会计学企业决策的基础答案.docx

《会计学企业决策的基础答案.docx》由会员分享,可在线阅读,更多相关《会计学企业决策的基础答案.docx(24页珍藏版)》请在冰豆网上搜索。

会计学企业决策的基础答案

管理会计作业(chapter16-20)

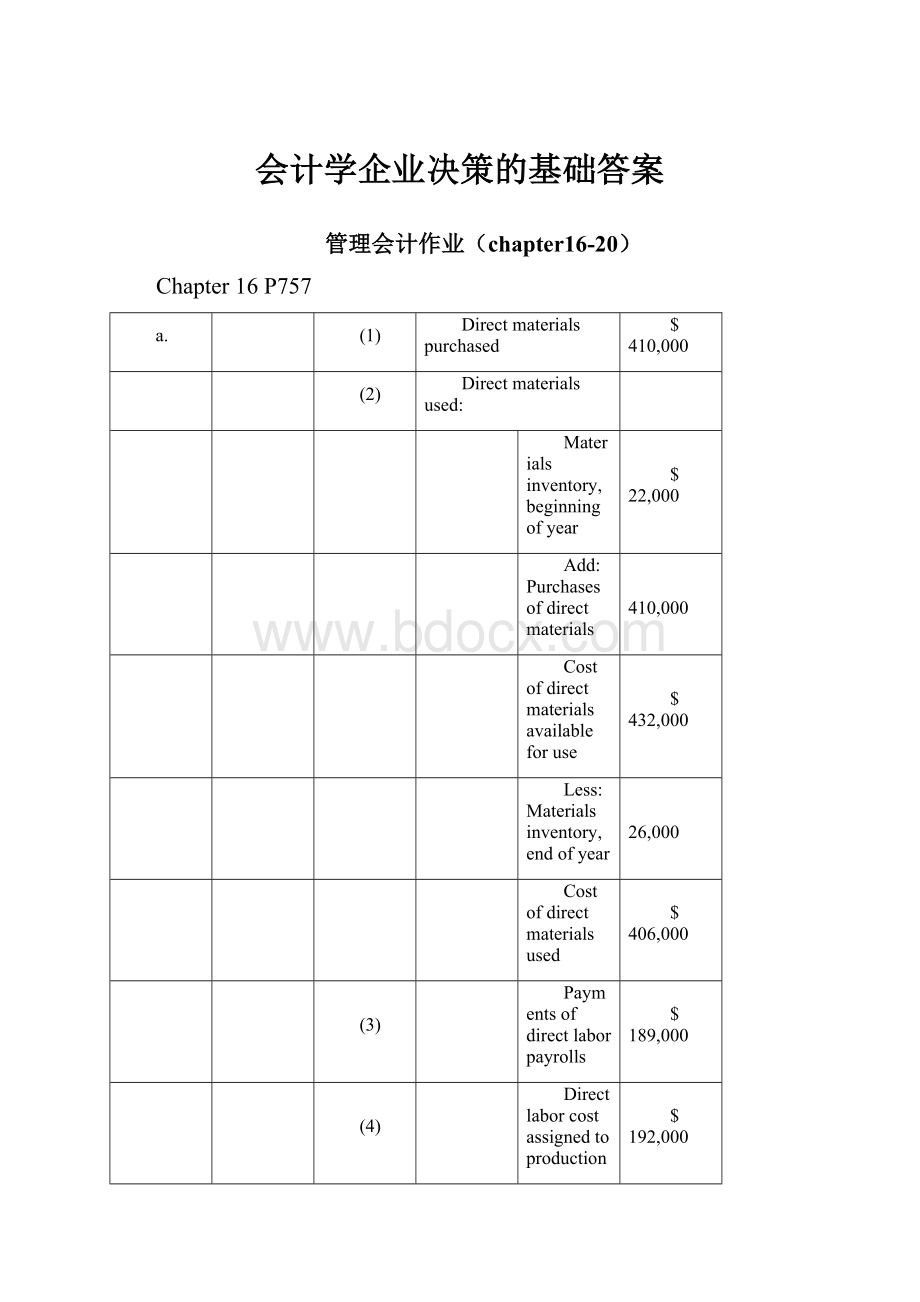

Chapter16P757

a.

