财务报表分析与运用杰拉尔德课后答案英文版第三章.docx

《财务报表分析与运用杰拉尔德课后答案英文版第三章.docx》由会员分享,可在线阅读,更多相关《财务报表分析与运用杰拉尔德课后答案英文版第三章.docx(50页珍藏版)》请在冰豆网上搜索。

财务报表分析与运用杰拉尔德课后答案英文版第三章

财务报表分析与运用杰拉尔德课后答案英文版第三章

Chapter3-Solutions

Overview:

ProblemLengthProblem#’s

{S}1,3

{M}2,7,8,12,13

{L}4-6,9-11,14,15

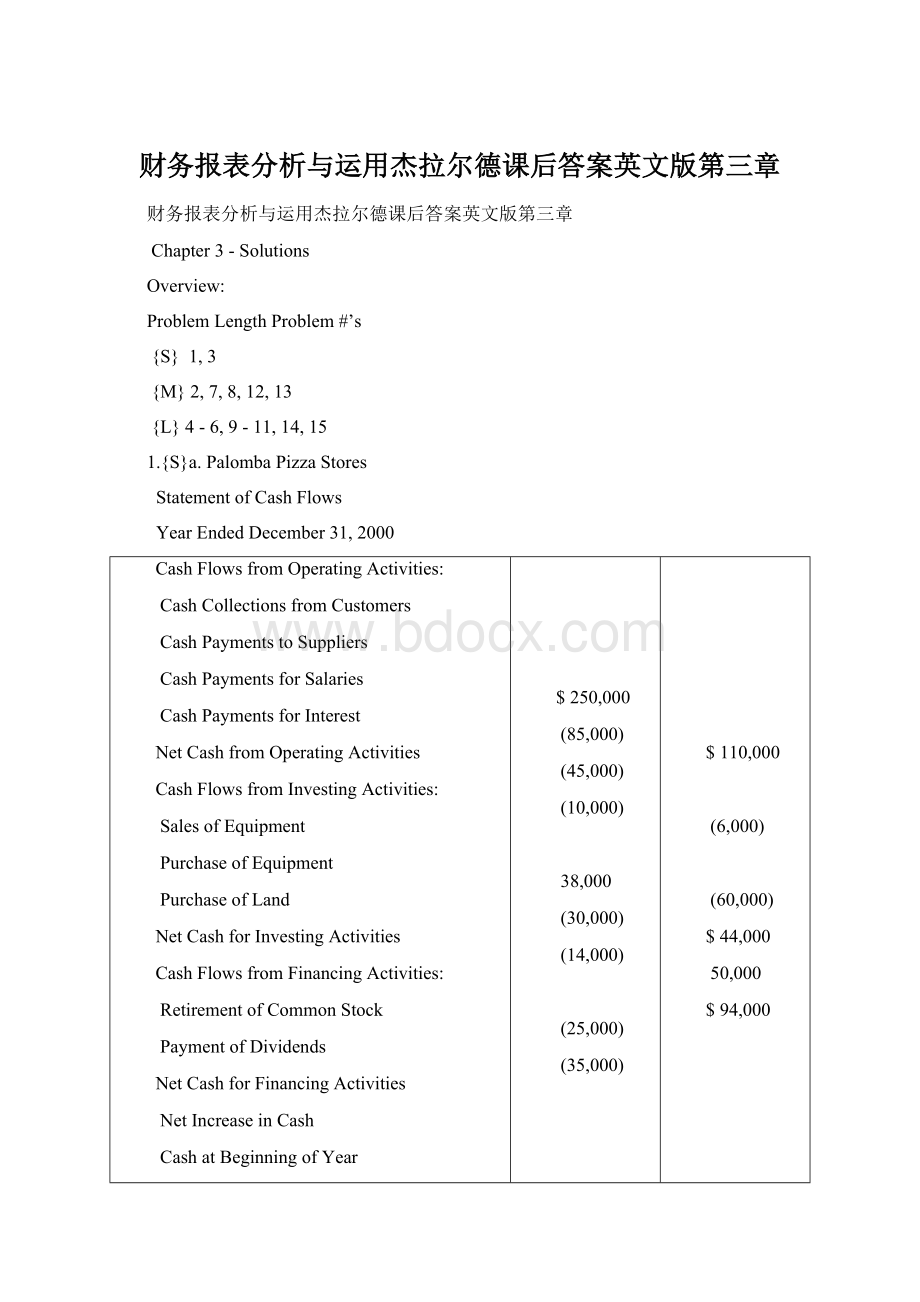

1.{S}a.PalombaPizzaStores

StatementofCashFlows

YearEndedDecember31,2000

CashFlowsfromOperatingActivities:

CashCollectionsfromCustomers

CashPaymentstoSuppliers

CashPaymentsforSalaries

CashPaymentsforInterest

NetCashfromOperatingActivities

CashFlowsfromInvestingActivities:

SalesofEquipment

PurchaseofEquipment

PurchaseofLand

NetCashforInvestingActivities

CashFlowsfromFinancingActivities:

