23 Public finance for public goods JULYWord文档下载推荐.docx

《23 Public finance for public goods JULYWord文档下载推荐.docx》由会员分享,可在线阅读,更多相关《23 Public finance for public goods JULYWord文档下载推荐.docx(29页珍藏版)》请在冰豆网上搜索。

Taxesandpublicfinance

Taxationwhenincomeisspent

Taxeswithoutanexcessburden

Administrativeandemotionalcostsoftaxation

Deferredtaxation:

Governmentborrowing

Whopaysatax?

Economy-wideeffectsoftaxes

Reponsestoagovernmentbudgetsurplus

Summary

WesawintheprevioussectionthatfinancingandsupplyofpublicgoodsisideallydeterminedbytheLindahlconsensussolution,butthatgovernmentslacktheinformationaboutpersonalbenefitsrequiredforimplementingtheLindahlsolution.TheClarketax,cost-benefitcalculations,andlocationalchoicearemeansofhopingtosolvetheinformationproblem.Weshallnowsetasidetheinformationproblem.Thequestionthatweaddressinthissectionishowtofinancepublicspendingonpublicgoods.

Wewouldhavelikedtohaveunambiguouslysolvedtheinformationproblemabouthowmuchtospendonapublicgoodbeforebeginningtoconsiderhowtofinancepublicspendingonapublicgood.Wedonothoweverhaveanunambiguoussolutiontotheinformationproblem.Weshallthereforehavetosupposethatagovernmentsomehowknowsthebenefitstothepopulationfromapublicgoodandalsoknowsthecostsofsupplyingthepublicgood.Perhapsinformationnotprovidedbymarketvalueswasobtainedthroughaccuratecost-benefitanalysis,orperhapsthegovernmentjurisdictionconsistsofpeoplewhohaverevealedtheirsimilarknownpreferencesthroughlocationalchoice.Weshallthereforenowregard∑MBforthepopulationandtheMCofthepublicgoodasknowntothegovernment,whereMCisdeterminedbythepricesoftheinputsusedtoprovidethepublicgood.

Weshallbeconcernedwithtaxeswhenpublicgoodsarenotcongestibleorcongested.Whenpublicgoodsbecomecongested,thepurposeoftaxationcanbenottofinanceapublicgood,buttodiscourageexcessiveuseandsoreducecongestion.Forpurepublicgoodsorpublicgoodsthatarenotcongested,thereasonfortaxationistoprovidemeansoffinancingpublicspending.

Publicgoodscanbefinancedbyuserpricesratherthantaxation.Userpricesrequiretheabilitytoexcludefrombenefitpeoplewhodonotpay,asforexampleexcludingusersfromatollroadorbridgeiftheydonotpay.Peoplecouldalso,forexample,payauserpriceeverytimetheycalluponthepoliceforassistance.Theuserchargescouldfinancethepolicebudget,soavoidingtheneedfortaxationandpublicfinance.Ifuserpriceswereimposedforcallingforpoliceassistance,victimswouldbepayingforpoliceservicesandpeoplewithinsufficientmoneywouldbedeniedtheprotectionoftheruleoflaw,whichappearssociallyundesirableandunethical.Sinceuserchargesforpoliceassistancewoulddiscouragepeoplefromreportingcrimes,criminalswouldalsohavegreateropportunitiestorepeattheircrimes.Thepolicealsoprovideapublicgoodthroughdeterrenceofcrime,anditisnotpossibletodirectlychargeforthebenefitsofdeterrence.Userchargesarethereforenotleviedtofinancethecostsofpoliceprotection.Whereexclusionfrombenefitofpeoplewhodonotpayispossible,voluntaryprivatepaymentishoweverinprincipleanalternativetocompulsorytaxationofpublicfinance.Weshallreturntoconsideruserpricingasanalternativetotaxationandpublicfinanceforpublicgoods.

Here,weshallnowconsidertaxationandpublicfinanceasthemeansofpayingforpublicgoods.Afterthepublicgoodshavebeenfinancedthroughtaxation,thebenefitsfrompubliclyfinancedpublicgoodsarethenavailablewithoutfurtherpaymenttoeverybody.Thefreeaccesstothepubliclyfinancedpublicgoodsisefficient,sinceonepersonbenefitingdoesnotreducethebenefittoanyotherperson.

ThepersonalLindahlpricesprovideefficientfinancingforpublicgoodsbuttheLindahlsolutioncannotbeimplemented.IfhowevertheefficientLindahlpricescouldbepersonallychargedtofinancepublicgoods,thepaymentsmakeforpublicgoodswouldbeinthemarketforapublicgood.Thatis,inthemarketforthepublicgood,peoplewouldbevoluntarilypayingtheirshareofthecostofsupply.

