第7章ARCH模型和GARCH模型.docx

《第7章ARCH模型和GARCH模型.docx》由会员分享,可在线阅读,更多相关《第7章ARCH模型和GARCH模型.docx(28页珍藏版)》请在冰豆网上搜索。

第7章ARCH模型和GARCH模型

第7章、ARCH模型和GARCH模型

研究内容:

研究随时间而变化的风险。

(回忆:

Markowitz均值-方差投资组合选择模型怎样度量资产的风险)

本章模型与以前所学的异方差的不同之处:

随机扰动项的无条件方差虽然是常数,但是条件方差是按规律变动的量。

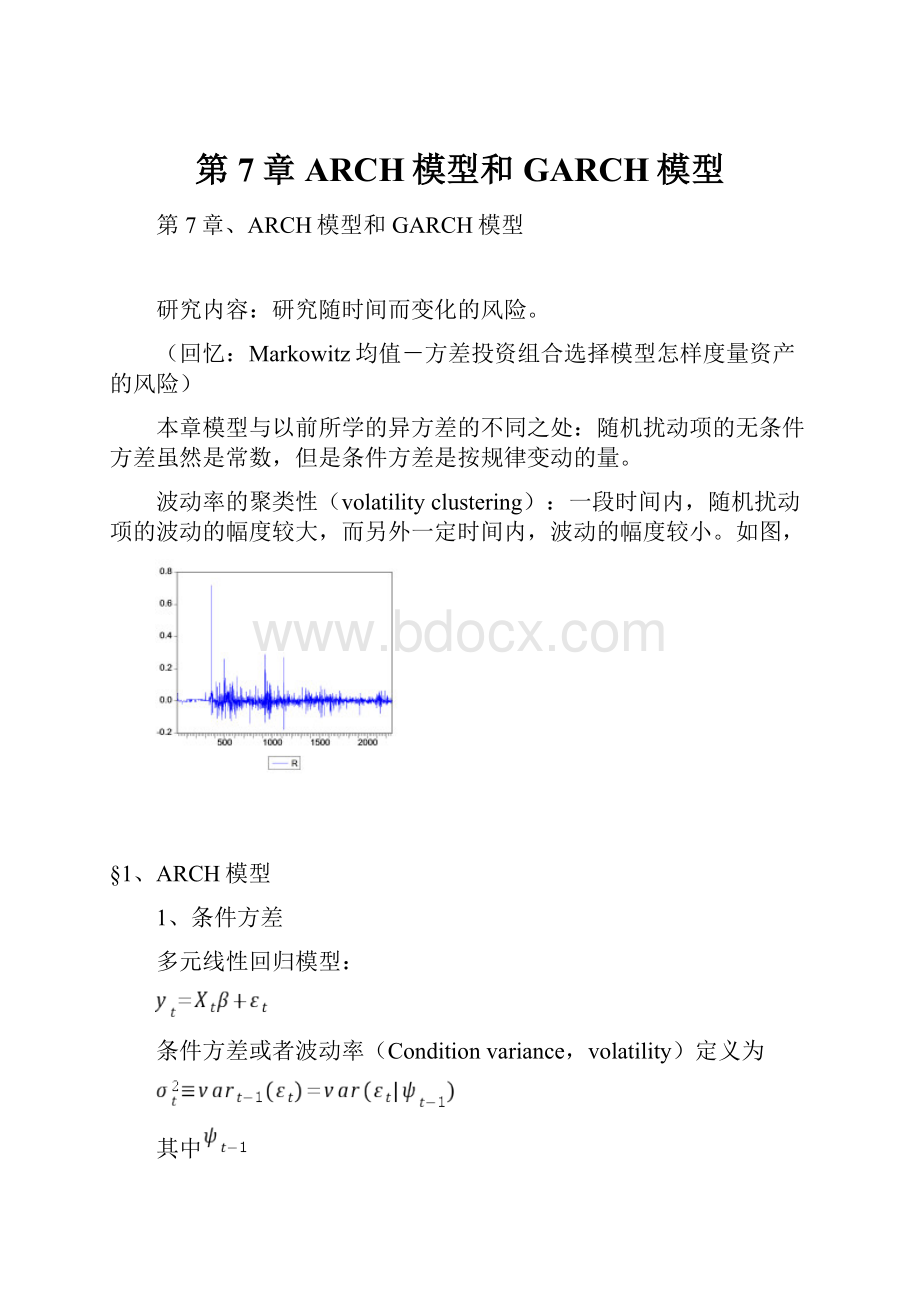

波动率的聚类性(volatilityclustering):

一段时间内,随机扰动项的波动的幅度较大,而另外一定时间内,波动的幅度较小。

如图,

§1、ARCH模型

1、条件方差

多元线性回归模型:

条件方差或者波动率(Conditionvariance,volatility)定义为

其中

是信息集。

2、ARCH模型的定义

Engle(1982)提出ARCH模型(autoregressiveconditionalheteroskedasticity,自回归条件异方差)。

ARCH(q)模型:

(1)

的无条件方差是常数,但是其条件分布为

(2)

其中

是信息集。

方程

(1)是均值方程(meanequation)

✓

:

条件方差,含义是基于过去信息的一期预测方差

方程

(2)是条件方差方程(conditionalvarianceequation),由二项组成

✓常数

✓ARCH项

:

滞后的残差平方

习题:

方程

(2)给出了

的条件方差,请计算

的无条件方差。

证明:

利用方差分解公式:

Var(X)=VarY[E(X|Y)]+EY[Var(X|Y)]

由于

,所以条件均值为0,条件方差为

。

那么,

推出

,说明

3、ARCH模型的平稳性条件

在ARCH

(1)模型中,观察参数

的含义:

当

时,

当

时,退化为传统情形,

ARCH模型的平稳性条件:

(这样才得到有限的方差)

4、ARCH效应检验

ARCHLMTest:

拉格朗日乘数检验

建立辅助回归方程

此处

是回归残差。

原假设:

H0:

序列不存在ARCH效应

即

H0:

可以证明:

若H0为真,则

此处,m为辅助回归方程的样本个数。

R2为辅助回归方程的确定系数。

Eviews操作:

①先实施多元线性回归

②view/residual/Tests/ARCHLMTest

§2、GARCH模型的实证分析

从收盘价,得到收益率数据序列。

seriesr=log(p)-log(p(-1))

点击序列p,然后view/linegraph

1、检验是否有ARCH现象。

首先回归。

取2000到2254的样本。

输入lsrc,得到

DependentVariable:

R

Method:

LeastSquares

Date:

10/21/04Time:

21:

26

Sample:

20002254

Includedobservations:

255

Variable

Coefficient

Std.Error

t-Statistic

Prob.

C

0.000432

0.001087

0.397130

0.6916

R-squared

0.000000

Meandependentvar

0.000432

AdjustedR-squared

0.000000

S.D.dependentvar

0.017364

S.E.ofregression

0.017364

Akaikeinfocriterion

-5.264978

Sumsquaredresid

0.076579

Schwarzcriterion

-5.251091

Loglikelihood

672.2847

Durbin-Watsonstat

2.049819

问题:

这样进行回归的含义是什么?

其次,view/residualtests/ARCHLMtest,得到

ARCHTest:

F-statistic

5.220573

Probability

0.000001

Obs*R-squared

44.68954

Probability

0.000002

TestEquation:

DependentVariable:

RESID^2

Method:

LeastSquares

Date:

10/21/04Time:

21:

27

Sample(adjusted):

20102254

Includedobservations:

245afteradjustingendpoints

Variable

Coefficient

Std.Error

t-Statistic

Prob.

C

0.000110

5.34E-05

2.060138

0.0405

RESID^2(-1)

0.141549

0.065237

2.169776

0.0310

RESID^2(-2)

0.055013

0.065823

0.835766

0.4041

RESID^2(-3)

0.337788

0.065568

5.151697

0.0000

RESID^2(-4)

0.026143

0.069180

0.377893

0.7059

RESID^2(-5)

-0.041104

0.069052

-0.595260

0.5522

RESID^2(-6)

-0.069388

0.069053

-1.004854

0.3160

RESID^2(-7)

0.005617

0.069178

0.081193

0.9354

RESID^2(-8)

0.102238

0.065545

1.559806

0.1202

RESID^2(-9)

0.011224

0.065785

0.170619

0.8647

RESID^2(-10)

0.064415

0.065157

0.988613

0.3239

R-squared

0.182406

Meandependentvar

0.000305

AdjustedR-squared

0.147466

S.D.dependentvar

0.000679

S.E.ofregression

0.000627

Akaikeinfocriterion

-11.86836

Sumsquaredresid

9.19E-05

Schwarzcriterion

-11.71116

Loglikelihood

1464.875

F-statistic

5.220573

Durbin-Watsonstat

2.004802

Prob(F-statistic)

0.000001

得到什么结论?

2、模型定阶:

如何确定q

实施ARCHLMtest时,取较大的q,观察滞后残差平方的t统计量的p-value即可。

此处选取q=3。

因此,可以对残差建立ARCH(3)模型。

3、ARCH模型的参数估计

参数估计采用最大似然估计。

具体方法在GARCH一节中讲解。

如何实施ARCH过程:

由于存在ARCH效应,所以点击estimate,在method中选取ARCH

得到如下结果

DependentVariable:

R

Method:

ML-ARCH

Date:

10/21/04Time:

21:

48

Sample:

20002254

Includedobservations:

255

Convergenceachievedafter13iterations

Coefficient

Std.Error

z-Statistic

Prob.