RetirementofCommonStock

PaymentofDividends

NetCashforFinancingActivities

NetIncreaseinCash

CashatBeginningofYear

CashatEndofYear

$250,000

(85,000)

(45,000)

(10,000)

38,000

(30,000)

(14,000)

(25,000)

(35,000)

$110,000

(6,000)

(60,000)

$44,000

50,000

$94,000

b.CashFlowfromOperations(CFO)measuresthecashgeneratingabilityofoperations,inadditiontoprofitability.Ifusedasameasureofperformance,CFOislesssubjecttodistortionthannetincome.AnalystsusetheCFOasacheckonthequalityofreportedearnings,althoughitisnotasubstitutefornetincome.CompanieswithhighnetincomeandlowCFOmaybeusingoverlyaggressiveincomerecognitiontechniques.Theabilityofafirmtogeneratecashfromoperationsonaconsistentbasisisoneindicationofthefinancialhealthofthefirm.AnalystssearchfortrendsinCFOtoindicatefuturecashconditionsandpotentialliquidityorsolvencyproblems.

CashFlowfromInvestingActivities(CFI)reportshowthefirmisinvestingitsexcesscash.TheanalystmustconsidertheabilityofthefirmtocontinuetogrowandCFIisagoodindicationoftheattitudeofmanagementinthisarea.Thiscomponentoftotalcashflowincludesthecapitalexpendituresmadebymanagementtomaintainandexpandproductivecapacity.DecreasingCFImaybeaforecastofslowerfuturegrowth.

CashFlowfromFinancing(CFF)indicatesthesourcesoffinancingforthefirm.Forfirmsthatrequireexternalsourcesoffinancing(eitherborrowingorequityfinancing)itcommunicatesmanagement'spreferencesregardingfinancialleverage.Debtfinancingindicatesfuturecashrequirementsforprincipalandinterestpayments.Equityfinancingwillcausefutureearningspersharedilution.

Forfirmswhoseoperatingcashflowexceedsinvestmentneeds,CFFindicateswhetherthatexcessisusedtorepaydebt,pay(orincrease)cashdividends,orrepurchaseoutstandingshares.

c.CashpaymentsforinterestshouldbeclassifiedasCFFforpurposesofanalysis.Thisclassificationseparatestheeffectoffinancialleveragedecisionsfromoperatingresults.ItalsofacilitatesthecomparisonofPalombawithotherfirmswhosefinancialleveragediffers.

d.Thechangeincashhasnoanalyticsignificance.Thechangeincash(andhence,thecashbalanceattheendoftheyear)isaproductofmanagementdecisionsregardingfinancing.Forexample,thefirmcanshowalargecashbalancebydrawingonbanklinesjustpriortoyearend.

e.andf.

Thereareanumberofdefinitionsoffreecashflows.

Inthetext,freecashflowisdefinedascashfromoperationslesstheamountofcapitalexpendituresrequiredtomaintainthefirm’scurrentproductivecapacity.Thisdefinitionrequirestheexclusionofcostsofgrowthandacquisitions.However,fewfirmsprovideseparatedisclosuresofexpendituresincurredtomaintainproductivecapacity.Capitalcostsofacquisitionsmaybeobtainedfromproxystatementsandotherdisclosuresofacquisitions(SeeChapter14).

Inthefinanceliterature,freecashflowsavailabletoequityholdersareoftenmeasuredascashfromoperationslesscapitalexpenditures.Interestpaidisadeductionwhencomputingcashfromoperationsasitispaidtocreditors.Palomba’sfreecashflowavailabletoequityholdersiscalculatedasfollows:

Netcashflowfromoperatingactivitieslessnetcashforinvestingactivities:

$110,000-$6,000=$104,000

Theinvestmentactivitiesdisclosedintheproblemdonotindicateanyacquisitions.

Anotherdefinitionoffreecashflows,whichfocusesonfreecashflowavailabletoallprovidersofcapital,wouldexcludepaymentsforinterest($10,000inthiscase)anddebt.Thus,Palomba’sfreecashflowavailabletoallprovidersofcapitalwouldbe$114,000.

2.{M}a.

1996

1997

1998

1999

2000

2001

Sales

Baddebtexpense

Netreceivables

Cashcollections1

$---

---

30

$---

$140

7

40

$123

$150

7

50

$133

$165

8

60

$147

$175

10

75

$150

$195

10

95

$165

1Sales-baddebtexpense-increaseinnetreceivables

b.

1997

1998

1999

2000

2001

Baddebtexpense/sales

5.0%

4.7%

4.9%

5.7%

5.1%

Netreceivables/sales

28.6

33.3

36.4

42.8

48.7

Cashcollections/sales

87.9

88.7

89.1

85.7

84.6

c.Thebaddebtprovisiondoesnotseemtobeadequate.From1997-2001salesincreasedbyapproximately40%,whilenetreceivablesmorethandoubled,indicatingthatcollectionshavebeenlagging.Theratioscalculatedinpartbalsoindicatetheproblem.Whilebaddebtexpensehasremainedfairlyconstantat5%ofsalesoverthe5yearperiod,netreceivablesasapercentageofsaleshaveincreasedfrom29%to49%;cashcollectionsrelativetosaleshavedeclined.OtherpossibleexplanationsforthesedataarethatstatedpaymenttermshavelengthenedorthatStengelhasallowedcustomerstodelaypaymentforcompetitivereasons.

