Multiple Linear Regression Model1.docx

《Multiple Linear Regression Model1.docx》由会员分享,可在线阅读,更多相关《Multiple Linear Regression Model1.docx(12页珍藏版)》请在冰豆网上搜索。

MultipleLinearRegressionModel1

MultipleLinearRegressionModel

Ⅰ.Introduction

ByusingRsoftwareestimationcanbeturnedintolinearregressionmodelofthenonlinearmodel,andtheparametersofthelinearregressionmodeltestoflinearconstraints.Thisexperimentonthegrossvalueofindustrialoutputandassetsandworkernumberoflinearityregressionanalysis.

Ⅱ.Caseintroduced

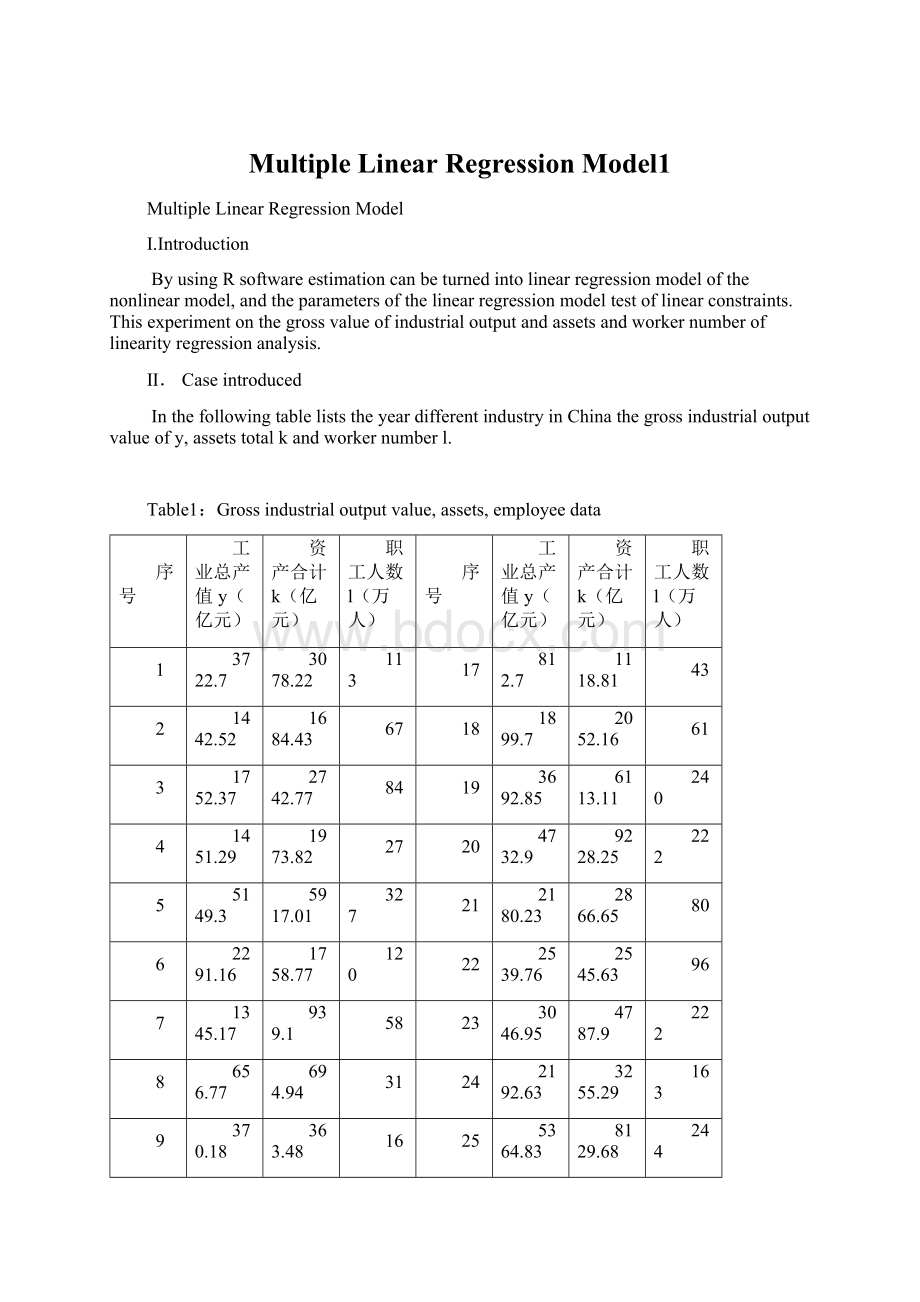

InthefollowingtableliststheyeardifferentindustryinChinathegrossindustrialoutputvalueofy,assetstotalkandworkernumberl.