C

-0.000640

0.000750

-0.852888

0.3937

VarianceEquation

C

9.24E-05

1.66E-05

5.569337

0.0000

ARCH

(1)

0.244793

0.082640

2.962142

0.0031

ARCH

(2)

0.081425

0.077428

1.051624

0.2930

ARCH(3)

0.457883

0.109698

4.174043

0.0000

R-squared

-0.003823

Meandependentvar

0.000432

AdjustedR-squared

-0.019884

S.D.dependentvar

0.017364

S.E.ofregression

0.017535

Akaikeinfocriterion

-5.495982

Sumsquaredresid

0.076872

Schwarzcriterion

-5.426545

Loglikelihood

705.7377

Durbin-Watsonstat

2.042013

为了比较,观察将q放大对系数估计的影响

DependentVariable:

R

Method:

ML-ARCH

Date:

10/21/04Time:

21:

54

Sample:

20002254

Includedobservations:

255

Convergenceachievedafter16iterations

Coefficient

Std.Error

z-Statistic

Prob.

C

-0.000601

0.000751

-0.799909

0.4238

VarianceEquation

C

9.38E-05

1.60E-05

5.880741

0.0000

ARCH

(1)

0.262009

0.090256

2.902959

0.0037

ARCH

(2)

0.041930

0.070518

0.594596

0.5521

ARCH(3)

0.452187

0.108488

4.168076

0.0000

ARCH(4)

-0.021920

0.050982

-0.429956

0.6672

ARCH(5)

0.037620

0.044394

0.847408

0.3968

R-squared

-0.003550

Meandependentvar

0.000432

AdjustedR-squared

-0.027830

S.D.dependentvar

0.017364

S.E.ofregression

0.017603

Akaikeinfocriterion

-5.483292

Sumsquaredresid

0.076851

Schwarzcriterion

-5.386081

Loglikelihood

706.1198

Durbin-Watsonstat

2.042568

观察:

说明q选取为3确实比较恰当。

4、ARCH模型是对的吗?

如果ARCH模型选取正确,即回归残差的条件方差是按规律变化的,那么标准化残差就会服从标准正态分布,即不会有ARCH效应了。

为什么?

请思考。

对q为3的ARCH模型做LMtest,发现没有了ARCH效应。

注意,虽然是同一个检验名称,但是ARCH过程后是对标准化残差进行检验。

注意观察被解释变量或者依赖变量是什么?

ARCHTest:

F-statistic

0.238360

Probability

0.992099

Obs*R-squared

2.470480

Probability

0.991299

TestEquation:

DependentVariable:

STD_RESID^2

Method:

LeastSquares

Date:

10/21/04Time:

21:

56

Sample(adjusted):

20102254

Includedobservations:

245afteradjustingendpoints

Variable

Coefficient

Std.Error

t-Statistic

Prob.

C

1.102371

0.264990

4.160043

0.0000

STD_RESID^2(-1)

-0.038545

0.065360

-0.589741

0.5559

STD_RESID^2(-2)

-0.003804

0.065308

-0.058252

0.9536

STD_RESID^2(-3)

-0.057313

0.065303

-0.877649

0.3810

STD_RESID^2(-4)

-0.010325

0.065277

-0.158169

0.8745

STD_RESID^2(-5)

0.003537

0.065280

0.054185

0.9568

STD_RESID^2(-6)

-0.007420

0.065274

-0.113670

0.9096

STD_RESID^2(-7)

0.063317

0.065264

0.970165

0.3330

STD_RESID^2(-8)

-0.012167

0.065293

-0.186340

0.8523

STD_RESID^2(-9)

-0.010653

0.065278

-0.163194

0.8705

STD_RESID^2(-10)

-0.020211

0.065228

-0.309845

0.7570

R-squared

0.010084

Meandependentvar

1.007544

AdjustedR-squared

-0.032221

S.D.dependentvar

2.112747

S.E.ofregression

2.146514

Akaikeinfocriterion

4.409426

Sumsquaredresid

1078.160

Schwarzcriterion

4.566625

Loglikelihood

-529.1546

F-statistic

0.238360

Durbin-Watsonstat

2.000071

Prob(F-statistic)

0.992099

方程整体是不显著的。

还可以观察标准化残差

ARCH建模以后,procs/makeresidualseries/可以产生残差

和标准化残差

,以分别下是残差和标准化残差。

可以看出没有了集群现象。

还可以观察波动率(条件方差)的图形。

对比r和残差的图形,发现条件方差的起伏与波动率的大小一致。

ARCH建模以后,procs/makegarchvarianceseries/得到

结论:

ARCH模型确实很好描述了股票市场收益率的波动性。

可以观察系数之和小于1,满足平稳性条件。

§3、GARCH模型

当q较大时,采用Bollerslov(1986)提出的GARCH模型(GeneralizedARCH)

