ProjectManagementcost estimates.docx

《ProjectManagementcost estimates.docx》由会员分享,可在线阅读,更多相关《ProjectManagementcost estimates.docx(38页珍藏版)》请在冰豆网上搜索。

ProjectManagementcostestimates

Chapter4Costestimates,Part1:

DefinitionsandPrinciples

Agoodestimateofprojectcostsisnecessaryforsubsequentmanagementdecisionsandcontrol.Themostobviousreasonforproducingcostestimatesistoassistinpricingdecisions,butthatisbynomeansthewholestory.Costestimatesareusuallyneededforallprojects,includingin-housemanagementprojectsandthosesoldwithoutfixedprices.Timescaleplanning,pre-allocationofprojectresources,theestablishmentofbudgetsforfunding,manpowerandcostcontrol,andthemeasurementofachievementagainstexpectedperformancealldemandtheprovisionofsoundestimates.

Costdefinitionsandprinciples

Itisgenerallyunderstoodinaccountingcirclesthattheword'cost'shouldneverbeusedalone,withoutaqualifyingadjective.Itmustalwaysbemadeclearexactlywhatkindsofcostsaremeant.Therearemanywaysinwhichcostscanbedescribed,butwithinthespaceofthischapteritisnecessarytooutlinesomeofthetermswithwhichcostestimatorsandprojectmanagersshouldbeacquainted.Thereisnoneedtoclarifyself-explanatoryterms(suchaslabourcosts,materialcostsandsoon),andthefollowinglisthasbeenlimitedtoafewtermsthatmaynotbefamiliartoallreaders.Thelistisinalphabeticalorder.

Absorptioncosting

SeeOverheadrecovery.

Below-the-linecosts

Acollectivenameforthevariousallowancesthatareaddedonceatotalbasiccostestimatehasbeenmade.Thesecanincludeallowancesforcostescalation,exchangeratefluctuationandothercontingencies.

Costescalation

Costescalationistheincreaseinanyelementofprojectcostswhenthecostofthatelementiscomparedbetweentwodifferentdates(forexample,nowandtwoyearshence).Causedbywageandsalaryawardsandinflationarypressuresonpricespaidformaterialsandpurchasedcomponents,costescalationisusuallyexpressedatanannualratepercent.

Directcosts

Costswhichcanbeattributeddirectlytoajoborprojecttaskaretermeddirectcosts.Thusifapersonspendstwohoursinthemanufactureofacomponentwhichisidentifiableasbeingrequiredforaparticularproject,thenthattimecanbeclassedasdirectlabouranditscostcanberecordedasadirectcosttobechargeddirecttotheproject.Similarly,materials,componentsandexpensesdirectlyattributabletoaparticularprojectcanbeclassedasdirect.

