整理SAP+FI+汇率与外币评估.docx

《整理SAP+FI+汇率与外币评估.docx》由会员分享,可在线阅读,更多相关《整理SAP+FI+汇率与外币评估.docx(24页珍藏版)》请在冰豆网上搜索。

整理SAP+FI+汇率与外币评估

汇率与外币评估

汇率设置:

OC47|OB07,OB08|OC41,SE16:

V_TCURF

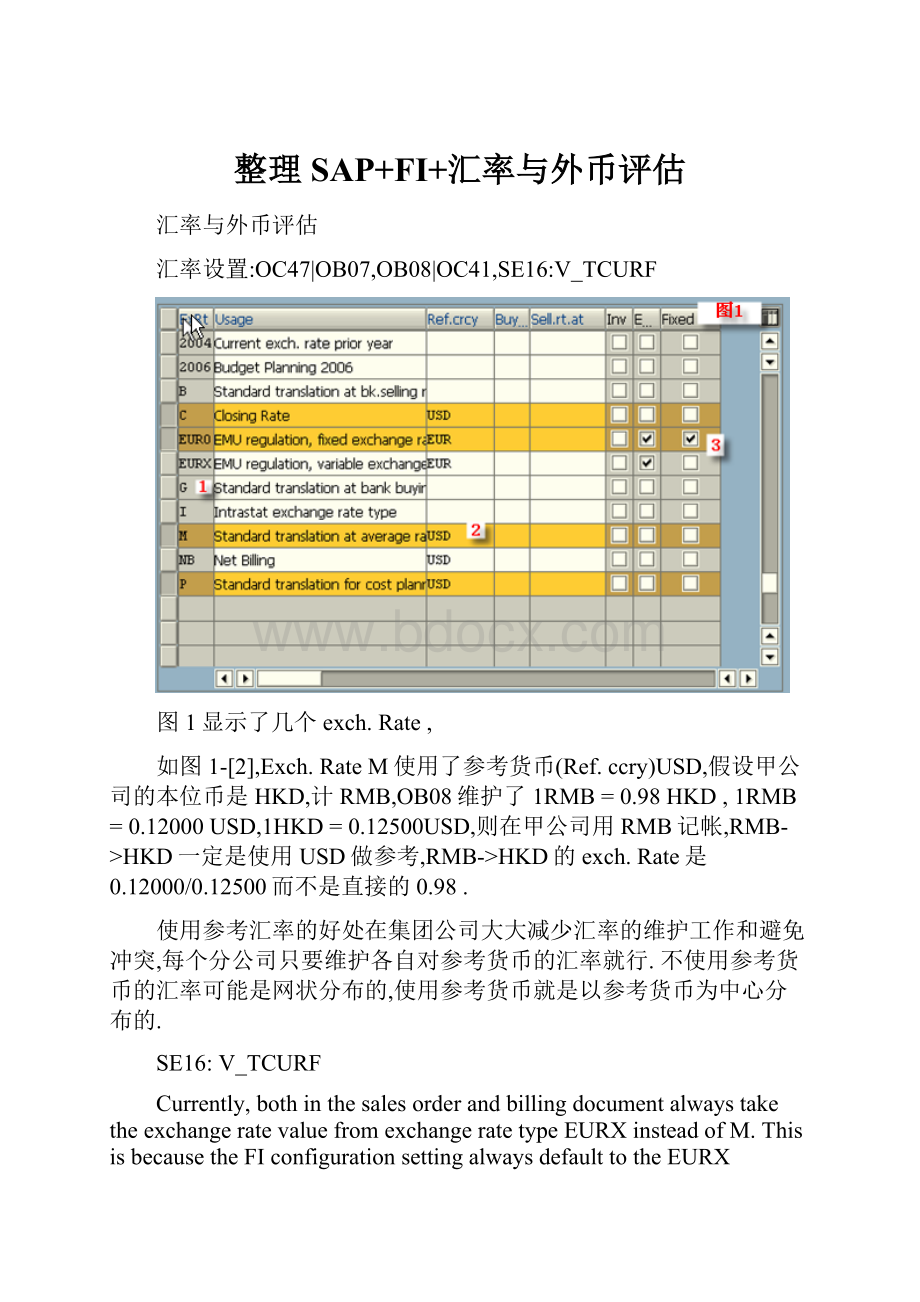

图1显示了几个exch.Rate,

如图1-[2],Exch.RateM使用了参考货币(Ref.ccry)USD,假设甲公司的本位币是HKD,计RMB,OB08维护了1RMB=0.98HKD,1RMB=0.12000USD,1HKD=0.12500USD,则在甲公司用RMB记帐,RMB->HKD一定是使用USD做参考,RMB->HKD的exch.Rate是0.12000/0.12500而不是直接的0.98.

