会计英语课后习题参考答案.docx

《会计英语课后习题参考答案.docx》由会员分享,可在线阅读,更多相关《会计英语课后习题参考答案.docx(22页珍藏版)》请在冰豆网上搜索。

会计英语课后习题参考答案

SuggestedSolution

Chapter1

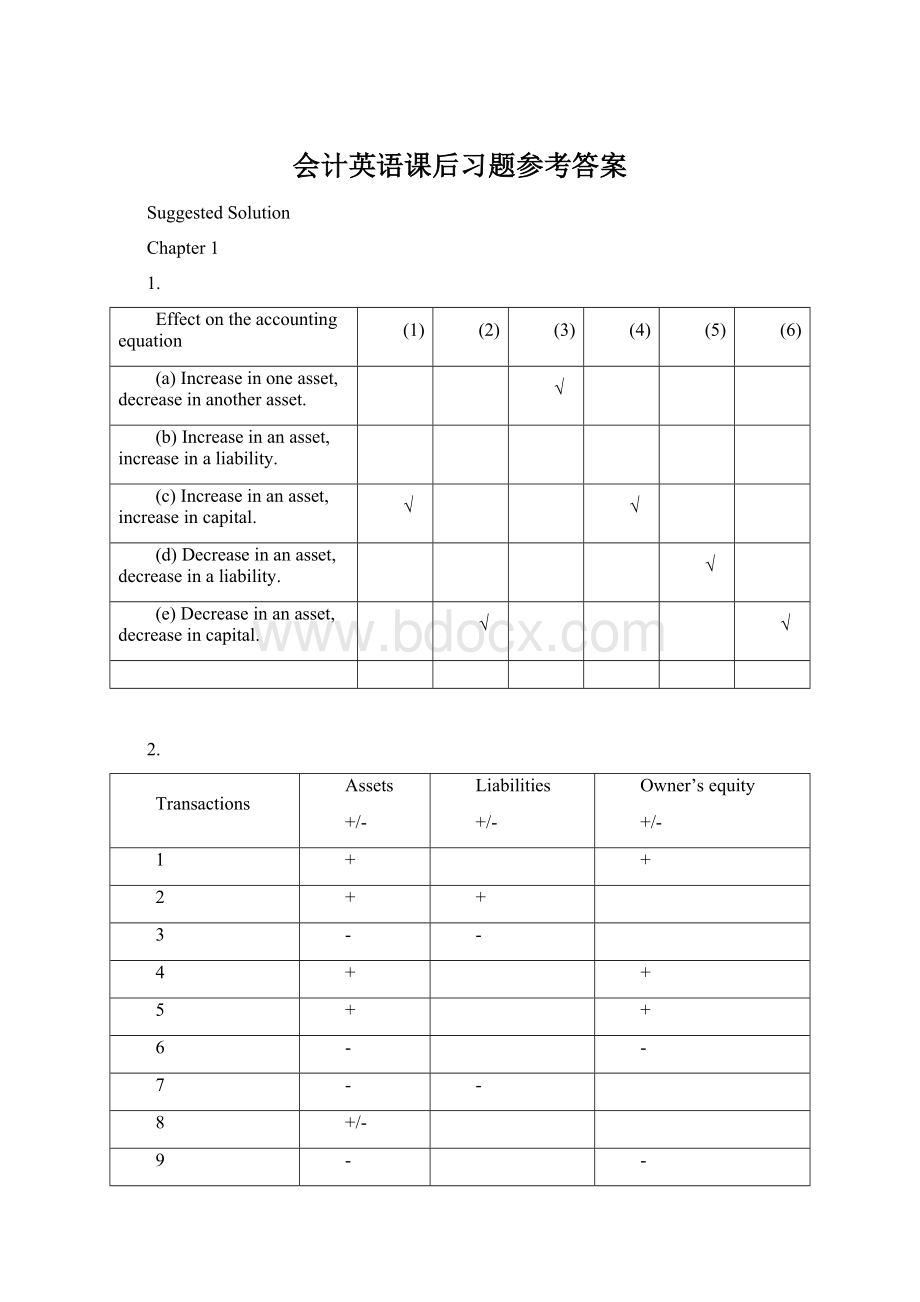

1.

