亨格瑞管理会计英文第练习答案05.docx

《亨格瑞管理会计英文第练习答案05.docx》由会员分享,可在线阅读,更多相关《亨格瑞管理会计英文第练习答案05.docx(54页珍藏版)》请在冰豆网上搜索。

亨格瑞管理会计英文第练习答案05

CHAPTER5

COVERAGEOFLEARNINGOBJECTIVES

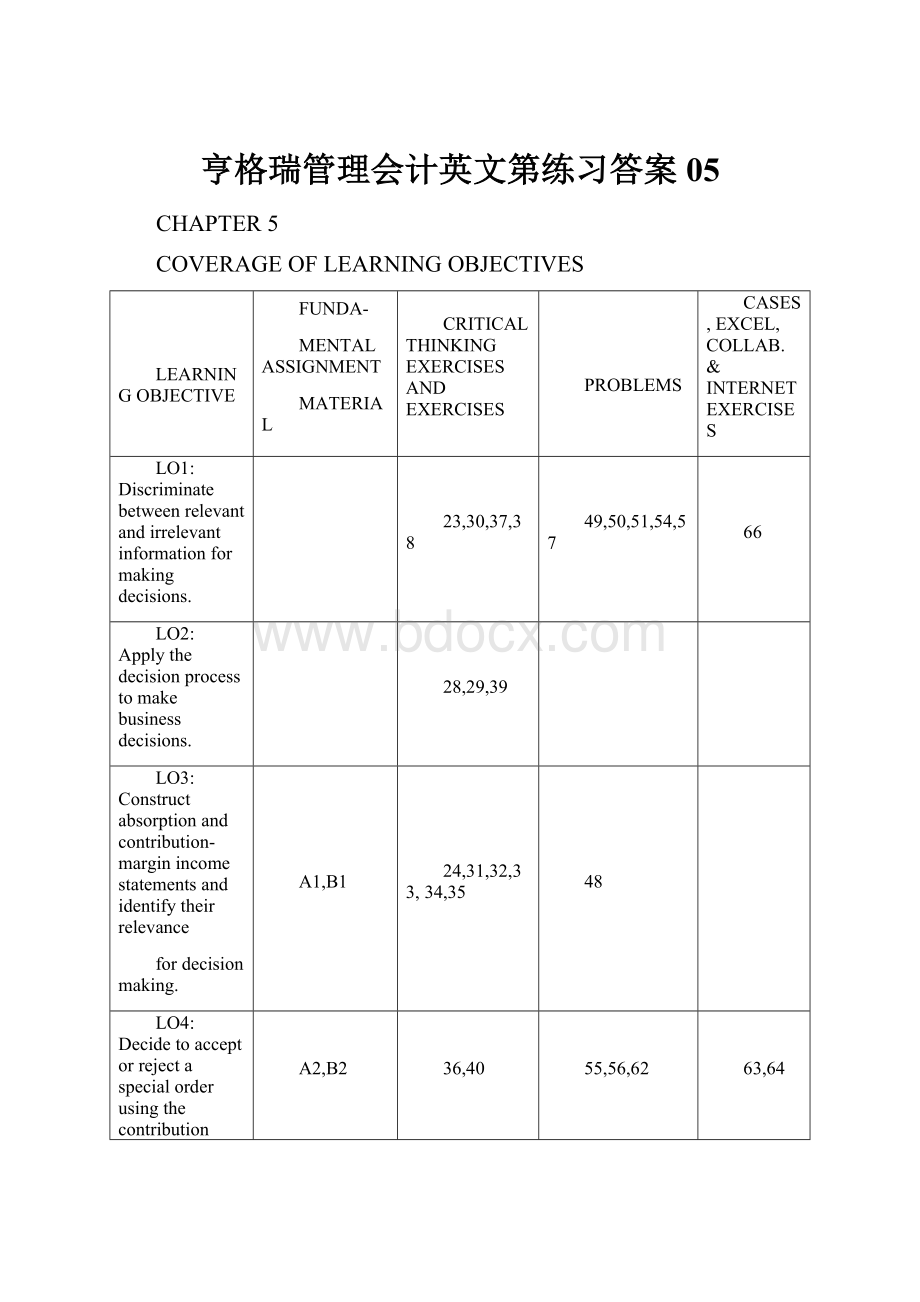

LEARNINGOBJECTIVE

FUNDA-

MENTALASSIGNMENT

MATERIAL

CRITICALTHINKINGEXERCISESANDEXERCISES

PROBLEMS

CASES,EXCEL,COLLAB.&INTERNETEXERCISES

LO1:

Discriminatebetweenrelevantandirrelevantinformationformakingdecisions.

23,30,37,38

49,50,51,54,57

66

LO2:

Applythedecisionprocesstomakebusinessdecisions.

28,29,39

LO3:

Constructabsorptionandcontribution-marginincomestatementsandidentifytheirrelevance

fordecisionmaking.

A1,B1

24,31,32,33,34,35

48

LO4:

Decidetoacceptorrejectaspecialorderusingthecontributionmargintechnique.