ThevoluntaryLindahlpaymentswithinamarketforpublicgoodscontrastwithfinancingofpublicgoodsthroughcompulsorytaxesthatareleviedonbuyersandsellersinothermarketsandnotinthemarketforthepublicgooditself.Thetaxesinothermarketscanbetaxesonincomesearnedinthelabormarketorsalestaxesonprivatespendingonprivategoods.Thesetaxesinothermarketsareanintrusionintotheseothermarkets.Theintrusionhasacost,throughapersonalefficiencylossfortaxpayers.

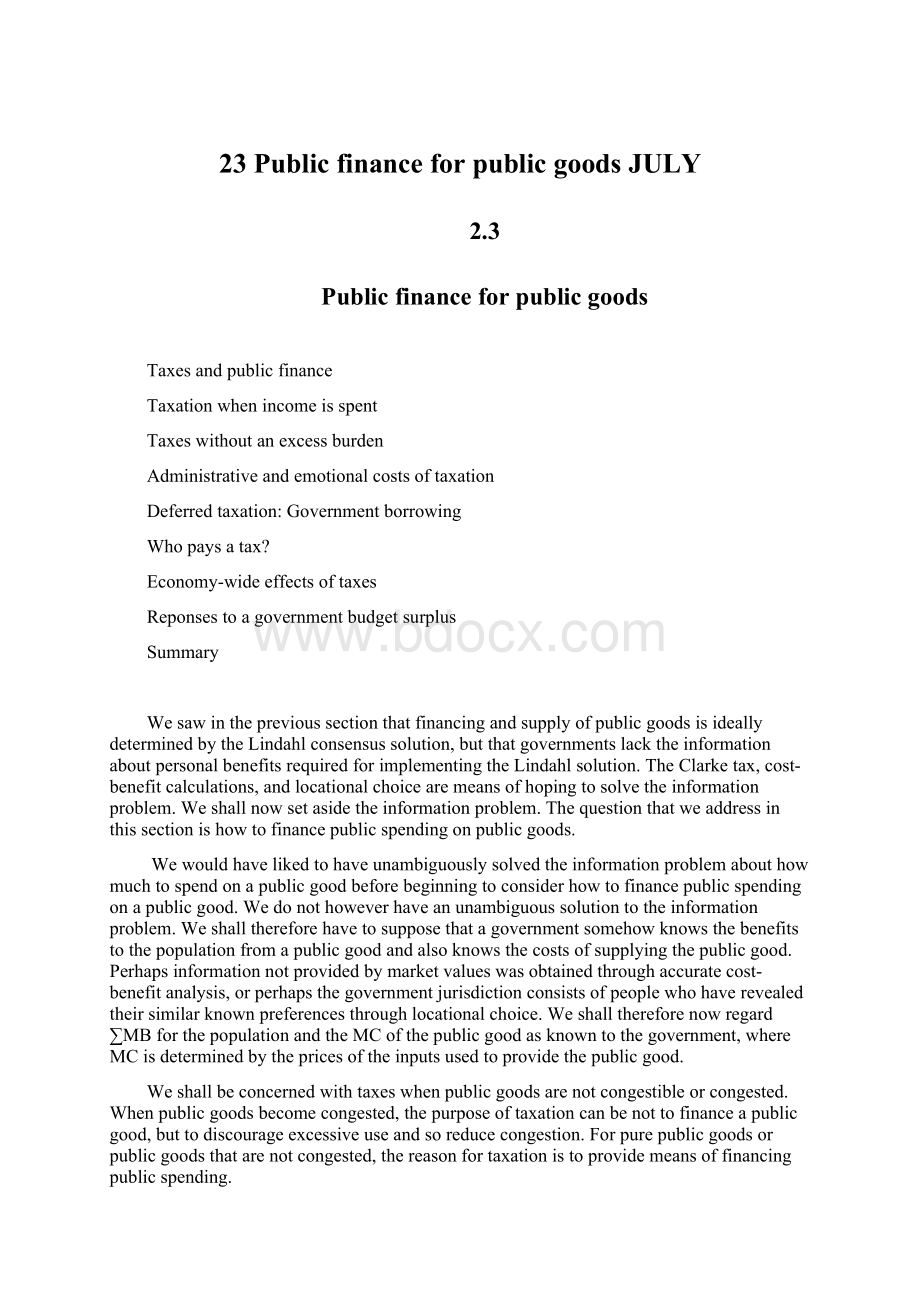

Toseehowthepersonalefficiencylossarises,wecanconsiderataxonincome.Figure2.22showsanindividual’ssupplyoflaborfunctionSL(foraweek,ormonth,oryear).Thesupplyoflaborfunctionshowsthesubstitutionbetweenhoursworkedandfreetimewhenthenet-of-taxwagethattheindividualreceiveschanges.Asthenet-of-taxwageincreases,theindividualsubstitutesincome-earningactivityforfreetimeandlaborsupply(andeffort)increases.

Attheindividual’smarket-determinedwagewwithnotaxation,theindividualchoosestoworkL2hours.Anincometaxataconstanttpercentreducesthenet-of-taxwageperhourtow(1-t),andtheindividualrespondsbydecreasinghoursworkedtoL1.