Effectontheaccountingequation

(1)

(2)

(3)

(4)

(5)

(6)

(a)Increaseinoneasset,decreaseinanotherasset.

√

(b)Increaseinanasset,increaseinaliability.

(c)Increaseinanasset,increaseincapital.

√

√

(d)Decreaseinanasset,decreaseinaliability.

√

(e)Decreaseinanasset,decreaseincapital.

√

√

2.

Transactions

Assets

+/-

Liabilities

+/-

Owner’sequity

+/-

1

+

+

2

+

+

3

-

-

4

+

+

5

+

+

6

-

-

7

-

-

8

+/-

9

-

-

10

-

-

3.

Describeeachtransactionbasedonthesummaryabove.

Transactions

1

Purchasedlandforcash,$6,000.

2

Investmentforcash,$3,200.

3

Paidexpense$1,200.

4

Purchasedsuppliesonaccount,$800.

5

Paidowner’spersonaluse,$750.

6

Paidcreditor,$1,500

7

Suppliesusedduringtheperiod,$630.

4.

Assets

Liabilities

Equity

Beginning

275,000

80,000

195,000

Add.investment

48,000

Add.Netincome

27,000

Lesswithdrawals

-35,000

Ending

320,000

85,000

235,000

5.

(a)

March31,20XX

April30,20XX

Assets

Cash

4,500

5,400

Accountsreceivable

2,560

4,100

Supplies

840

450

Totalassets

7,900

9,950

Liabilities

Accountspayable

430

690

Equity

TinaPierce,Capital

7,470

9,260

(b)netincome=9,260-7,470=1,790

(c)netincome=1,790+2,500=4,290

Chapter2

1.

a.ToincreaseNotesPayable-CR

b.TodecreaseAccountsReceivable-CR

c.ToincreaseOwner,Capital-CR

d.TodecreaseUnearnedFees-DR

e.TodecreasePrepaidInsurance-CR

f.TodecreaseCash-CR

g.ToincreaseUtilitiesExpense-DR

h.ToincreaseFeesEarned-CR

i.ToincreaseStoreEquipment-DR

j.ToincreaseOwner,Withdrawal-DR

2.

a.

Cash

1,800

Accountspayable

1,800

b.

Revenue

4,500

Accountsreceivable

4,500

c.

Owner’swithdrawals

1,500

SalariesExpense

1,500

d.

AccountsReceivable

750

Revenue

750

3.

PrepareadjustingjournalentriesatDecember31,theendoftheyear.

Advertisingexpense

600

Prepaidadvertising

600

Insuranceexpense(2160/12*2)

360

Prepaidinsurance

360

Unearnedrevenue

2,100

Servicerevenue

2,100

Consultantexpense

900

Prepaidconsultant

900

Unearnedrevenue

3,000

Servicerevenue

3,000

4.

1.$388,400

2.$22,520

3.$366,600

4.$21,800

5.

1.netlossfortheyearendedJune30,2002:

$60,000

2.DRJonNissen,Capital60,000

CRincomesummary60,000

3.post-closingbalanceinJonNissen,CapitalatJune30,2002:

$54,000

Chapter3

1.DundeeRealtybankreconciliation

October31,2009

Reconciledbalance$6,220Reconciledbalance$6,220

2.April7Dr:

Notesreceivable—Acompany5400

Cr:

Accountsreceivable—Acompany5400

12Dr:

Cash5394.5

Interestexpense5.5

Cr:

Notesreceivable5400

June6Dr:

Accountsreceivable—Acompany5533

Cr:

Cash5533

18Dr:

Cash5560.7

Cr:

Accountsreceivable—Acompany5533

Interestrevenue27.7

3.(a)Asawhole:

theendinginventory=685

(b)appliedseparatelytoeachproduct:

theendinginventory=625

4.Thecostofgoodsavailableforsale=endinginventory+thecostofgoods=80,000+200,000*500%=80,000+1,000,000=1,080,000

5.

