US GAAP vs PRC GAAPQuestionnair.docx

《US GAAP vs PRC GAAPQuestionnair.docx》由会员分享,可在线阅读,更多相关《US GAAP vs PRC GAAPQuestionnair.docx(29页珍藏版)》请在冰豆网上搜索。

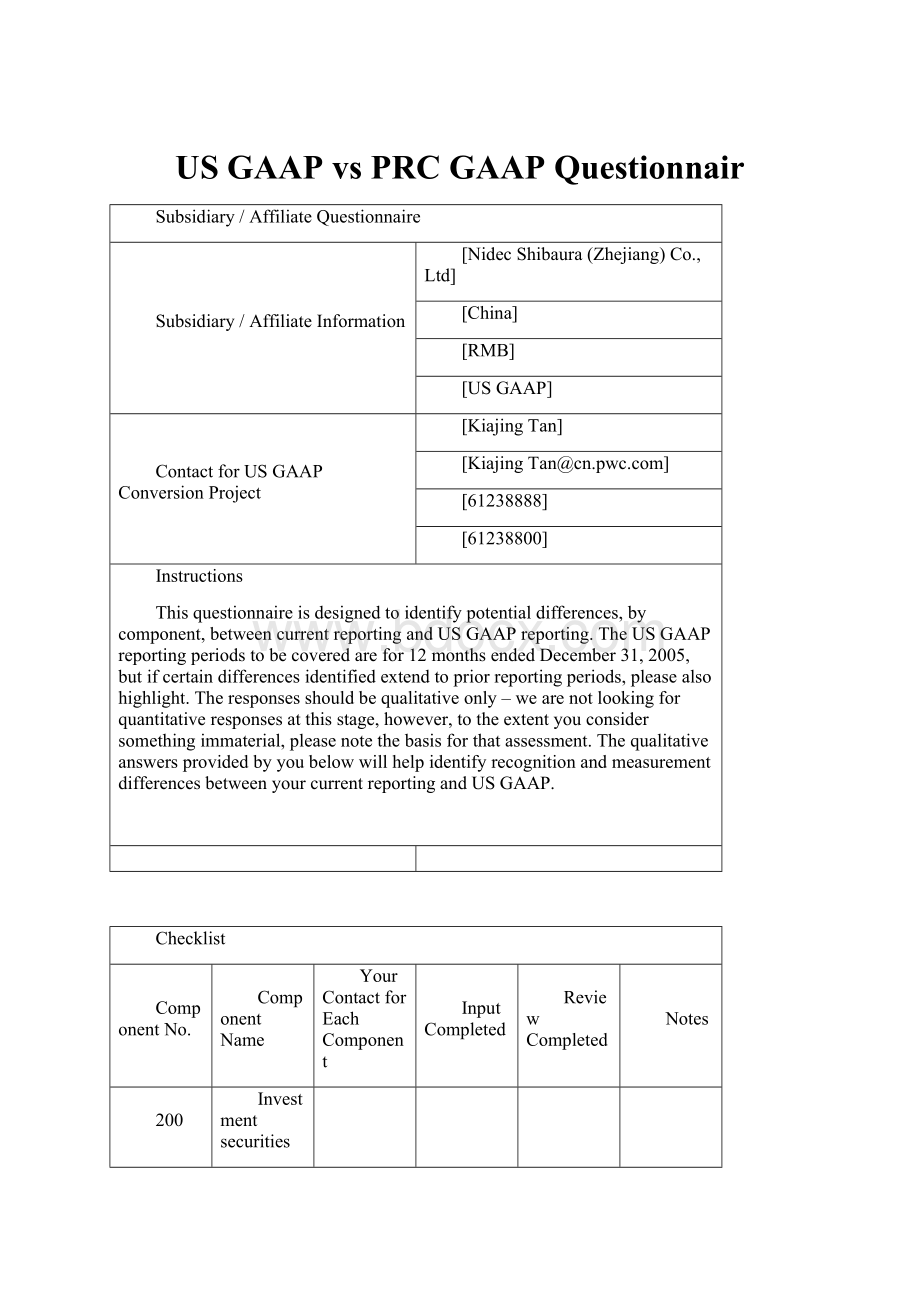

USGAAPvsPRCGAAPQuestionnair

Subsidiary/AffiliateQuestionnaire

Subsidiary/AffiliateInformation

[NidecShibaura(Zhejiang)Co.,Ltd]