A2,B2

36,40

55,56,62

63,64

LO5:

Explainwhypricingdecisionsdependonthecharacteristicsofthemarket.

A2,B2

25,42

58

LO6:

Identifythefactorsthatinfluencepricingdecisionsinpractice.

26,41

47,52,53

65

LO7:

Computeatargetsalespricebyvariousapproaches,andcomparetheadvantagesanddisadvantagesoftheseapproaches.

A3

43,44

LO8:

Usetargetcostingtodecidewhethertoaddanewproduct.

A4,B3

27,45,46

59,60,61

CHAPTER5

RelevantInformationforDecisionMakingwithaFocusonPricingDecisions

5-A1(40-50min.)

1.INDEPENDENCECOMPANY

ContributionIncomeStatement

FortheYearEndedDecember31,2009

(inthousandsofdollars)

Sales$2,200

Lessvariableexpenses

Directmaterial$400

Directlabor330

Variablemanufacturingoverhead(Schedule1)150

Totalvariablemanufacturingcostof

goodssold$880

Variablesellingexpenses80

Variableadministrativeexpenses25

Totalvariableexpenses985

Contributionmargin$1,215

Lessfixedexpenses:

Fixedmanufacturingoverhead(Schedule2)$345

Sellingexpenses220

Administrativeexpenses119

Totalfixedexpenses684

Operatingincome$531

INDEPENDENCECOMPANY

AbsorptionIncomeStatement

FortheYearEndedDecember31,2009

(inthousandsofdollars)

Sales$2,200

Lessmanufacturingcostofgoodssold:

Directmaterial$400

Directlabor330

Manufacturingoverhead(Schedules1and2)495

Totalmanufacturingcostofgoodssold1,225

Grossmargin$975

Less:

Sellingexpenses$300

Administrativeexpenses144444

Operatingincome$531

INDEPENDENCECOMPANY

SchedulesofManufacturingOverhead

FortheYearEndedDecember31,2009

(inthousandsofdollars)

Schedule1:

VariableCosts

Supplies$20

Utilities,variableportion40

Indirectlabor,variableportion90$150

Schedule2:

FixedCosts

Utilities,fixedportion$15

Indirectlabor,fixedportion50

Depreciation200

Propertytaxes20

Supervisorysalaries60345

Totalmanufacturingoverhead$495

2.Changeinrevenue$200,000

Changeintotalcontributionmargin:

Contributionmarginratioinpart1

is$1,215÷$2,200=.552

Ratiotimesdecreaseinrevenueis.552×$200,000$110,400

Operatingincomebeforechange531,000

Newoperatingincome$420,600

Thisanalysisisreadilydonebyusingdatafromthecontributionincomestatement.Incontrast,thedataintheabsorptionincomestatementmustbeanalyzedandsplitintovariableandfixedcategoriesbeforetheeffectonoperatingincomecanbeestimated.

5-A2(25-30min.)

1.Acontributionformat,whichissimilartoExhibit5-6,clarifiestheanalysis.

WithoutWith

SpecialEffectofSpecial

OrderSpecialOrderOrder

Units2,000,000150,0002,150,000

TotalPerUnit

Sales$11,000,000$660,000$4.401$11,660,000

Lessvariableexpenses:

Manufacturing$3,500,000$322,500$2.152$3,822,500

Selling&administrative800,00035,250.2353835,250

Totalvariableexpenses$4,300,000$357,750$2.385$4,647,250

Contributionmargin$6,700,000$302,250$2.015$7,002,250

Lessfixedexpenses:

Manufacturing$3,000,00000.00$3,000,000

Selling&administrative2,200,00000.002,200,000

Totalfixedexpenses$5,200,00000.00$5,200,000

Operatingincome$1,500,000$302,250$2.015$1,802,250

1$660,000÷150,000=$4.40

2Regularunitcost=$3,500,000÷2,000,000=$1.75

Logo.40

Variablemanufacturingcosts$2.15

3Regularunitcost=$800,000÷2,000,000=$.40

Lesssalescommissionsnotpaid(3%of$5.50)(.165)

Regularunitcost,excludingsalescommission$.235

2.Operatingincomefromselling7.5%moreunitswouldincreaseby$302,250÷$1,500,000=20.15%.Notealsothattheaveragesellingpriceonregularbusinesswas$5.50.Thefullcost,includingsellingandadministrativeexpenses,was$4.75.The$4.75,plusthe40¢perlogo,lesssavingsincommissionsof.165¢cameto$4.985.Thepresidentapparentlywanted$4.985+.08($4.985)=$4.985+.3988=$5.3838perpen.

Moststudentswillprobablycriticizethepresidentforbeingtoostubborn.Thecosttothecompanywastheforgoingof$302,250ofincomeinordertoprotectthecompany'simageandgeneralmarketposition.Whether$302,250wasawiseinvestmentinthefutureisajudgmentthatmanagersarepaidforrendering.

5-A3(15-20min.)

Thepurposeofthisproblemistounderscoretheideathatanyofanumberofgeneralformulasmightbeusedthat,properlyemployed,wouldachievethesametargetsellingprices.Desiredsales=$7,500,000+$1,500,000=$9,000,000.