(1)

Directmaterialspurchased

$410,000

(2)

Directmaterialsused:

Materialsinventory,beginningofyear

$22,000

Add:

Purchasesofdirectmaterials

410,000

Costofdirectmaterialsavailableforuse

$432,000

Less:

Materialsinventory,endofyear

26,000

Costofdirectmaterialsused

$406,000

(3)

Paymentsofdirectlaborpayrolls

$189,000

(4)

Directlaborcostassignedtoproduction

$192,000

(5)

Totalmanufacturingcosts:

Directmaterialsused[parta

(2)]

$406,000

Directlaborcost

192,000

Manufacturingoverhead

393,600

Totalmanufacturingcosts

$991,600

(6)

Costoffinishedgoodsmanufactured:

Workinprocessinventory,beginningofyear

$5,000

Add:

Totalmanufacturingcosts[parta(5)]

991,600

Costofallgoodsinprocessduringtheyear

$996,600

Less:

Workinprocessinventory,endofyear

9,000

Costoffinishedgoodsmanufactured

$987,600

(7)

Costofgoodssold:

Beginninginventoryoffinishedgoods

$38,000

Add:

Costoffinishedgoodsmanufactured[parta(6)]

987,600

Costofgoodsavailableforsale

$1,025,600

Less:

Endinginventoryoffinishedgoods

25,000

Costofgoodssold

$1,000,600

(8)

Totalinventory:

Materialsinventory

$26,000

Workinprocessinventory

9,000

Finishedgoodsinventory

25,000

Totalinventory

$60,000

b.

HILLSDALEMANUFACTURINGCORP.

ScheduleoftheCostofFinishedGoodsManufactured

FortheYearEndedDecember31,20__

Workinprocessinventory,beginningofyear

$5,000

Add:

Manufacturingcostsassignedtoproduction:

Directmaterialsused[parta

(2)]

$406,000

Directlabor

192,000

Manufacturingoverhead

393,600

Totalmanufacturingcosts

991,600

Costofallgoodsinprocessduringtheyear

$996,600

Less:

Workinprocess,endofyear

9,000

Costoffinishedgoodsmanufactured

$987,600

Chapter16P761

a.

Purchasesofdirectmaterials

$360,000

b.

Costofdirectmaterialsused:

Materialsinventory,beginningofyear

$18,000

Add:

Purchasesofdirectmaterials

360,000

Costofmaterialsavailableforuse

$378,000

Less:

Materialsinventory,endofyear

14,000

Costofdirectmaterialsused

$364,000

c.

Directlaborpayrollspaidduringtheyear

$225,000

d.

Directlaborcostsassignedtoproduction

$230,000

e.

Overheadcostsduringtheyear

$400,000

Unitsintheactivitybase(directlaborcosts)

230,000

Overheadstatedasapercentageofdirectlaborcosts

($400,000÷$230,000)

174%

f.

Directmaterialsused(partb)

$364,000

Directlaborcostsassignedtoproduction

230,000

Manufacturingoverheadappliedtoproduction

400,000

Totalmanufacturingcostschargedtoworkinprocess

$994,000

g.

Costsoffinishedgoodsmanufactured:

Workinprocessinventory,beginningofyear

$20,000

Add:

Totalmanufacturingcosts(partf)

994,000

Costofallgoodsinprocessduringtheyear

$1,014,000

Less:

Costofworkinprocessinventory,endofyear

25,000

Costoffinishedgoodsmanufactured

$989,000

h.

Costofgoodssold:

Beginninginventoryoffinishedgoods

$98,000

Add:

Costoffinishedgoodsmanufactured(partg)

989,000

Costofgoodsavailableforsale

$1,087,000

Less:

Endinginventoryoffinishedgoods

110,000

Costofgoodssold

$977,000

i.

Totalinventoryatyear-end:

Materialsinventory

$14,000

Workinprocessinventory

25,000

Finishedgoodsinventory

110,000

Totalinventory

$149,000

Chapter17P802

a.

DepartmentOneoverheadapplicationratebasedonmachine-hours:

ManufacturingOverhead

=

$420,000

=

$35permachine-hour

Machine-Hours

12,000

DepartmentTwooverheadapplicationratebasedondirectlaborhours:

ManufacturingOverhead

=

$337,500

=

$perdirectlaborhour

DirectLaborHours

15,000

b.

Jobno.58:

Dept.One

Dept.Two

Total

Directmaterials

$10,100

$7,600

$17,700

Directlabor

16,500

11,100

27,600

Manufacturingoverhead:

750machine-hours×$35perhour

26,250

26,250

740directlaborhours×$perhour

16,650

16,650

Totalcostofjobno.58

$88,200

c.