使用参考汇率的好处在集团公司大大减少汇率的维护工作和避免冲突,每个分公司只要维护各自对参考货币的汇率就行.不使用参考货币的汇率可能是网状分布的,使用参考货币就是以参考货币为中心分布的.

SE16:

V_TCURF

Currently,bothinthesalesorderandbillingdocumentalwaystaketheexchangeratevaluefromexchangeratetypeEURXinsteadofM.ThisisbecausetheFIconfigurationsettingalwaysdefaulttotheEURXexchangeratetypeforEUR<->USD,thusitneedtobechangedsoitcantaketheratewiththeexchangeratetypeM.

Inthecurrentsetting,theEURXhasbeendefinedinthecurrencytranslationratioforexchangeratetypeM.TheEURXneedtoberemovedfromcolumn"Alt.ERT"forexchangeratetypeMforcurrencytranslationfromUSD<->EUR.

就是说不使用EURX做EUR<->USD而是使用Mexch.Ratetype,该死的Exch.RateEURX.

外币评估:

OB59,OBA1->KDF|OB09

注意Z001/Z002使用的exch.Rate是C,Z002选上了BalanceValuat.选择.

TMD这个破Balancevalut.是篾意思?

看SAP的帮助

BalanceValuationforOpenItems

Ifyouselectthisparameter,openitemsarebalancedperaccountorgroupandcurrency.Thebalanceisvaluatedaccordingtothevaluationmethod.Thevaluationdifferenceispostedasanexpenseorrevenue(peraccount,onlyrevenueORexpense).

Ifyoudonotselectthisparameter,theopenitemsaresummarizedandvaluatedperreferencenumber.Ifthereisnoreferencenumber,eachlineitemisvaluatedindividually.Thedifferencesthatarisearepostedasanexpenseorrevenue(peraccount,expenseANDrevenue).

Example:

3lineitems:

A,BandC

A Referencenumber1 100USD 190

B Referencenumber1 30-USD 50-

C Noreferencenumber 10USD 15

1)Nobalancevaluation,lowestvalueprinciple,spotexchangerate1.8

Totalfrom A+B 70USD 140DEM Valuationdifference14-DEM

(70*1.8=126 126-140=-14)

C 10USD 15DEM Novaluation,duetolowest

valueprinciple

2)Balancevaluation,lowestvalueprinciple,spotexchangerate1.8

TotalA-C 80USD 155DEM Valuationdifference=11-DEM

(80*1.8=144-155=-11)

Thetotalispostedasanexpense.

3)Nobalancevaluation,revaluationanddevaluation,spotexchange

rate1.8

TotalA+B 70USD 140DEMvaluationdifference 14-DEM

(70*1.8=126 126-140=-14)

C 10USD 15DENvaluationdifference +3DEM

Postings,expense14DEM,revenue3DEM

Z004同Z003唯一不同的是Z004的BalanceValuat.选上了,Z003和Z004是专门重置外币评估的方法

外币评估F.05通常分成2类评估

1.以外币记帐的客户/供应商/总帐未清项(D/K/S)->对所有的未清项进行评估

(余额虽为0,但有未清项)

2.以外币记帐的资产负债表科目(即科目货币非本位币)->对外币余额进行评估

确定评估差异有两种方法:

1.在资产负债表出表日确认并在下月1日冲销

2.在资产负债表出表日确认并更新被评估的未清项,不冲销

未清项的评估是在外币的汇率有变化时,对有涉及外币未清项的科目按统驭科目或科目类型、按币种、分借贷分别进行统计其由于汇率变化产生

的差额,将变化额按科目类型和币种进行帐务调整。

f-03、f-28、f-32你是在做这些记账操作的时候,item中出现valuationaccount吗?

是的,

去查出现此种情况的原会计凭证科目Openitem的moredata中均有valuationdiff金额。

外币评估简单操作.

也就是OpenItemBSEG的这个破BDIFF字段评估后有了差异(如下图).