[China]

[RMB]

[USGAAP]

ContactforUSGAAPConversionProject

[KiajingTan]

[KiajingTan@]

[61238888]

[61238800]

Instructions

Thisquestionnaireisdesignedtoidentifypotentialdifferences,bycomponent,betweencurrentreportingandUSGAAPreporting.TheUSGAAPreportingperiodstobecoveredarefor12monthsendedDecember31,2005,butifcertaindifferencesidentifiedextendtopriorreportingperiods,pleasealsohighlight.Theresponsesshouldbequalitativeonly–wearenotlookingforquantitativeresponsesatthisstage,however,totheextentyouconsidersomethingimmaterial,pleasenotethebasisforthatassessment.ThequalitativeanswersprovidedbyyoubelowwillhelpidentifyrecognitionandmeasurementdifferencesbetweenyourcurrentreportingandUSGAAP.

Checklist

ComponentNo.

ComponentName

YourContactforEachComponent

InputCompleted

ReviewCompleted

Notes

200

Investmentsecurities

205

Derivatives,EmbeddedDerivatives

210

Revenue&Notesandaccountsreceivable

215

Inventory

220

Otherassets

225

PremisesandEquipment

230

Goodwill&Intangibleassets

235

Capitalizedsoftwarecosts&R&D

240

ExitActivities

245

Leases(lessor)

250

Leases(lessee)

300

Notesandaccountspayable

310

WarrantyandOtherliabilities

315

EmployeeBenefits

320

TaxAccounting

325

Contingencies

330

Environmentalliabilities

400

Equity

100

Financialreporting&other

105

Consolidation

110

FIN46

120

ForeignExchange

Component:

-InvestmentSecuritiesN/A

USGAAPBackground

Investmentsecuritiesusuallyincludenotonlysecuritiessuchasequity,debtsecurities,mutualfundsbutalsopartnershiporotherinvestments,suchasventurecapitalpartnerships,etc..Dependingontheclassificationandwhethertheyhavereadilydeterminablefairvalues,theyaregenerallyaccountedforatfairvalue,amortizedcostoracquisitioncost.

Questions

Responses

1.Whattypesofinvestmentsecuritiesdoestheentityhave?

Arethereanyforeigncurrencydenominatedinvestments?

Arethereanyintercompanyinvestmentsenteredintowiththeparent,othersubsidiariesoraffiliates?

Doestheentitypurchaseorsellanysharesoftheparent,othersubsidiariesoraffiliates?

N/A

2.UnderUSGAAP,investmentsinequitysecuritieswithreadilydeterminablefairvaluesandallinvestmentsindebtsecuritiesareclassifiedeitheras

(1)trading,

(2)available-for-saleor(3)held-to-maturitydependingonmanagement’sdetermination.Howdoestheentityclassifysuchinvestments?

N/A

3.UnderUSGAAP,equityanddebtsecuritiesclassifiedastradingoravailable-for-salearerecordedatperiodendfairvaluesgenerallyobtainedfromanactiveexchange.Fairvaluechangesfortradingsecuritiesarerecordedinearningsandfairvaluechangesforavailable-for-salesecuritiesarerecordedinothercomprehensiveincome(“OCI”)inequity.Doestheentityuseperiodendfairvaluestovaluesecurities?

Whatarethesourcesforthefairvalues?

Wherearethefairvaluechangesrecorded-netincomeorothercomprehensiveincome?

N/A

4.Doestheentityhaveinvestmentsinunlistedequityanddebtsecurities?

Howaretheyrecorded?

Aretheysubjecttofairvalueassessmentsandreviewedperiodicallyforimpairment?

N/A

5.UnderUSGAAP,unrealizedlossesorimpairmentofinvestmentsecuritiesthatisconsideredother-than-temporaryarerecognizedasrealizedlosses.Thecostbasisofinvestmentsecuritiesarewrittendowntofairvalueandanysubsequentupwardadjustmentstocostarenotallowed.Howdoestheentityassessforimpairmentandhowaretheyrecognized?

N/A

6.Onwhatbasisdoestheentityrecordsalesofsecurities?

Forinstance,first-infirst-out(“FIFO”)orweightedaveragecostbasis?

N/A

7.UnderUSGAAP,investmentsinvotingcommonstocksexceeding20%aregenerallyaccountedforusingtheequitymethod.Doestheentityhavesuchinvestmentsandhowaretheyaccountedfor?