Table1:

Grossindustrialoutputvalue,assets,employeedata

序号

工业总产值y(亿元)

资产合计k(亿元)

职工人数l(万人)

序号

工业总产值y(亿元)

资产合计k(亿元)

职工人数l(万人)

1

3722.7

3078.22

113

17

812.7

1118.81

43

2

1442.52

1684.43

67

18

1899.7

2052.16

61

3

1752.37

2742.77

84

19

3692.85

6113.11

240

4

1451.29

1973.82

27

20

4732.9

9228.25

222

5

5149.3

5917.01

327

21

2180.23

2866.65

80

6

2291.16

1758.77

120

22

2539.76

2545.63

96

7

1345.17

939.1

58

23

3046.95

4787.9

222

8

656.77

694.94

31

24

2192.63

3255.29

163

9

370.18

363.48

16

25

5364.83

8129.68

244

10

1590.36

2511.99

66

26

4834.68

5260.2

145

11

616.71

973.73

58

27

7549.58

7518.79

138

12

617.94

516.01

28

28

867.91

984.52

46

13

4429.19

3785.91

61

29

4611.39

18626.94

218

14

5749.02

8688.03

254

30

170.3

610.91

19

15

1781.37

2798.9

83

31

325.53

1523.19

45

16

1243.07

1808.44

33

Ⅲ.ModelBuilding

3.1.Model_1Setamodelfor

Step1:

Readthedata

>da=read.table("C:

/23/f.csv",sep=",")

>y=da[,2]

>k=da[,3]

>l=da[,4]

>win.graph(width=3.5,height=3.5,pointsize=8)

>plot(y,k)#plotthescatterofyandk

>plot(y,l)#plotthescatterofyandl

Step2:

PARAMETERESTIMATION

>m1=lm(y~k+l)

>summary(m1)

Call:

lm(formula=y~k+l)

Residuals:

Min1QMedian3QMax

-2113.0-472.9-232.7196.53928.2

Coefficients:

EstimateStd.ErrortvaluePr(>|t|)

(Intercept)588.61734339.389361.7340.09386.

k0.199260.081942.4320.02167*

l11.120213.622673.0700.00473**

---

Signif.codes:

0‘***’0.001‘**’0.01‘*’0.05‘.’0.1‘’1

Residualstandarderror:

1143on28degreesoffreedom

MultipleR-squared:

0.6715,AdjustedR-squared:

0.648

F-statistic:

28.62on2and28DF,p-value:

1.706e-07

Itisconcludedthatthefollowingregressionequation:

Analysisofvariance

>anova(m1)

AnalysisofVarianceTable

Response:

y

DfSumSqMeanSqFvaluePr(>F)

k1624666966246669647.80771.624e-07***

l112311730123117309.42250.004725**

Residuals28365854951306625

---

Signif.codes:

0‘***’0.001‘**’0.01‘*’0.05‘.’0.1‘’1

Residualanalysis

>re1=residuals(m1)

>plot(re1)

Step3:

Resultsanalysis

1.coefficientofdetermination

BecauseofR^2=0.6715,sothefittingeffectisnotgood

2.TESTSOFHYPOTHESES

Agivenlevelofsignificance:

>qf(0.975,2,27)

[1]4.242094

>qt(0.975,27)

[1]2.051831

F=28.62>F(2,27)=4.24

P=1.706e-07<0.05,Showthatk,lcombinedtohaveasignificantlinearimpactony.

T(k)=2.432〉t(27)=2.05;T(l)=3.070〉t(27)=2.05,Showthatk,lofyhassignificantlinearinfluence.

3.Accordingtotheresidualfigure,wecanfindthatasthedatasequence,residualobviousdeviationfromthemean,theincreasescope,showedthatpoorregressionresults.

4.Theregressionequationresidualanalysis

>plot(m1)

Fromtheaboveknowable,deviatingfromthefittinglinesituationisrelativelyserious,canalsobeconcludedthatthefittingeffectisnotgood.