Thetargetmarkuppercentagewouldbe:

1.100%ofdirectmaterialsanddirectlaborcostsof$4,500,000.

Computationis:

($9,000,000-$4,500,000)÷$4,500,000=100%

2.50%ofthefullcostofjobsof$6,000,000.

Computationis:

($9,000,000-$6,000,000)÷$6,000,000=50%

3.[$9,000,000–($3,500,000+$1,000,000+$700,000)]÷$5,200,000=73.08%

4.($9,000,000-$7,500,000)÷$7,500,000=20%

5.[$9,000,000–($3,500,000+$1,000,000+$700,000+$500,000)]÷$5,700,000=$3,300,000÷$5,700,000=57.9%

Ifthecontractorisunabletomaintaintheseprofitpercentagesconsistently,thedesiredoperatingincomeof$1,500,000cannotbeobtained.

5-A4(15-20minutes)

1.Revenue($360×70,000)$25,200,000

Totalcostoverproductlife16,000,000

Estimatedcontributiontoprofit$9,200,000

Desired(target)contributiontoprofit

40%×$25,200,00010,080,000

Deficiencyinprofit$880,000

Theproductshouldnotbereleasedtoproduction.

2.Previoustotalestimatedcost$16,000,000

Costsavingsfromsuppliers

.20×.70×$8,000,0001,120,000

Revisedtotalestimatedcost$14,880,000

Revisedtotalcontributiontoprofit:

$25,200,000-$14,880,000$10,320,000

Desired(target)contributiontoprofit10,080,000

Excesscontributiontoprofit$240,000

Theproductshouldbereleasedtoproduction.

3.Previousrevisedtotalestimatedcostfrom

requirement2.$14,880,000

Processimprovementsavings:

.25×.30×$8,000,000$600,000

Lesscostofnewtechnology220,000380,000

Revisedtotalestimatedcost14,500,000

Revisedtotalcontributiontoprofit:

$25,200,000-$14,500,000$10,700,000

Desired(target)contributiontoprofit10,080,000

Excesscontributiontoprofit$620,000

Theproductshouldbereleasedtoproduction.

5-B1(40-50min.)

1.KINGLANDMANUFACTURING

ContributionIncomeStatement

FortheYearEndedDecember31,2009

(Inthousandsofdollars)

Sales$13,000

Lessvariableexpenses:

Directmaterial$4,000

Directlabor2,000

Variableindirectmanufacturing

costs(Schedule1)960

Totalvariablemanufacturingcostofgoodssold$6,960

Variablesellingexpenses:

Salescommissions$500

Shippingexpenses300800

Variableclericalsalaries400

Totalvariableexpenses8,160

Contributionmargin$4,840

Lessfixedexpenses:

Manufacturing(Schedule2)$702

Selling(advertising)400

Administrative-executivesalaries100

Totalfixedexpenses1,202

Operatingincome$3,638

KINGLANDMANUFACTURING

AbsorptionIncomeStatement

FortheYearEndedDecember31,2009

(Inthousandsofdollars)

Sales$13,000

Lessmanufacturingcostofgoodssold:

Directmaterial$4,000

Directlabor2,000

Indirectmanufacturingcosts

(Schedules1and2)1,6627,662

Grossprofit5,338

Sellingexpenses:

Salescommissions$500

Advertising400

Shippingexpenses300$1,200

Administrativeexpenses:

Executivesalaries$100

Clericalsalaries4005001,700

Operatingincome$3,638

KINGLANDMANUFACTURING

Schedules1and2

IndirectManufacturingCosts

FortheYearEndedDecember31,2009

(Inthousandsofdollars)

Schedule1:

VariableCosts

Cuttingbits$60

Abrasivesformachining100

Indirectlabor800$960

Schedule2:

FixedCosts

Factorysupervisors'salaries$100

Factorymethodsresearch40

Long-termrent,factory100

Fireinsuranceonequipment2

Propertytaxesonequipment30

Depreciationonequipment400

Factorysuperintendent'ssalary30702

Totalindirectmanufacturingcosts$1,662

2.Operatingincomewoulddecreasefrom$3,638,000to$3,268,000:

Decreaseinrevenue$1,000,000

Decreaseintotalcontributionmargin*:

Ratiotimesrevenueis.37×$1,000,000$370,000

Decreaseinfixedexpenses0

Operatingincomebeforeincrease3,638,000

Newoperatingincome$3,268,000

*Contributionmarginratioincontributionincomestatementis$4,840÷$13,000=.37(rounded).

Theaboveanalysisisreadilycalculatedbyusingdatafromthecontributionincomestatement.Incontrast,thedataintheabsorptionincomestatementmustbeanalyzedanddividedintovariableandfixedcategoriesbeforetheeffectonoperatingincomecanbeestimated.

5-B2(30-40min.)

1.DANUBECOMPANY

IncomeStatement

FortheYearEndedDecember31,20X0

TotalPerUnit

Sales$40,000,000$20.00

Lessvariableexpenses:

Manufacturing$18,000,000

Selling&administrative9,000,00027,000,00013.50

Contributionmargin$13,000,000$6.50

升级会员

升级会员