想一个问题,为什么在F-32,F-44会有类型凭证?

把供应商与客户一起选中执行,结果只产生外币评价凭证未产生相应的回转凭证.抛账会计凭证举例如下:

DR:

F/XLOSS-Unreali*** DR:

ARrev ***

Cr:

ARrevluation*** Cr:

F/Xgain-Unreali***

现在在做冲账动作时,只要产生汇兑损益情况,均会抛出外币评价科目.举例如下:

借:

银行存款 100HKD 112RMB

贷:

应收账款-XXX 100HKD 112RMB

借:

汇兑损失 0HKD xxRMB

贷:

应收账款外币评价0HKD xxRMB

FI-IncorrectExchangeRatedeterminationinForeignCurrencyValuationinF.05

TheEuroLoanisvaluatedmonthlyinCCcurrencyaswellasGroupCurrency.ThedifferencedenotedtheforeignExchangeGain/Lossuponvaluation.TheGLA/c30010010wasvaluedforthisloanon29/01/05.Butthedifferenceappearstobetoohigh.

wondertheformulainstep1whichistorevaluateforeigncurrencytoclosingmonthendrateisnotright.Inmeasuring10MEUR,howcomestep1saysUS$11Mlosswhilestep2saysUS$10Mgain?

Pleaseinvestigate.

ItisnecessarytoinvestigateandclosethisissueASAPasmonthlyclosingisheldupforthis.

F.05

EstimatedMan-day

IfwehaveacloselookatGL30010010forCC5100wefindthatanumberofentrieshavebeenpostedonabackdate.Pls.seetheworksheetbelow.

NowwhentheTransactionF.05wascarriedouton03/21/2005,thepositionoftheGLwasthatTheEURvaluewas10M

EUR,thelocalCurrencyvaluewasalso10MHKDwhiletheUSDvaluewas12,223,092.47allincredit.Atthispoint,the

systemtriedtovaluate10MEUROintoHKDasstep1.ItfoundtheexchangeratefromEURtoHKDusingUSDas

referencecurrencytobe10.16381.Thusthevaluationcameto101.638MHKD.Thebalanceinbookswas10M.soit

postedadifferenceof91.638Mincreditsignifyinganactualliabilityof101.638Mintotal(Documentno.600002097).While

itvaluatedinHKD,italsocarriedoutavaluationinGroupcurrencywhichwasasimpleconversionofHKDtoUSDatthe

Crateexistingonthatdate1HKD=0.12820USD.i.e.HKD91,638,065.52HKD*0.12820=11,748,000.00.Thisitpostedas

aliability.SonowthetotalliabilityinUSDcameto11,748,000.00+originalliability12,223,092.47=23,971,092.47USDor

23.971M.

Sowhenittriedtodoagroupvaluationinstep2itfoundtheactualliabilitytobe10,000,000EUR*1.30300(Exchange

ratefor1EURto1USD)=

13,030,000or13.030MUSD.ButtheGLvaluewas23,971,092.47USD.Soitpostedadebitof23,971,092.47-13,030,000=

10,941,092.47or10.941

MUSD.

Fromthesystempointofviewthereisnomistake.ItcalculatedvaluesasperBalancesexistinginthesystemonaparticular

date.

HencethevariationinGain/LossAccount.

FIChangeF.05Step1andStep2variants

CurrentlyeachentitiesusesthefollowingvariantswhenrunningF.05

/XXXX_STEP1and/XXXX_STEP2whereXXXXisreplacedbytheapplicablecompanycode.

ThesevariantsareprotectedsothattheycanonlybechangedbyuserDANIELLEB.

GlennhasrequestedthatGLaccountsbeginningwith14and20beexcludedfromthevariants.AdditionallytheseGLaccountsshouldberemovedfromtheconfiguraitonwhichisusedinF.05(thiswouldpreventthemfromeverbeingvaluated).

Attachedistheexistingsetupforboth/XXXX_STEP1and/XXXX_STEP2

FIChangeF.05Step1andStep2variants

CurrentlyeachentitiesusesthefollowingvariantswhenrunningF.05

/XXXX_STEP1and/XXXX_STEP2whereXXXXisreplacedbytheapplicablecompanycode.

ThesevariantsareprotectedsothattheycanonlybechangedbyuserDANIELLEB.

