原创R语言TMA三均线策略实现附代码数据.docx

《原创R语言TMA三均线策略实现附代码数据.docx》由会员分享,可在线阅读,更多相关《原创R语言TMA三均线策略实现附代码数据.docx(36页珍藏版)》请在冰豆网上搜索。

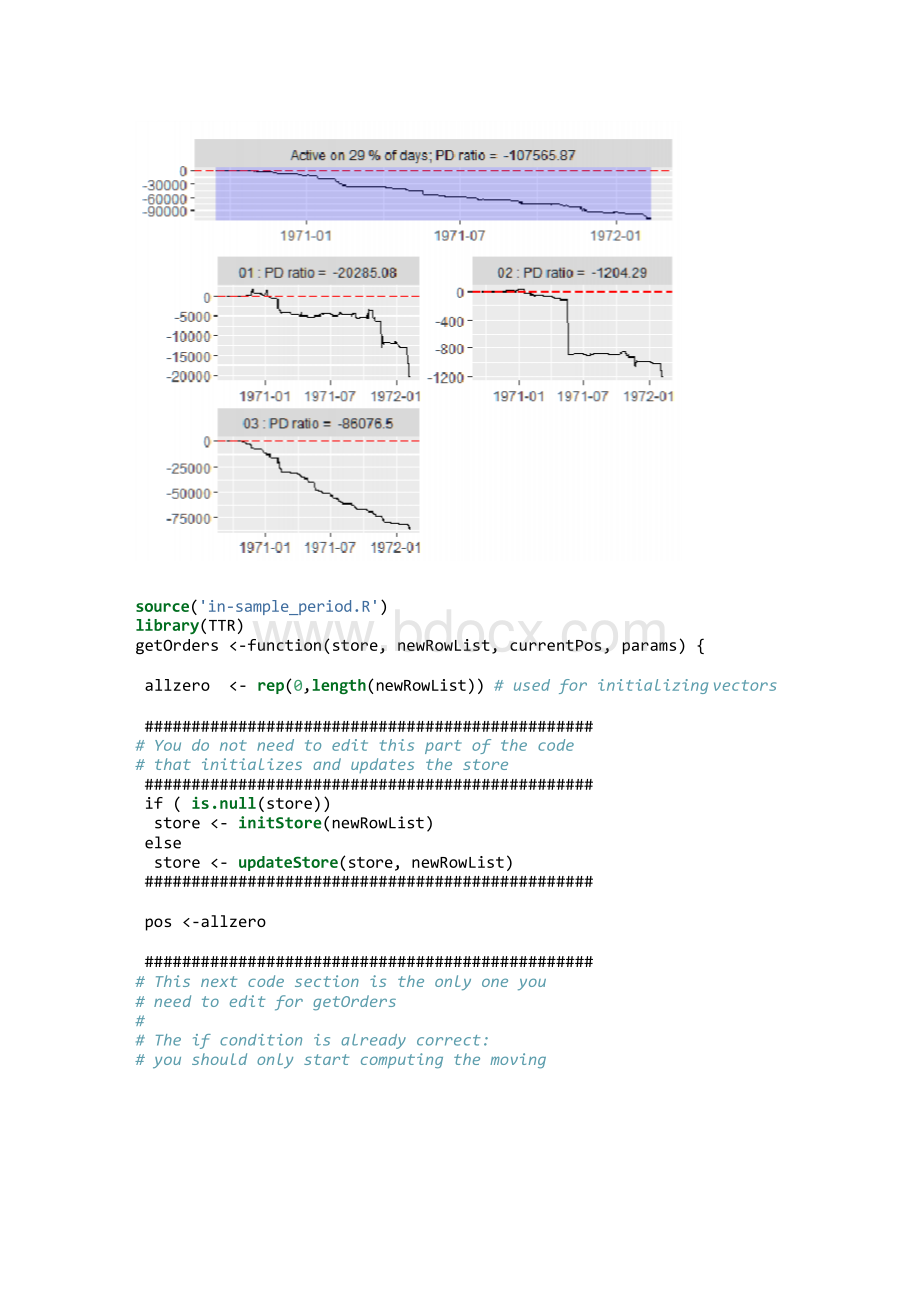

source('in-sample_period.R')library(TTR)

getOrders<-function(store,newRowList,currentPos,params){allzero <-rep(0,length(newRowList))#usedforinitializingvectors

################################################

#Youdonotneedtoeditthispartofthecode#thatinitializesandupdatesthestore

################################################

if(is.null(store))

store<-initStore(newRowList)else

store<-updateStore(store,newRowList)################################################

pos<-allzero################################################

#Thisnextcodesectionistheonlyoneyou#needtoeditforgetOrders

#

#Theifconditionisalreadycorrect:

#youshouldonlystartcomputingthemoving

#averageswhenyouhaveenoughcloseprices#forthelongmovingaverage

################################################

if(store$iter>params$lookbacks$long){

for(indexin 1:

length(params$series)){current_close= last(store$cl[[index]])close=store$cl[[index]]

xtsclose= as.xts(close)

GETtma= getTMA(xtsclose,params$lookbacks)

pos= getPosSignFromTMA(GETtma)*getPosSize(current_close)

}

}################################################

#Youdonotneedtoeditthispartofthecode#thatinitializesandupdatesthestore

################################################

marketOrders<--currentPos+pos

return(list(store=store,marketOrders=marketOrders,limitOrders1=allzero,limitPrices1=allzero,limitOrders2=allzero,limitPrices2=allzero))

}

########################################################################

#Thefollowingfunctionshouldbeeditedtocompletesteps1to3#ofcomp22assignment2

getTMA<-function(close_prices,lookbacks){

if(!

("long" %in% names(lookbacks)&&"short" %in% names(lookbacks)&&"medium" %in% names(lookbacks)))

stop("E01:

Atleastoneof\"short\",\"medium\",\"long\"ismissingfromnames(lookbacks)")

#ReplaceTRUEto

#checkthattheelementsoflookbacksareallintegers

if(!

(class(lookbacks[[1]])=="integer"&&class(lookbacks[[2]])=="integer"&&class(lookbacks[[3]])=="integer"))

stop("E02:

Atleastoneofthelookbacksisnotanintegeraccordingtois.integer()")

#ReplaceTRUEto

#checkthatlookbacks$shortif(!

(lookbacks[[1]]stop("E03:

Thelookbacksdonotsatisfylookbacks$shortium#ReplaceTRUEto

#checkthatclose_pricesisanxts

if(!

(class(close_prices)[1]=="xts"))

stop("E04:

close_pricesisnotanxtsaccordingtois.xts())"

#ReplaceTRUEto

#checkthatclose_priceshasenoughrows

if(nrow(close_prices)stop("E05:

close_pricesdoesnotenoughrows)"

#ReplaceTRUEto

#checkthatclose_pricescontainsacolumncalled"Close"

if(!

(colnames(close_prices)=="Close"))

stop("E06:

close_pricesdoesnotcontainacolumn\"Close\")"

sma=numeric(0)for(iin1:

3){

sma[i]<-as.numeric(last(SMA(close_prices,n=lookbacks[[i]])))#TTRversion#converttovectorfromxts

}

smalist<-list(short=sma[1],medium=sma[2],long=sma[3])

#Youneedtoreplacetheassignmenttoretsothatthe#returnedobject:

# -isalist

# -hastherightnames(short,medium,long),and# -containsnumericandnotxtsobjects

# -andcontainsthecorrectmovingaveragevalues,whichshould# havewindowsofthecorrectsizeswhichshouldallendinthe# sameperiodwhichshouldbethelastrowofclose_prices

return(smalist)

}

getPosSignFromTMA<-function(tma_list){if(tma_list$short=1

elseif(tma_list$long>tma_list$medium&&tma_list$medium>tma_list$short)ret=-1

elseret=0

return(ret)

}

getPosSize<-function(current_closec,onstant=1000){

return(floor(constant/current_close))

}

getInSampleResult<-function(){TIme=getInSamplePeriod('x1xxx')dataList<-getData(directory="A2")

dataList<-lapply(dataList,function(x)x[TIme[1]:

TIme[2]])

lookbacks<-list(short=as.integer(5),medium=as.integer(10),long=as.integer(20))

sMult<-0.2#slippagemultiplier

newRowList=getRowList(dataList,1)numOfSeries=length(dataList)

params<-list(lookbacks=lookbacks,sdParam=1,series=1:

numOfSeries)#,posSizes=rep(1,getPosSize(newRowList[[1]]$Close)))

results<-backtest(dataList,getOrders,params,sMult)pfolioPnL<-plotResults(dataList,results)pfolioPnL$fitAgg

cat("PDratio",pfolioPnL$fitAgg)

}

getInSampleOptResult<-function(){sMult<-0.2#slippagemultiplierTIme=getInSamplePeriod('x4wl1')#####dataList<-getData(directory="A2")

dataList<-lapply(dataList,function(x)x[TIme[1]:

TIme[2]])sMult<-0.2#slippagemultiplier

numOfSeries=length(dataList)medium<-seq(from=105,to=120,by=5)short<-seq(from=100,to=110,by=5)long<-

升级会员

升级会员