财务报表分析与运用 杰拉尔德 课后答案英文版第七章.docx

《财务报表分析与运用 杰拉尔德 课后答案英文版第七章.docx》由会员分享,可在线阅读,更多相关《财务报表分析与运用 杰拉尔德 课后答案英文版第七章.docx(34页珍藏版)》请在冰豆网上搜索。

财务报表分析与运用杰拉尔德课后答案英文版第七章

Chapter7Solutions

Overview:

ProblemLengthProblem#s

{S}2,3,5,8,and10

{M}1,4,6,7,9,11,12,and13

Appendices

{M}7A-1and7B-1

{L}7A-2and7B-2

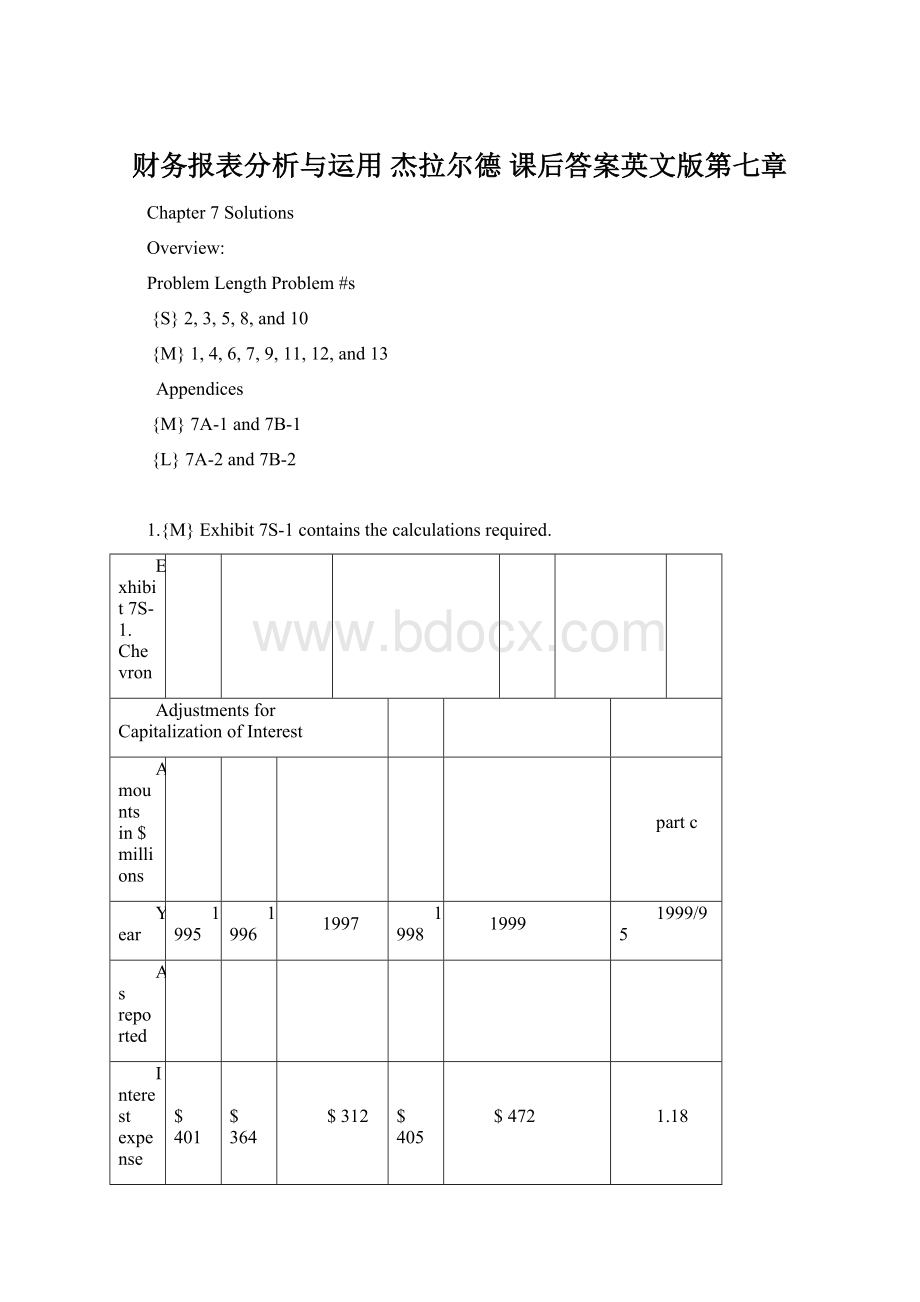

1.{M}Exhibit7S-1containsthecalculationsrequired.