Factorycost

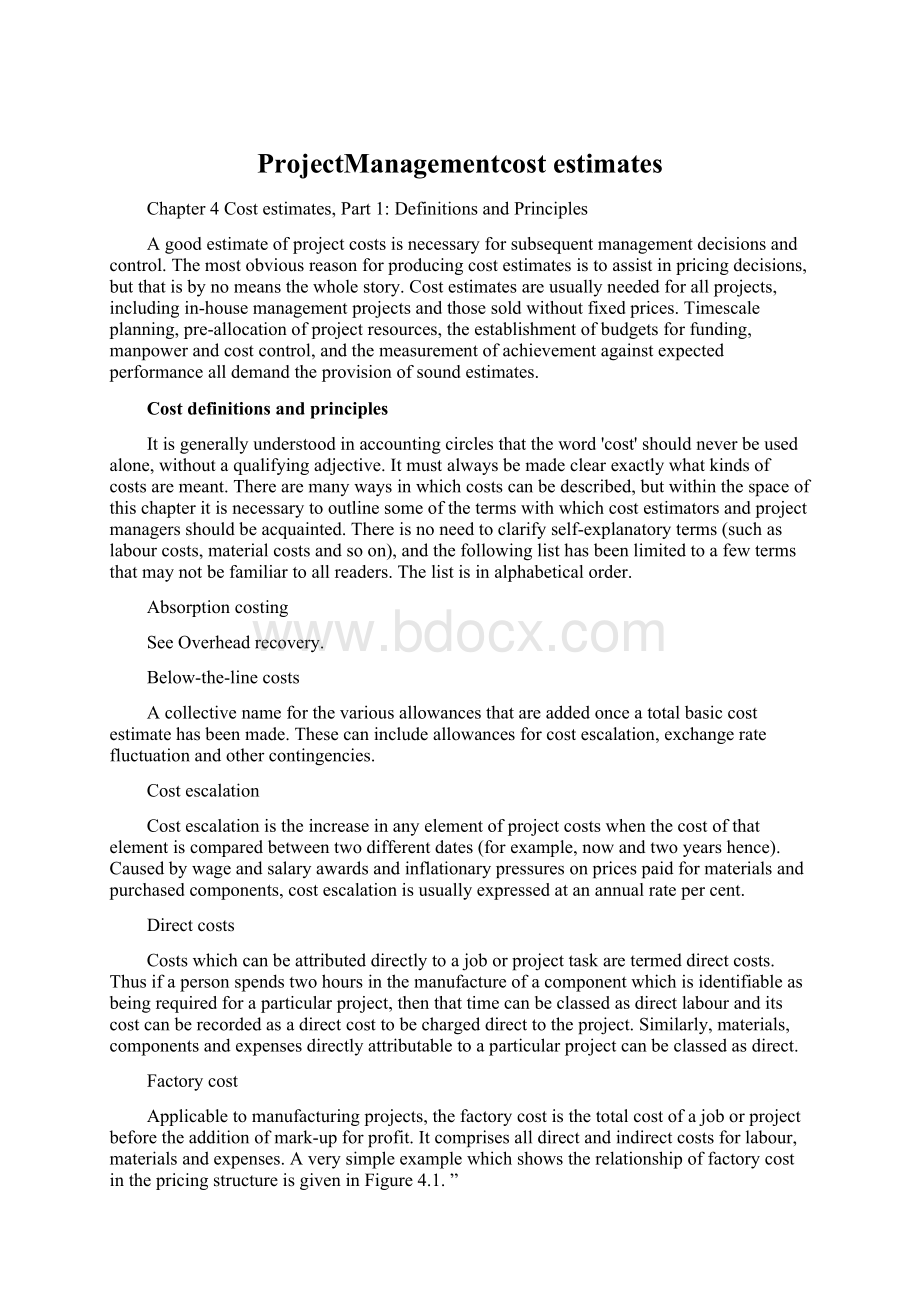

Applicabletomanufacturingprojects,thefactorycostisthetotalcostofajoborprojectbeforetheadditionofmark-upforprofit.Itcomprisesalldirectandindirectcostsforlabour,materialsandexpenses.AverysimpleexamplewhichshowstherelationshipoffactorycostinthepricingstructureisgiveninFigure4.1.”

Designcostsareoftentreatedasindirectinroutinemanufacturing,toberecoveredasoverheadsagainstbulksalesoftheresultingproduct.TheexampleinFigure4.1,however,isforaspecialproject.Althoughthisisaverysimpleproject,itcanrankasaprojectnonethelessbecauseitisforthedesignandone-offmanufactureofacomponenttosatisfyacustomer'sspecialpurchaseorder.Allthedesigncostsinthiscasecanberecordedandattributeddirectlytotheproject,andtheyhavethereforebeentreatedasdirectcosts.

Fixedcosts

Costsaresaidtobefixedwhentheyremainvirtuallyunchangedandmustcontinuetobeincurredeventhoughtheworkloadmightfluctuatebetweenzeroandthemaximumcapacity.Thesecoststypicallyincludemanagementandadministrativesalaries,rent,businessrates,heating,insurance,buildingsmaintenanceandsoon.Fixedcostsusuallyformbyfarthebiggestcomponentofacompany'sindirectoroverheadcosts(seeIndirectCosts).

item

£

£

£

Perhour

Directmaterials

Brasssheet

Brassrod

Other

Totalcostofdirectmaterials

1000.00

1500.00

1250.00

3750.00

Directlabour(standardcostrates)

Design

10hoursseniorengineer

25.00

250.00

15hoursdesignengineer

15.00

225.00

1hourchecker

17.00

17.00

Manufacture

200hourssheetmetal

13.00

2600.00

30hoursturner

13.00

390.00

10hourassembly

13.00

130.00

1hourinspection

16.00

16.00

Totaldirectlabourcost

Primecost

820.00

4570.00

Overheadsat130%ofdirectlabour

Factorycost

Mark-upat50%

Indicatedsellingprice

1066.00

5636.00

2818.00

8454.00

Figure4.1Costandpricestructureforasimplemanufacturingproject

Indirectcosts(overheadcostsoroverheads)

Theprovisionoffacilitiesandservicessuchasfactoryandofficeaccommodation,management,personnelandwelfareservices,training,costandmanagementaccounting,generaladministration,heating,lightingandmaintenancegivesrisetocoststhatmustgenerallybeincurredinrunningabusiness.Thesecostscanincludesalariesandwages,materialsandotherexpenses,but(exceptintheunusualcaseofanentireorganizationsetupspeciallytofulfilonlyoneproject)thesegeneralcostscannotbeallocateddirectlytoonejoborproject.Theyarethereforetermedindirectcosts,oftencalled'overheadcosts',orsimply'overheads'.

