars,whereBisthefacevalueofbonds.If,however,thevalueofthefirm(V)islessthanB,theloanissatisfiedbythebondholderstakingoverthefirm.Inthisway,thebondholdersareforcedto“pay”B(inthesensethattheloaniscancelled)inreturnforanassetworthonlyV.ItisasthoughthebondholderswroteaputonanassetworthVwithexercisepriceB.Alternatively,onemightviewthebondholdersasgivingtherighttotheequityholderstoreclaimthefirmbypayingofftheBdollardebt.Thebondholdershaveissuedacalltotheequityholders.

11.a.&b.TheExcelspreadsheetforbothparts(a)and(b)isshownonthenextpage,andtheprofitdiagramsareonthefollowingpage.

12.Themanagergetsabonusifthestockpriceexceedsacertainvalueandgetsnothingotherwise.Thisisthesameasthepayofftoacalloption.

13.i.Equityindex-linkednote:

Unliketraditionaldebtsecuritiesthatpayascheduledrateofcouponinterestonaperiodicbasisandtheparamountofprincipalatmaturity,theequityindex-linkednotetypicallypayslittleornocouponinterest;atmaturity,however,aunitholderreceivestheoriginalissuepriceplusasupplementalredemptionamount,thevalueofwhichdependsonwheretheequityindexsettledrelativetoapredeterminedinitiallevel.

ii.Commodity-linkedbearbond:

Unliketraditionaldebtsecuritiesthatpayascheduledrateofcouponinterestonaperiodicbasisandtheparamountofprincipalatmaturity,thecommodity-linkedbearbondallowsaninvestortoparticipateinadeclineinacommodity’sprice.Inexchangeforalowerthanmarketcoupon,buyersofabeartranchereceivearedemptionvaluethatexceedsthepurchasepriceifthecommoditypricehasdeclinedbythematuritydate.

SpreadsheetforProblem11:

StockPrices

BeginningMarketPrice

116.5

EndingMarketPrice

130

X130Straddle

Ending

Profit

BuyingOptions:

StockPrice

-37.20

CallOptionsStrike

Price

Payoff

Profit

Return%

50

42.80

110

22.80

20.00

-2.80

-12.28%

60

32.80

120

16.80

10.00

-6.80

-40.48%

70

22.80

130

13.60

0.00

-13.60

-100.00%

80

12.80

140

10.30

0.00

-10.30

-100.00%

90

2.80

100

-7.20

PutOptionsStrike

Price

Payoff

Profit

Return%

110

-17.20

110

12.60

0.00

-12.60

-100.00%

120

-27.20

120

17.20

0.00

-17.20

-100.00%

130

-37.20

130

23.60

0.00

-23.60

-100.00%

140

-27.20

140

30.50

10.00

-20.50

-67.21%

150

-17.20

160

-7.20

Straddle

Price

Payoff

Profit

Return%

170

2.80

110

35.40

20.00

-15.40

-43.50%

180

12.80

120

34.00

10.00

-24.00

-70.59%

190

22.80

130

37.20

0.00

-37.20

-100.00%

200

32.80

140

40.80

10.00

-30.80

-75.49%

210

42.80

SellingOptions:

Bullish

CallOptionsStrike

Price

Payoff

Profit

Return%

Ending

Spread

110

22.80

-20

2.80

12.28%

StockPrice

6.80

120

16.80

-10

6.80

40.48%

50

-3.2

130

13.60

0

13.60

100.00%

60

-3.2

140

10.30

0

10.30

100.00%

70

-3.2

80

-3.2

PutOptionsStrike

Price

Payoff

Profit

Return%

90

-3.2

110

12.60

0

12.60

100.00%

100

-3.2

120

17.20

0

17.20

100.00%

110

-3.2

130

23.60

0

23.60

100.00%

120

-3.2

140

30.50

10

40.50

132.79%

130

6.8

140

6.8

MoneySpread

Price

Payoff

Profit

150

6.8

BullishSpread

160

6.8

Purchase120Call

16.80

10.00

-6.80

170

6.8

Sell130Call

13.60

0

13.60

180

6.8

CombinedProfit

10.00

6.80

19

升级会员

升级会员