(1)24,000+60,000-90,000*0.8=12000

(2)(60,000+24,000)/(85,000+31,000)*(85,000+31,000-90,000)=18828

Chapter4

1.(a)second-yeardepreciation=(114,000–5,700)/5=21,660;

(b)second-yeardepreciation=8,600*(114,000–5,700)/36,100=25,800;

(c)first-yeardepreciation=114,000*40%=45,600

second-yeardepreciation=(114,000–45,600)*40%=27,360;

(d)second-yeardepreciation=(114,000–5,700)*4/15=28,880.

2.(a)weighted-averageaccumulatedexpenditures(2008)=75,000*12/12+84,000*9/12+180,000*8/12+300,000*7/12+100,000*6/12=483,000

(b)interestcapitalizedduring2008=60,000*12%+(483,000–60,000)*10%=49,500

3.

(1)depreciationexpense=30,000

(2)bookvalue=600,000–30,000*2=540,000

(3)depreciationexpense=(600,000–30,000*8)/16=22,500

(4)bookvalue=600,000–30,000*8–22,500=337,500

4.Situation1:

Jan1st,2008InvestmentinM260,000

Cash260,000

June30Cash6000

Dividendrevenue6000

Situation2:

January1,2008InvestmentinS81,000

Cash81,000

June15Cash10,800

InvestmentinS10,800

December31InvestmentinS25,500

InvestmentRevenue25,500

5.a.December31,2008InvestmentinK1,200,000

Cash1,200,000

June30,2009DividendReceivable42,500

DividendRevenue42,500

December31,2009Cash42,500

DividendReceivable42,500

b.December31,2008InvestmentinK1,200,000

Cash1,200,000

December31,2009Cash42,500

InvestmentinK42,500

InvestmentinK146,000

Investmentrevenue146,000

c.Ina,theinvestmentamountis1,200,000

netincomereposedis42,500

Inb,theinvestmentamountis1,303,500

Netincomereposedis146,000

Chapter5

1.

a.June1:

Dr:

Inventory198,000

Cr:

AccountsPayable198,000

June11:

Dr:

AccountsPayable198,000

Cr:

NotesPayable198,000

June12:

Dr:

Cash300,000

Cr:

NotesPayable300,000

b.Dr:

InterestExpenses(fornotesonJune11)12,100

Cr:

InterestPayable12,100

Dr:

InterestExpenses(fornotesonJune12)8,175

Cr:

InterestPayable8,175

c.Balancesheetpresentation:

NotesPayable498,000

AccruedInterestonNotesPayable20,275

d.ForGreen:

Dr:

NotesPayable198,000

InterestPayable12,100

InterestExpense7,700

Cr:

Cash217,800

ForWestern:

Dr:

NotesPayable300,000

InterestPayable8,175

InterestExpense18,825

Cr:

Cash327,000

2.

(1)208Deferredincometaxisaliability2,400

Incometaxpayable21,600

209Deferredincometaxisanasset600

Incometaxpayable26,100

(2)208:

Dr:

Taxexpense24,000

Cr:

Incometaxpayable21,600

Deferredincometax2,400

209:

Dr:

Taxexpense25,500

Deferredincometax600

Cr:

Incometaxpayable26,100

(3)208:

Incomestatement:

taxexpense24,000

Balancesheet:

incometaxpayable21,600

209:

Incomestatement:

taxexpense25,500

Balancesheet:

incometaxpayable26,100

3.

a.1,560,000(20000000*12%*(1-35%))

b.7.8%(20000000*12%*(1-35%)/20000000)

4.

maturityvalue

numberofinterestperiods

statedrateperinterest-period

effectiveinterestrateperinterest-period

paymentamountperperiod

presentvalueofbondsatdateofissue

1

$10

40

3.75%

3%

$0.375

$11.73

2

20

10

10%

12%

2

17.74

3

25

10

0%

12%

0

8.05

5.

