上海对外贸易学院财管中加财务报表分析课后练习答案cha3 cha4.docx

《上海对外贸易学院财管中加财务报表分析课后练习答案cha3 cha4.docx》由会员分享,可在线阅读,更多相关《上海对外贸易学院财管中加财务报表分析课后练习答案cha3 cha4.docx(23页珍藏版)》请在冰豆网上搜索。

上海对外贸易学院财管中加财务报表分析课后练习答案cha3cha4

Cha3

5.{L}a.(i)

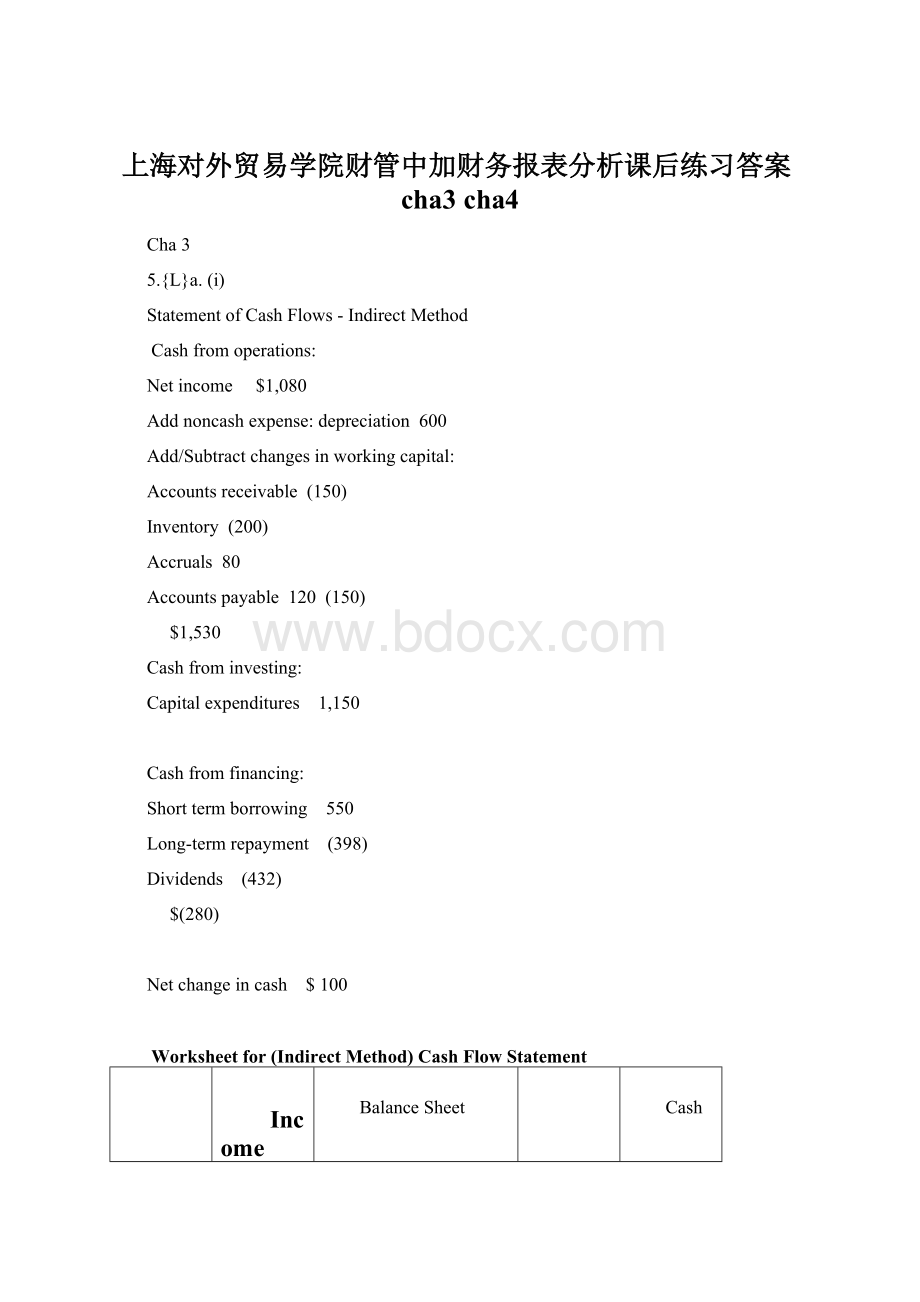

StatementofCashFlows-IndirectMethod

Cashfromoperations:

Netincome$1,080

Addnoncashexpense:

depreciation600

Add/Subtractchangesinworkingcapital:

Accountsreceivable(150)

Inventory(200)

Accruals80

Accountspayable120(150)