Pre–taxwagegiveninalabormarket

Figure2.22:

Theexcessburdenofanincometax.

ThetaxoftpercentisleviedonthetaxbaseofL1hoursworked.Afterthetax,theemployercontinuestopaythecompetitivelydeterminedmarketwagew.Theindividual’spre-taxincomeinfigure2.22isABJOandnet-of-taxincomeisCDJO.ThedifferencebetweengrossincomeandnetincomeisthemoneyABCDpaidastaxestothegovernment.

Weseeinfigure2.22thatthetaxhascreatedagapbetweenthecostoflabortotheemployerwandthewagereceivedbytheemployeew(1-t).Thetaxhasalsoresultedinachangeinmarketbehavior,indicatedinthedeclineinlaborsupplyfromL2toL1.Thechangeinmarketbehaviorhasoccurredthroughasubstitutionresponse,withtheindividualsubstitutingfreetimeforproductivetime.Thesubstitutionresponseisthesourceofapersonalefficiencyloss.

Thepresenceofthepersonalefficiencylossduetothetaxisrevealedwhenweasktheindividualinfigure2.22oneoftwoquestions:

(1)Howmuchareyoupreparedtopaythegovernment,inreturnforthegovernmentnotlevyingtheincometaxonyou?

(2)Howmuchdoesthegovernmenthavetogiveyoutocompensateyouforthetaxthathasbeenleviedonyou?

Thefirstquestionpresumesthatthetaxisnotlevied,andaskshowmuchtheindividualiswillingtopaytokeepthetaxatbay.Thesecondquestionpresumesthatthetaxisinplace,andaskshowmuchtheindividualhastobepaidascompensationforthetaxhavingbeenlevied.

Letussupposethat,inansweringthequestions,theindividualinfigure2.22feelsnobenefitfromthetaxespaidtothegovernment.Theindividualthenwantsthemoneypaidintaxesreturned.Still,theanswertothequestionhowmuchtheindividualispreparedtopaytoavoidpayingthetaxismorethanthemoneypaidintaxes.Theanswertothequestionhowmuchtheindividualhastobecompensatedforhavinghadtopaythetaxisalsomorethanthevalueofthemoneypaidintaxes.Inbothcases,thereisanexcessburdenoftaxationbeyondthevalueofthemoneypaidintaxes.

TheexcessburdenoftaxationistheareaDBEinfigure2.22.Theindividualinfigure2.22ispreparedtopayanamountofmoneyDBEthatismorethanthevalueofthetaxtoavoidpayingthetax,andhastobecompensatedbytheamountofmoneyDBEmorethanthevalueofthetaxforhavingpaidthetax.

WhyisDBEapersonallossfromtaxation?

Whenlaborissupplied,apersonalcostisincurredthroughfreetimethatwouldhavebeenavailable.ThepersonalcostisexpressedthroughthelaborsupplyfunctionSL,whichisapersonalMCfunctionforlaborsupplied.TheareaunderthefunctionSLiscorrespondinglythepersonaltotalcostofsupplyinglabor.Wecannowproceedthroughthefollowingsteps:

(1)Beforethetaxisimposed,theindividual’sbenefitfrommarketparticipationinfigure2.22isOAE,whichisthebenefitorincomeAEHOfromsupplyingL2hoursoflaborminusthecostOEHofsupplyingthesehoursoflabor.

(2)Afterthetaxisimposed,theindividual’sbenefitfrommarketparticipationisOCD,whichisthedifferencebetweenpost-taxincomeABJOandthepersonalcostODJintermsoffreetimeforgoneofsupplyingL1hoursoflabor.

(3)Theeffectofthetaxhasthereforebeentoreducethegainfrommarketparticipationby(AEO-CDO)=AEDC.

(4)AEDChastwocomponents.OnecomponentisthetaxrevenueABCDpaidtothegovernment.ThesecondcomponentisDBE,whichistheadditionalpersonallossfromthetaxinexcessofthetaxrevenuepaidtothegovernment.

Theefficiencylossoftaxation

Wehavebeenviewingtheindividualbeingtaxedasnotfeelingbenefitfromthetaxpaidtothegovernment.Taxeshoweverfinancepublicspendingonpublicgoods,andthepublicgoodscanbeasourceofbenefitforthetaxpayer.ThereishowevernoprospectforgainassociatedwiththeexcessburdenDBEinfigure2.22.Theexcessburdenispurelyandsimplyanefficiencyloss,orawaste.

TheefficiencylossDBEisbornepersonallybythetaxpayerinfigure2.22.Thepersonalefficiencylossisnotdirectlyobservedasanysumofmoney.Itissomethingthatapersonhadbeforethetax,butthatdisappearedafterthetax.Nosumofmoneyequaltotheexcessburdenoftaxationchangeshands.Theexcessburdenoftaxationisinvisible.

Whenthesupply-of-laborfunc

升级会员

升级会员