3.2.Model2

Setamodelfor

Thelogarithmictransformation,

Canbeconvertedinto

Step1:

DATAPROCESSING

>y1=log(y)#takelogarithms

>k1=log(k)

>l1=log(l)

Table2:

data(ln)

Serialnumber

Grossvalueofindustrialoutput

lnY

Assetstotal

lnK

Theworkernumber

lnL

(亿元)

(亿元)

(万人)

1

8.222204

8.032107

4.727388

2

7.274147

7.429183

4.204693

3

7.468724

7.916724

4.430817

4

7.280208

7.587726

3.295837

5

8.546616

8.685587

5.78996

6

7.736814

7.47237

4.787492

7

7.204276

6.844922

4.060443

8

6.487334

6.543826

3.433987

9

5.913989

5.895724

2.772589

10

7.371716

7.828831

4.189655

11

6.424399

6.881134

4.060443

12

6.426391

6.246126

3.332205

13

8.395972

8.239042

4.110874

14

8.656785

9.069701

5.537334

15

7.485138

7.936982

4.418841

16

7.125339

7.50022

3.496508

17

6.700362

7.020021

3.7612

18

7.549451

7.626648

4.110874

19

8.214154

8.718191

5.480639

20

8.462293

9.130025

5.402677

21

7.687186

7.960899

4.382027

22

7.839825

7.842133

4.564348

23

8.021896

8.473847

5.402677

24

7.692857

8.088037

5.09375

25

8.58762

9.003277

5.497168

26

8.48357

8.567924

4.976734

27

8.929247

8.92516

4.927254

28

6.766088

6.892154

3.828641

29

8.436285

9.832364

5.384495

30

5.137562

6.41495

2.944439

31

5.785455

7.328562

3.806662

Step2:

Parameterestimation

>m2=lm(log(y)~log(k)+log(l))

>summary(m2)

Call:

lm(formula=log(y)~log(k)+log(l))

Residuals:

Min1QMedian3QMax

-1.20679-0.155170.031790.265320.73927

Coefficients:

EstimateStd.ErrortvaluePr(>|t|)

(Intercept)1.15400.72761.5860.12397

log(k)0.60920.17643.4540.00178**

log(l)0.36080.20161.7900.08432.

---

Signif.codes:

0‘***’0.001‘**’0.01‘*’0.05‘.’0.1‘’1

Residualstandarderror:

0.4255on28degreesoffreedom

MultipleR-squared:

0.8099,AdjustedR-squared:

0.7963

F-statistic:

59.66on2and28DF,p-value:

8.035e-11

Itisconcludedthatthefollowingregressionequation:

(exp(1.1540)=3.170851)

Analysisofvariance

>anova(m2)

AnalysisofVarianceTable

Response:

log(y)

DfSumSqMeanSqFvaluePr(>F)

log(k)121.024921.0249116.10691.805e-11***

log(l)10.58000.58003.20320.08432.

Residuals285.07030.1811

---

Signif.codes:

0‘***’0.001‘**’0.01‘*’0.05‘.’0.1‘’1

Residualanalysis

>re2=residuals(m2)

>plot(re2)

>

Step3:

Resultsanalysis

2.coefficientofdetermination

:

BecauseofR^2=0.8099,Sothefittingeffectisbetterthanmodel1.

3.TESTSOFHYPOTHESES

Agivenlevelofsignificanceis5%,

>qf(0.975,2,27)

[1]4.242094

>qt(0.975,27)

[1]2.051831

F=59.66>F(2,27)=4.24

P=8.035e-11<0.05,ShowthatLNK,LNLcombinedtohaveasignificantlinearimpactonlny

。

T(lnk)=3.454>2.05,T(lnl)=1.790<2.05,LNKparametersthroughthetestofsignificanceofvariables;ButtheparametersoftheLNLfailedtheinspection.

Ifagiven10%significancelevel

>qt(0.95,27)

[1]1.703288

T(lnk)=3.454>1.70;T(lnl)=1.790>1.70,SotheLNK,LNLparametersthroughthetestofsignificanceofvariables.

3.Accordingtotheresidualfigure,wecanfindthatinadditiontothethreeabnormalpointsafter,evenlydistributedaroundthezeroresidual,andvolatility,within0.5regressionresultisgood.

4.Theregressionequationresidualfigure

>plot(m2)

升级会员

升级会员