NotesPayable14,400

InterestPayable1,296

AccountsPayable60,000

+UnearnedRentRevenue7,200

CurrentLiabilities82,896

Chapter6

1.Mar.1

Cash1,200,000

CommonStock1,000,000

Paid-inCapitalinExcessofParValue200,000

Mar.15

OrganizationExpense50,000

CommonStock50,000

Mar.23

Patent120,000

CommonStock100,000

Paid-inCapitalinExcessofParValue20,000

Thevalueofthepatentisnoteasilydeterminable,sousetheissuepriceof$12pershareonMarch1whichistheissuingpriceofcommonstock.

2.July.1

TreasuryStock180,000

Cash180,000

Thecostoftreasurypurchasedis180,000/30,000=60pershare.

Nov.1

Cash70,000

TreasuryStock60,000

Paid-inCapitalfromTreasuryStock10,000

Sellthetreasuryatthecostof$60pershare,andsellingpriceis$70pershare.Thetreasurystockissoldabovethecost.

Dec.20

Cash75,000

Paid-inCapitalfromTreasuryStock15,000

TreasuryStock90,000

Thecostoftreasuryis$60persharewhilethesellingpriceis$50whichislowerthanthecost.

3.a.July1

RetainedEarnings24,000

DividendsPayable—PreferredStock24,000

b.Sept.1

DividendsPayable—PreferredStock24,000

Cash24,000

c.Dec.1

RetainedEarnings80,000

DividendsPayable—CommonStock80,000

d.Dec.31

IncomeSummary350,000

RetainedEarnings350,000

4.

a.Preferredstockgivesitsownercertainadvantagesovercommonstockholders.Thesebenefitsincludetherighttoreceivedividendsbeforethecommonstockholdersandtherighttoreceiveassetsbeforethecommonstockholdersifthecorporationliquidates.Corporationpayafixedamountofdividendsonpreferredstock.

The7%cumulativetermindicatesthattheinvestorsearn7%fixeddividends.

b.7%*120%*20,000=504,000

c.Ifcorporationissueddebt,ithasobligationtorepayprincipal

d.Thedateofdeclarationdecreasethestockholders’equity;thedateofrecordandthedateofpaymenthavenoeffectonstockholders.

5.

a.Jan.15

RetainedEarnings35,000

AccumulatedDepreciation35,000

Tocorrecterrorinprioryear’sdepreciation.

b.Mar.20

LossfromEarthquake70,000

Building70,000

c.Mar.31

RetainedEarnings12,500

DividendsPayable12,500

d.Apirl.15

DividendsPayable12,500

Cash12,500

e.June30

RetainedEarnings37,500

CommonStock25,000

AdditionalPaid-inCapital12,500

Torecordissuanceof10%stockdividend:

10%*25,000=2,500shares;

2500*$15=$37,500

f.Dec.31

DepreciationExpense14,000

AccumulatedDepreciation14,000

Originaldepreciation:

$40,000/40=$10,000peryear.BookvalueonJan.1,2009is$350,000(=$400,000-5*$10,000).Deprecationfor2009is$14,000(=$350,000/25).

g.Thecompanydoesnotneedtomakeentryintheaccountingrecords.ButtheamountofCommonStock($10parvalue)decreases275,000,whiletheamountofCommonStock($5parvalue)increases275,000.

Chapter7

1.

Requirement1

Ifrevenueisrecognizedatthedateofdelivery,thefollowingjournalentrieswouldbeusedtorecordthetransactionsforthetwoyears:

Year1

I

升级会员

升级会员