GeneralJournal

CostofGoodsSold

88,200

FinishedGoodsInventory

88,200

Torecordcostofgoodssold(jobno.58)

toCityFurniture.

AccountsReceivable(CityFurniture)

147,000

Sales

147,000

TorecordrevenuefromsaletoCityFurniture.

d.

Dept.One

Dept.Two

ActualmanufacturingoverheadforJanuary

$39,010

$26,540

Manufacturingoverheadappliedtojobs:

1,100machine-hours×$35perhour

38,500

1,200directlaborhours×$perhour

27,000

Underappliedmanufacturingoverhead—Dept.One

$510

Overappliedmanufacturingoverhead—Dept.Two

$460

Chapter17P805

a.

Budgetedmanufacturingoverhead

$24,600

Budgeteddirectlaborhours(DLH)

÷2,500

Manufacturingoverheadapplicationrate

$

perDLH

ManufacturingoverheadallocatedusingDLH

BasicChunks

CustomCuts

50,000bags×DLHperbag×$perDLH

$4,920

20,000cases×DLHpercase×$perDLH

$19,680

b.

Percentofcostdriverassignedtoeachproductline

BasicChunks

CustomCuts

Kilowatthours:

BasicChunks(90,000KWH÷100,000KWH)

90%

CustomCuts(10,000KWH÷100,000KWH)

10%

Machinehours:

BasicChunks(160MH÷200NH)

80%

CustomCuts(40MH÷200MH)

20%

Squarefeetoccupied:

BasicChunks(60,000Sq.Ft.÷80,000Sq.Ft.)

75%

CustomCuts(20,000Sq.Ft.÷80,000Sq.Ft.)

25%

Directlaborhours:

BasicChunks(500DLH÷2,500DLH)

20%

CustomCuts(2,000DLH÷2,500DLH)

80%

ManufacturingoverheadallocatedusingABC

BasicChunks

CustomCuts

Utilitiescostpool(usingKWHasacostdriver):

BasicChunks(90%×$8,000)

$7,200

CustomCuts(10%×$8,000)

$800

Maintenancecostpool(usingMHasacostdriver):

BasicChunks(80%×$1,000)

$800

CustomCuts(20%×$1,000)

$200

Depreciationcostpool(usingSq.Ft.asacostdriver):

BasicChunks(75%×$15,000)

$11,250

CustomCuts(25%×$15,000)

$3,750

Miscellaneouscostpool(usingDLHasacostdriver):

BasicChunks(20%×$600)

$120

CustomCuts(80%×$600)

$480

TotaloverheadallocatedtoeachproductlineusingABC

$19,370

$5,230

c.

Totalmanufacturingcostsallocatedtoeachproductline

BasicChunks

CustomCuts

DirectLabor:

BasicChunks(50,000bags×$12perDLH×DLH)

$6,000

CustomCuts(20,000cases×$12perDLH×DLH)

$24,000

DirectMaterials:

BasicChunks(50,000bags×$2perbag)

$100,000

CustomCuts(20,000cases×$4percase)

$80,000

ManufacturingOverhead(allocateusingABC):

BasicChunks(frompartb)

$19,370

CustomCuts(frompartb)

$5,230

TotalcostallocatedusingABC

$125,370

$109,230

d.

TheCustomCutsproductlineisverylaborintensiveincomparisontotheBasicChunksproductline.Thus,thecompany’scurrentpracticeofusingdirectlaborhourstoallocateoverheadresultsintheassignmentofadisproportionateamountoftotaloverheadtotheCustomCutsproductline.Ifpricingdecisionsaresetasafixedpercentageabovethemanufacturingcostsassignedtoeachproduct,theCustomCutsproductlineisoverpricedinthemarketplacewhereastheBasicChunksproductlineiscurrentlypricedatanartificiallylowpriceinthemarketplace.ThisprobablyexplainswhysalesofBasicChunksremainstrongwhilesalesofCustomCutsareonthedecline.

e.

Thebenefitsthecompanywouldachievebyimplementinganactivity-basedcostingsysteminclude:

(1)abetteridentificationofitsoperatinginefficiencies,

(2)abetterunderstandingofitsoverheadcoststructure,(3)abetterunderstandingoftheresourcerequirementsofeachproductline,(4)thepotentialtoincrease

升级会员

升级会员