3.{S}NiagaraCompany

StatementofCashFlows2001

Cashcollections

Cashinputs

Cashexpenses

Cashinterestpaid

Incometaxespaid

CashfromOperations

Purchaseoffixedassets

CashUsedforInvesting

IncreaseinLTdebt

Decreaseinnotespayable

Dividendspaid

CashUsedforFinancing

NetChangeinCash

CashBalance12/31/00

CashBalance12/31/01

$980

(670)

(75)

(40)

(30)

$165

(150)

(150)

50

(25)

(30)

(5)

$1050

$60

[Sales-∆AccountsReceivable]

[COGS+∆Inventory

[Selling&GeneralExpense-∆AccountsPayable1]

[InterestExpense-∆InterestPayable]

[IncomeTaxExpense-∆DeferredTax]

[DepreciationExpense+∆FixedAssets(net)]

[NetIncome-∆Retainedearnings]

1Canalsobeusedtocalculatecashinputs,decreasingthatoutflowto$645whileincreasingcashexpensesto$100.

4.{L}a.GCompany

IncomeStatement,2000($thousands)

Sales

COGS+operating

expenses1

Depreciation

Interest

Taxes

Netincome

$3,841

3,651

15

41

42

$92

[receiptsfromcustomers+increaseinaccountsreceivable]

[payments-increaseininventory+increaseinaccountspayable]

[increaseinaccumulateddepreciation]

[payments]

[payment+increaseintaxpayable]

[check=changeinretainedearningsastherearenodividends]

1Notethatthesetwoitemscannotbecalculatedseparatelyfromtheinformationavailable.

b.MCompany

CashReceiptsandDisbursements,2000($thousands)

Cashreceiptsfrom:

Customers

Issueofstock

Short-termdebt

Long-termdebt

Total

Cashdisbursements:

COGSandoperatingexpenses

Taxes

Interest

Dividends

PP&Epurchase

Total

Changeincash

$1,807

3

62

96

$1,968

$1,843

3

51

22

33

$1,952

$16

[Sales-increaseinreceivables]

[Increaseinaccount]

[Increaseinliability]

[Increaseinliability]

[COGS+operatingexpense+increaseininventory+decreaseinaccountspayable]

[Expense-increaseintaxpayable]

[Expense]

[Income+increaseinretainedearnings]

[ChangeinPP&E]

Note:

Thisisnotatruereceiptsanddisbursementsscheduleasitshowscertainamounts(e.g.,debt)onanetbasisratherthangross.Suchschedules(andcashflowstatements)preparedfrompublisheddatacanonlyshowsomeamountsnet,unlesssupplementarydataareavailable.

c.ThecashflowstatementsarepresentedwiththeincomestatementforcomparisonpurposesinansweringPartd.

MCompany:

StatementofCashFlows($thousands)

1996

1997

1998

1999

2000

CFO:

Fromcustomers

Lessoutlaysfor:

COGS/oper.exp.

Interest

Taxes

CFI:

PP&Epurchase

CFF:

Issueofstock

Short-termdebt

Long-termdebt

Dividends

Stockrepurchase

LTdebtrepaid

STdebtrepaid

Changeincash

$1,165

1,130

15

23

$(3)

(14)

5

64

--

(20)

(22)

(2)

--

$25

8

$1,210

1,187

19

19

$(15)

(17)

5

65

--

(21)

(14)

(2)

--

$33

1

$1,327

1,326

16

9

$(24)

(37)

8

--

100

(21)

--

(3)

(8)

$76

15

$1,587

1,672

21

9

$(115)

(30)

3

153

--

(21)

(10)

--

--

$125

(20)

$1,807

1,843

51

3

$(90)

(33)

3

62

96

(22)

--

--

--

$139

16

MCompany:

IncomeStatement($thousands)

1996

1997

1998

1999

2000

Sales

COGS

Operatingexpense

Depreciation

Interest

Taxes

Total

NetIncome

$1,220

818

298

9

15

38

$1,178

42

$1,265

843

320

10

19

33

$1,225

40

$1,384

931

363

11

16

27

$1,348

36

$1,655

1,125

434

12

21

26

$1,852

37

$1,861

1,277

504

14

51

6

$1,852

9

GCompany:

StatementofCashFlows($thousands)

1996

1997

1998

1999

2000

CFO:

Fromcustomers

Disbursements:

COGS/Oper.exp.

Interest

Taxes

CFI:

PP&Epurchase

CFF:

Issueofstock

Short-termdebt

Long-termdebt

Changeincash

$1,110

1,214

11

13

$(128)

---

10

80

40

$130

$2

$1,659

1,702

13

15

$(71)

---

---

52

23

$75

$4

$2,163

1,702

23

16

$(

升级会员

升级会员