GlennhasrequestedthatGLaccountsbeginningwith14and20beexcludedfromthevariants.AdditionallytheseGLaccountsshouldberemovedfromtheconfiguraitonwhichisusedinF.05(thiswouldpreventthemfromeverbeingvaluated).

Attachedistheexistingsetupforboth/XXXX_STEP1and/XXXX_STEP2

F.05的简单操作

1.运行OB08,输入月末汇率

2.运行F.05输入参数如下图所示:

3.这里我选择的是一个客户,真正运行时可以选择客户,供应商,总帐科目,根据评估需要进行选择。

4.执行后如下图所示

5.点击按钮“posting”产生如下图画面

6.运行SM35,可以看到刚刚生成的一个会话

7.执行此会话,如下图选择参数。

8.执行过程中如出现错误,在线更改,或者中止,修改错误后再执行。

不会出现严重错误,因为此会话只是做凭证记账,会计凭证过账常见的错误你们都可以处理的。

为什么清帐时clearingdate被更改了

Issue:

WhileperformingF-32|FB1Dforcustomeropenitemclearing,forexample,wemightcleartheinter-companycustomeropenitemswithUSD(localcurrencyofcompanycode5100isHKD)on02/27/2006,however,wewanttocleartheOIonthepreviousperiod,soweinput02/18/2006.

Thentheissueoccurs,thepostingdateis02/18/2006whiletheclearingdateis02/27/2006.

Then,ifweuseFBL5Ntodisplaycleareditemswithclearingdate,actuallythedataisinconsequent.

ReasonInvestigation

Keywords:

Partialpayment|ResidualPayment

(1)Tcode:

F-32orFB1D

Forexample,ifwechoosepartialpmt,

Thereare3docwithpostingdate02/23/2006,02/18/2006and02/15/2006.

Weusethedocumentpostedin02/23/2006toclearthe2docspostedin02/18/2006and02/15/2006.

Icheckedtheprogram,andfindfinallytheother2docswillusetheclearingdoc’spostingdate02/23/2006asclearingdate.

This’sthegenerateddocument,sincethedocument5100000023postedin02/23/2006hasremainingamount,itisnotaclearingitems.

2.环境价值的度量——最大支付意愿

WithFBL5N,wehavetoinputclearingdate02/23/2006forcleareditemsearch.

二、环境影响评价的要求和内容

(1)规划实施后实际产生的环境影响与环境影响评价文件预测可能产生的环境影响之间的比较分析和评估;

仍以森林为例,营养循环、水域保护、减少空气污染、小气候调节等都属于间接使用价值的范畴。

SAPonlinehelp

(3)评价单元划分应考虑安全预评价的特点,以自然条件、基本工艺条件、危险、有害因素分布及状况便于实施评价为原则进行。

ClearingDate

(3)机会成本法Theclearingdatespecifiesasfromwhentheitemistoberegardedascleared.Whenclearing,thelastpostingdateofallthedocumentsinvolvedinclearingissetastheclearingdate.

Examples

专项规划中的指导性规划 环境影响篇章或说明Invoiceswhichwerepostedon10/10/1997andon10/15/1997areclearedbyapaymentdocumentwhichispostedon11/10/1997.Inthiscasetheclearingdateis11/10/1997,inotherwordsthepostingdateofthepaymentdocument.

1.依法评价原则;ArentalinvoiceforDecemberisenteredon11/28/1997andthepostingdateissetto12/01/1997.Therentispaidon11/30/1997andisalsopostedunderthisdate.12/01/1997isthensetastheclearingdate,inotherwordsthepostingdateoftheinvoice.

Dependencies

Theclearingdateofalineitemisneverallowedtobebeforethepostingdateoftheitem.

Eg.Onlyforpayment,theclearingdateispaymentdate.

(5)阐述划分评价单元的原则、分析过程等。

规划审批机关在审批专项规划草案时,应当将环境影响报告书结论以及审查意见作为决策的重要依据。

一.外币未清项评估原理

1.外币的未清项评估适用范围

1)应收帐款。

2)其他往来应收。

3)应付帐款。

4)应付工资。

5)其他应付。

6)预提费用。

7)借款。

2.原理。

未清项的评估是在外币的汇率有变化时,对有涉及外币未清项的科目按统驭科目或科目类型、按币种、分借贷分别进行统计其由于汇率变化产生的差额,

升级会员

升级会员