Notethattheprovisionoffacilitiesatthesiteofaconstructionproject,althoughthesemightincludeaccommodationandservicesthatwouldbeclassedasindirectbackatthemainorhomeoffice,canbeclassedasdirectcosts.Thisisbecausetheyareprovidedspecificallyfortheprojectinquestion,andcanthereforebeidentifiedsolelywiththatprojectandchargeddirectlytoit.

Thereareconsiderabledifferencesbetweencompaniesintheinterpretationofdirectandindirectcosts.Somefirmschargetoprojectsthecostsofprintingdrawings,forexample,andrecoverthosecostsdirectlybybillingthemtotheclientorcustomer.Otherfirmswouldregardsuchcostsasindirect,andchargethemtooverheads.Sometimestheclassificationofcostsasdirectorindirectcanvaryevenfromprojecttoprojectwithinthesamecompany,dependingonwhateachcustomerhasagreedandcontractedtopayforasadirectcharge.Costestimatorsandprojectmanagersmustbeclearonwhatconstitutesdirectandindirectcostsintheirparticularcompany,andmustalsopayattentiontoanyspecialprovisionscontainedintheproposalorcontractforeachproject.

Indirectcosts,althoughtheyarepredominantlyfixedcosts,cansometimesincludeanelementofvariablecosts.Maintainingapermanentheadquarterswouldbeafixedindirectcost,sinceitmustbeincurredirrespectiveofnormalworkloadfluctuations.Hiringtemporaryofficestafftoworkinadministrativedepartmentswouldbeavariablecost,becausetherateofexpenditure(thenumberandtypeoftemporarystaffhired)willvaryaccordingtofactorssuchasworkloadandavailabilityofpermanentstaff.Managementcandecidetoincreaseorreducethenumberoftemporarystaff(andhencetheircost)atwill.Classificationofoverheadsintofixedandvariablecostsisnotrelevanttomuchoftheargumentinthisbook,butitisimportantinthemanufacturingandprocessindustriesasacontrolinrelatingprices,profitabilityandthevolumeofproduction.

Whatevertheindustry,managementmustalwaysstrivetokeeptheoverheadexpensesaslowaspossibleinrelationtothedirectcosts,becausehighoverheadscankillacompany'schancesofbeingcompetitiveinthemarketplace.Itisinthevariableoverheadcostswheretheeasiestandquickestsavingscanbemade(shortofrelocatingthecompanyordismissingsomeofthepermanentadministrativeandmanagementstaff).

Labourburden

Thelabourburdenisanamount,usuallyexpressedasapercentageofwagesorsalaries,thatisaddedtothebasichourlyorweeklyrateforemployeestoallowfornon-workingtimeandvariousadditionalexpenses.Theconstituentsofatypicallabourburdenmightbethecostofpaidholidays,illnessorotherabsence,andpercapitaamountspayablebytheemployerasemployeebenefits,eithervoluntarilyorasarequirementofthenationallegislation.IntheUK,forexample,thesewouldincludeemployers'NationalInsurancecontributions.

Materialsburden

Materialspurchasedforaproject,whicharethemselveschargeableasadirectcost,aretypicallymarkedupbycontractorsinordertorecovertheiradministrativeandhandlingcosts.Thesemark-upsgenerallyrangefrom15percent(orless)forverylarge,costlyitemsshippeddirectlytositeto25percentorevenmoreonsmall,low-costitemsthathavehighhandlingandadministrationcostsrelativetotheirvalue.Acommonall-roundrateusedforthematerialsburdenis15percent.

Overheadcosts

SeeIndirectcosts.

Overheadrecovery

Mostprojectcostingsystemsworkonthebasisofchargingdirectlabourcosts(includingthelabourburden)astimerecordedonthejobmultipliedbythestandardhourlycostapplicabletothegrade.Anamountcanthenbeaddedtothislabourcost(usuallyasaratepercent)torecoverapartofthecompany'sindirect,overheadcosts.ThesimpleexampleinFigure4.1illustratesthisprinciple.

Thesameoverheadrate(130percentinFigure4.1)wouldnormallybeappliedoverallsimilarprojectscarriedoutbythecompany.Insomeindustriestheoverheadratecanriseto200percentorevenhigher(as,forexample,incompanieswithaveryhighlevelofresearchanddevelopmenttofund).Inlabour-intensiveindustries,withlittleresearchanddevelopmentandnohigh-gradepremises,theoverheadratemightbe50percentorevenless.Itisnotpossibletoindicatenorms,sincethecircumstancesofcompaniesvaryconsiderablyfromonetoanother(evenwheretheyarecarryingoutsimilarwork).Obviously,acompanywhichmanagestokeepitsindirectcosts(andoverheadrate)toaminimumenjoysacompetitiv

升级会员

升级会员