1、模型定义

条件方差方程

✓均值

✓

✓

:

过去的条件方差(也即预测方差,forecastvariance)

注意:

均值方程中若没有解释变量(即只有常数,如RC),则R2没有直观定义了,因此可为负)

2、GARCH(p,q)模型的稳定性条件

计算扰动项的无条件方差:

GARCH是协方差稳定的,因此是经典回归。

3、GARCH模型的参数估计

采用极大似然估计GARCH模型的参数。

下面以GARCH(1,1)为例。

由GARCH(1,1)模型

可以得到yt的分布为

由正态分布的定义公式,得到yt的pdf为

第t个观察样本的对数似然函数值为

其中

注意yi和yj之间不相关,因而是独立的。

似然函数为

取对数就得到了所有样本的对数似然函数。

其中条件方差项以非线性方式进入似然函数,所以不得不使用迭代算法求解。

4、模型的选择

两条原则:

1)若ARCH(q)中q太大,比如q大于7时,则选择GARCH(p,q)

2)使用AIC和SC准则,选择最优的GARCH模型

3)对于金融时间序列,一般选择GARCH(1,1)就够了。

回顾AIC和SC定义:

1)AIC准则(Akaikeinformationcriterion)

AIC越小越好,结合如下两者:

K(自变量个数)减少,模型简洁

LnL增加,模型精确

2)SC准则(Schwazcriterion)

习题1:

通货膨胀率有ARCH效应吗?

GreeneP572

点击数据文件usinf_greene_p572。

进行回归

lsinflationcinflation(-1)

DependentVariable:

INFLATION

Method:

LeastSquares

Date:

11/19/04Time:

10:

37

Sample(adjusted):

19411985

Includedobservations:

45afteradjustingendpoints

Variable

Coefficient

Std.Error

t-Statistic

Prob.

C

2.432859

0.816345

2.980184

0.0047

INFLATION(-1)

0.493213

0.131157

3.760466

0.0005

R-squared

0.247477

Meandependentvar

4.740000

AdjustedR-squared

0.229976

S.D.dependentvar

4.116784

S.E.ofregression

3.612519

Akaikeinfocriterion

5.450114

Sumsquaredresid

561.1625

Schwarzcriterion

5.530410

Loglikelihood

-120.6276

F-statistic

14.14110

Durbin-Watsonstat

1.612442

Prob(F-statistic)

0.000507

检验ARCH效应

ARCHTest:

F-statistic

0.215950

Probability

0.953308

Obs*R-squared

1.231192

Probability

0.941850

TestEquation:

DependentVariable:

RESID^2

Method:

LeastSquares

Date:

11/19/04Time:

10:

46

Sample(adjusted):

19461985

Includedobservations:

40afteradjustingendpoints

Variable

Coefficient

Std.Error

t-Statistic

Prob.

C

9.270522

7.425567

1.248460

0.2204

RESID^2(-1)

-0.031162

0.170116

-0.183184

0.8557

RESID^2(-2)

-0.006886

0.170151

-0.040469

0.9680

RESID^2(-3)

0.116261

0.169505

0.685888

0.4974

RESID^2(-4)

0.018545

0.170620

0.108694

0.9141

RESID^2(-5)

0.127906

0.168643

0.758439

0.4534

R-squared

0.030780

Meandependentvar

12.28323

AdjustedR-squared

-0.111753

S.D.dependentvar

34.15088

S.E.ofregression

36.00858

Akaikeinfocriterion

10.14287

Sumsquaredresid

44085.00

Schwarzcriterion

10.39620

Loglikelihood

-196.8574

F-statistic

0.215950

Durbin-Watsonstat

1.034796

Prob(F-statistic)

0.953308

习题2:

通货膨胀率有ARCH效应吗?

Lin的数据集

点击usinf文件

seriesdp=100*D(log(p))

lsdpcdp(-1)dp(-2)dp(-3)

DependentVariable:

DP

Method:

LeastSquares

Date:

11/19/04Time:

10:

10

Sample(adjusted):

1951:

11983:

4

Includedobservations:

132afteradjustingendpoints

Variable

Coefficient

Std.Error

t-Statistic

Prob.

C

0.109907

0.063405

1.733410

0.0854

DP(-1)

0.393583

0.084432

4.661536

0.0000

DP(-2)

0.203093

0.089452

2.270405

0.0249

DP(-3)

0.302073

0.084185

3.588214

0.0005

R-squared

0.696825

Meandependentvar

1.021373

AdjustedR-squared

0.689719

S.D.dependentvar

0.711412

S.E.ofregression

0.396277

Akaikeinfocriterion

1.016428

Sumsquaredresid

20.10054

Schwarzcriterion

1.103785

Loglikelihood

-63.08423

F-statistic

98.06599

D

升级会员

升级会员