Exhibit7S-1.Chevron

AdjustmentsforCapitalizationofInterest

Amountsin$millions

partc

Year

1995

1996

1997

1998

1999

1999/95

Asreported

Interestexpense

$401

$364

$312

$405

$472

1.18

Pretaxincome

1,789

4,740

5,502

1,834

3,648

2.04

Netincome

930

2,607

3,256

1,339

2,070

2.23

Capitalizedinterest

141

108

82

39

59

Amortizationofcapitalizedinterest

47

24

28

35

9

a.Calculations

EBIT

$2,190

$5,104

$5,814

$2,239

$4,120

Timesinterestearned

5.46

14.02

18.63

5.53

8.73

1.60

b.Adjusted

Netcapitalizedinterest

$94

$84

$54

$4

$50

After35%incometax

61

55

35

3

33

Interestexpense

542

472

394

444

531

0.98

EBIT

2,237

5,128

5,842

2,274

4,129

(i)Timesinterestearned

4.13

10.86

14.83

5.12

7.78

1.88

(ii)%reductionfromreportedratio

-24.4%

-22.5%

-20.4%

-7.4%

-10.9%

Pretaxincome

$1,695

$4,656

$5,448

$1,830

$3,598

2.12

(iii)Netincome

869

2,552

3,221

1,336

2,038

2.34

%reductionfromreported

-6.6%

-2.1%

-1.1%

-0.2%

-1.6%

b.(iv)Expensingallinterestreducesnetincomeforeachyear.Howevertheeffectdiminishesovertime.

c.(i)Becausetheamountofinterestcapitalizeddeclinedovertime,restatementreducestherateofincreaseininterestexpense.

(ii)Whiletheinterestcoverageratioislowerafterrestatement,itstrendimprovesduetothelowergrowthrateofinterestexpense.

(iii)Bothpretaxandnetincomearelowerafterrestatementbuttheirgrowthrateimprovesduetothelowergrowthrateofinterestexpense.

d.Therestateddataaremoreusefulforfinancialanalysisbecausetheyarebasedonactualinterestexpense.Theyprovidebettercomparabilitywithfirmsthatdonotcapitalizeinterest.

2.{S}a.(i)Interestcostcanbecapitalizedonborrowingsdirectlyassociatedwiththeprojectorwhenthecompanyhasdebtequaltoorexceedingthecostofconstruction.

(ii)Start-upcostsmustbeexpensedunderU.S.GAAP.

(iii)Shippingcostsareconsideredpartofthecostofacquisition.

(iv)IncreasesinthemarketvalueoflandandbuildingsmaynotberecognizedunderU.S.GAAP.

b.(i)WhilethebenchmarktreatmentunderIAS23istoexpenseallinterest,capitalizationofborrowingcostsdirectlyattributabletoaprojectisanallowedalternative.

(ii)SameasU.S.GAAPexceptthatthebenchmarkThecapitalizationofinterestisanallowedalternativeunderIAS23(paragraph11)

(iii)SameasU.S.GAAP.

(iv)WhilerevaluationisanallowedalternativeunderIAS16,itmustbeappliedtoallassetsinaparticularclassandcouldbeselectivelyappliedtoaparticularproject.

3.{S}a.UnderSFAS86(textpage242),computersoftwaredevelopmentcostscanbecapitalizedonlywheneconomicfeasibilityhasbeenestablished.

b.UnderIAS38(paragraph45),intangibleassetssuchascomputersoftwarecanberecognizedwhentheenterprisecandemonstratetechnicalandeconomicfeasibility.

4.{M}Exhibit7S-2containsthecalculationsrequiredbypartsathroughc.

Exhibit7S-2

Ericsson

AmountsinSEKmillions

1997

1998

1999

Developmentcostsforsoftwaretobesold:

Openingbalance

7,398

10,744

Capitalization

5,232

7,170

7,898

Amortization

(3,934)

(3,824)

(4,460)

Writedown

(989)

Year-endbalance

7,398

10,744

13,193

Developmentcostsforsoftwareforinternaluse:

Openingbalance

Capitalization

1,463

Amortization

(152)

Year-endbalance

1,311

a.UnderSwedishGAAP:

Netsales

167,740

184,438

215,403

Pretaxincome

17,218

18,210

16,386

Totalassets

147,440

167,456

202,628

Stockholders'equity

52,624

63,112

69,176

Averagetotalassets

157,448

185,042

Averageequity

57,868

66,144

Averagestockholders’equity

57,868

66,144

Assetturnover

1.17

1.16

PretaxROE

0.31

0.25

b.Adjustments:

Developmentcostsforsoftwaretobesold:

Capitalization

5,232

7,170

7,898

Amortization

(3,934)

(3,824)

(4,460)

Writedown

(989)

Neteffect

1,298

3,346

2,449

Developmentcostsforsoftwareforinternaluse:

Capitalization

1,463

Amortization

(152)

Neteffect

-

-

1,311

Totalpretaxeffect

1,298

3,346

3,760

Adjustedpretaxincome

18,516

21,556

20,146

(i)%change

8%

18%

23%

Exhibit7S-2(continued)

Year-endbalances:

Softwaretobesold

7,398

10,744

13,193

Internalusesoftware

1,311

Total

7,398

10,744

14,504

Less:

deferredtax@35%

(2,589)

(3,760)

(5,076)