$1,530

Cashfrominvesting:

Capitalexpenditures1,150

Cashfromfinancing:

Shorttermborrowing550

Long-termrepayment(398)

Dividends(432)

$(280)

Netchangeincash$100

Worksheetfor(IndirectMethod)CashFlowStatement

Income

BalanceSheet

Cash

Statement

12/31/00

12/31/01

Change

Effect

Netincome

$1,080

$1,080

Depreciation

600

600

Accountsreceivable

$1,500

$1,650

$150

(150)

Inventory

2,000

2,200

200

(200)

Accruals

800

880

80

80

Accountspayable

1,200

1,320

120

120

Depreciation

(600)

(600)

Netfixedassets

6,500

7,050

550

(550)

Capitalexpenditures

$(1,150)

Notepayable

5,500

6,050

550

550

Short-termborrowing

$550

Long-termdebt

2,000

1,602

(398)

(398)

Long-termdebtrepayment

$(398)

Netincome

(1,080)

(1,080)

Retainedearnings

500

1,148

648

648

Dividendspaid

$(432)

_________

______

0

$100

Theworksheettocreatethecashflowstatementispresentedabove.Eachbalancesheetchange(otherthancash)isaccountedforandmatchedwithitscorrespondingactivity.Asalastcheck,thenetincomeandtheadd-backsofnon-cashitemsarebalancedand“closed”totheirrespectiveaccounts(PP&Eandretainedearnings)providingtheamountsofcapitalexpendituresanddividends.

a.(ii)StatementofCashFlows-DirectMethod

CashfromOperations:

Cashcollections$9,850

Cashpaymentsformerchandise(6,080)

CashpaidforSG&A(920)

Cashpaidforinterest(600)

Cashpaidfortaxes(720)

$1,530

CashforInvestingActivities:

Capitalexpenditures(1,150)

CashforFinancingActivities:

Short-termborrowing550

Long-termdebtrepayment(398)

Dividends(432)

$(280)

NetChangeinCash$100

Theworksheettocreatethecashflowstatementispresentedbelow.Eachbalancesheetchange(otherthancash)isaccountedforandmatchedwithitscorrespondingactivity.Furthermoretheoperatingaccountchangesarematchedtotheircorrespondingincomestatementitem.Asalastcheck,thenetincomeisbalancedand“closed”toretainedearningsprovidingtheamountofdividends.

Notethatthereisnodifferencebetweentheindirectanddirectmethodsinthecashflowstatementandintheworksheetforcashforinvestingandfinancingactivities,

Worksheetfor(DirectMethod)CashFlowStatement

Income

BalanceSheet

Cash

Statement

12/31/00

12/31/01

Change

Effect

Sales

$10,000

$10,000

Accountsreceivable

$1,500

$1,650

$150

(150)

CashCollections

$9,850

COGS

(6,000)

(6,000)

Inventory

2,000

2,200

200

(200)

Accountspayable

1,200

1,320

120

120

CashPaidforMerchandise

$(6,080)

SG&Aexpense

(1,000)

(1,000)

Accruals

800

880

80

80

CashPaidforSG&A

$(920)

Interestexpense

(600)

(600)

CashPaidforInterest

$(600)

Taxes

(720)

(720)

CashPaidforTaxes

$(720)

Depreciation

(600)

(600)

Netfixedassets

6,500

7,050

550

(550)

CapitalExpenditures

$(1,150)

Notepayable

5,500

6,050

550

550

Short-termBorrowing

$550

Long-termdebt

2,000

1,602

(398)

(398)

Long-termDebtRepaid

$(398)

Netincome

(1,080)

(1,080)

Retainedearnings

500

1,148

648

648

Dividends

$(432)

______

_______

$0

$100

6.{L}a.Exhibit3P-3doesnotprovidethe(changesinthe)individualcomponentsthatmakeupthechangesinworkingcapital.Assuch,tocreatethedirectmethodcashflowstatement,wemustobtaintheinformationdirectlyfromthebalancesheet.Thisproceduredoesnotnecessarilyyieldthesamecashflowcomponentsusingthedirectmethodasthoseprovidedbythecompanyinitsindirectmethodcalculations.Differencesmayarisewhen

1.thereareacquisitions/divestments

2.thereareforeignexchangeadjustments

3.thefirmaggregatesorclassifiesinvestingaccrualstogetherwithoperatingones.

Inthiscase,thedifferencesareminimalasindicatedbelow.(ThecalculationsrequiredforthedirectmethodcashflowstatementarepresentedinExhibit3S-1alongwiththeassumptionsusedtogeneratethestatement)

DirectMethodCashFlowStat

升级会员

升级会员