Increaseinequity

4,809

6,984

9,428

Adjustedtotalassets

154,838

178,200

217,132

(ii)%change

5.0%

6.4%

7.2%

Adjustedequity

57,433

70,096

78,604

(iii)%change

9.1%

11.1%

13.6%

c:

Adjustedaverageassets

166,519

197,666

Adjustedaverageequity

63,764

74,350

(i)Adjustedassetturnover

1.11

1.09

(ii)AdjustedpretaxROE

0.34

0.27

d.TheadjustmentsforEricssonshowthatcapitalizationofsoftwaredevelopmentcostscanhaveasignificanteffectonreportedincomeandequity,andonfinancialratios.Thereforecomparabilityrequiresthatallfirmsberestatedtothesamebasis.

e.Theamountscapitalizedhighlightexpendituresandenabletheanalysttoinquireaboutthenewproductsunderdevelopment.Theamortizationperiodusedmaybeusefulasaforecastoftheusefullifeoftheproduct.Inbothcases(capitalizationandamortization)significantchangesfrompriorperiodsmayprovideusefulsignalsofimpendingchange.

5.{S}a.Thecapitalizationoftheinvestmentindisplaysdelaystheirimpactonincomeascomparedwithexpensing.Inaddition,cashfromoperationsispermanentlyincreasedastheexpendituresareclassifiedascashflowsforinvestment.Finally,iftheseexpendituresarevolatile,capitalizationandamortizationsmoothestheimpactonreportedincome.

b.(i)In2000,thecapitalizedamountincreasedby$1,648,000.Hadpromotionaldisplaysbeenexpensed,netincomewouldbe$1,071,200(after35%tax)lower.Expensingwouldhavereducednetincomeby7.4%($1,071.2/$14,467).

(ii)Shareholders’equitywouldbereducedby65%of$10,099,000equalto$6,564,350or7.1%.

(iii)Reportedreturnon(average)assetsequals$14,467/[($166,656+$140,609)/2]=9.42%

Adjustedreturnon(average)assetsequals($14,467–$1,071)/[($166,656-$10,099)+($140,609-$8,451)/2]=9.28%asassetsmustbereducedbytheinvestmentinpromotionaldisplays.

6.{M}a.Brandnamesareclearlyanasset.However,itisnotclearthattheseassetsshouldbeshownoncorporatebalancesheets.

Oneadvantageofrecognizingbrandnamesiscompleteness;abalancesheetthatignoresmajorfirmassetsisoflimiteduseforanalysis.Anotheradvantageisthatthecostofacquiringordevelopingabrandnameshouldberecordedasaninvestment(asset)inordertoproperlymatchrevenuesandexpenses.

Themajordisadvantageofbrandnamerecognitionisthedifficultyofpropermeasurement.Aseachbrandnameisunique,markettransactionsarenotavailabletovaluethebrand.Thus,thevaluerecognizedissubjective;differencesacrossfirmsmayreflecteitherrealdifferencesinthevalueofthebrandsordifferentmeasurementdecisions.

Oneapproachinvolvescapitalizationoftheacquisitioncost(forpurchasedbrands)ortheadvertisingandotherdevelopmentcosts(forinternallydevelopedbrands).Inthelattercase,itisunlikelythatthevalueofthebrandwillbeequaltothecostofdevelopment.Asuccessfulbrandwillbeworthmuchmorethanthecostofitsdevelopment;anunsuccessfulbrandmayhavenovalueatall.(Thesecharacteristicsmayalsodescribeacquiredbrands.)

Further,thevalueofbrandschangesovertime.DespitethequotationfromLaing,brandscanalsobecome"dilapidated"iftheyareneglected,iftheadvertisingispoor,oriftheproductsaredefective.Thevalueofbrandswillalsobeaffectedbychangesinmarketconditions,e.g.,pricingdecisionsandtheinroadsmadebygenericproducts.

Fromthepointofviewoffinancialanalysis,therefore,itisnotclearthatreportingmanagement'sestimateofbrandvaluewouldbehelpful.The"proofofthepuddingisintheeating"andavaluablebrandshouldbehighlyprofitable.Theevaluationofthatprofitabilitymightbebetterlefttothemarketplace.

b.Theadvantageofamortizationisthattheincomestatementshouldreflectallexpensesthathelpproduceincome.Ifprofitabilityisduetothebrandname,theamortizationofitsacquisitioncostshouldbeanelementofexpense.

Ontheotherhand,giventhesubjectivityofbrandnamevaluation,theamortizationamount(alsoaffectedbythechoiceofmethodandlife)maybeapoormeasureoftheexpiredvalue.Inaddition,brandnamesmaynotdeclineinvalueovertime;anydeclineislikelytobeirregular.

Forpurposesofanalysis,therefore,theamortizationofbrandnameintangibleassetsshouldbeexcludedfromincome.Theevaluationofprofitability,however,shouldconsidertheroleofbrandnames.

Exhibit7S-3

NorskHydro

1998R

升级会员

升级会员