N/A

8.UnderUSGAAP,majorityownedorover50%interestsinmutualfundsorventurecapitalpartnershipsaregenerallyconsolidated.Arethereanysuchmajorityownedinvestmentsandhowaretheyaccountedfor?

N/A

Component:

-Derivatives&EmbeddedDerivativesN/A

USGAAPBackground

UnderUSGAAP,allderivativesarefairvaluedonthebalancesheetwithchangesreflectedinearnings.Derivativestypicallyincludefutures,options,swaps,andforwards.

9.Whattypesofderivativesdoestheentityhave?

ArethosederivativesenteredintowithintheLeargrouporwithunrelatedparties?

N/A

10.UnderUSGAAP,allderivatives,includingthosethatareembeddedinothercontracts,arerecordedatfairvalueatyearendwithchangesreflectedinearnings.Arederivativesfairvaluedfortheentity?

Iftherewereanyderivativeswhicharenotrecordedatfairvalue,pleaseexplainthenatureofthederivatives.

11.Haveanyhedgeaccountingbeenappliedfortheentity?

Ifno,passthequestions[12]–[15],andgoto[16].

12.UnderUSGAAP,toqualifyforhedgeaccounting,extensivehedgedocumentationforhedgerelationshipsandperiodiceffectivenesstestingarerequired.Ifapplicable,whattypesofdocumentationortestingdoestheentityhave?

13.UnderUSGAAP,macrohedgesinwhichonederivativeinstrumentisusedtohedgemultipleitemsarenotpermitted.Ifapplicable,doestheentityhaveanymacrohedges?

14.Ifyourentityapplieshedgeaccounting,howmuchistheimpactonbalancesheetandincomestatements?

Pleaseestimatetheimpactinmillionyens.

15.UnderUSGAAP,anembeddedderivativeinstrumentmustbeseparatedfromthehostcontractandaccountedforseparatelyasaderivativeinstrumentatfairvalueifcertaincriteriahavebeenfulfilled.Ifapplicable,doestheentityidentifyandbifurcateanyembeddedderivatives?

Inaddition,doestheentityhaveanyembeddedderivativesinstruments?

Anexamplesofanembeddedderivativeinstrumentswouldbe:

∙Purchaseorsaleagreementsdenominatedinsomethingotherthantheentity’sfunctionalcurrencymaycontainembeddedforwardforeignexchangecontracts.

Component:

–RevenueandNotes&AccountsReceivable

USGAAPBackground

USGAAPcontainsveryspecificguidanceonrevenuerecognition.Broadlyspeaking,revenueisrecognizedwhenfourbasiccriteriaaremet

(1)persuasiveevidenceofanarrangementexists;

(2)deliveryhasoccurredorserviceshavebeenrendered;(3)thefeeisfixedordeterminable;and(4)collectibilityisreasonablyassured

Questions

Responses

16.Describeyourentity’sgeneralrevenuerecognitionpolicy

TheoverseasaleswasrecognizeduponB/Ldate

Thedomesticsaleswasrecognizedupontheclientacceptancedate

17.Doestheentityhaveapracticeofusingsignedcontractsforsalesorders?

Whatarethegeneraltermsofthesecontracts–withafocuson

(1)deliveryterms;

(2)termswhichspecifywhenrisksandrewardsofownershiptransfer(i.e.FOBShipping/FOBDestinationorother);(3)paymentterms;(4)refundclauses;(5)inspectionprovisions

Yes.

Overseasales:

FOBshipping

Domesticsales:

Basedonclientacceptancedate

Paymentterms:

Differentpaymenttermsweresetfordifferentclients.

Generallythepaymenttermsvariancefrom30days~90days.

Butnootherspecificinspectionprovision/refundclauses

18.Ifapplicable,intheabsenceofsignedcontracts,whattypesofsalesagreementsdoestheentityhave?

Nonenoted.

19.Doestheentityenterintoanyrevenuearrangementswhichcontainmultipledeliverableswithinthesamearrangement?

Ifso,howarethesemultipledeliverablesaccountedforwithinthearrangement?

N/A

20.Doestheentityenterintolongtermsupplyarrangements/longtermsalescontractswherethepaymenttermsmayvaryoverthelifeofthecontract(forexample,volumediscountsafterreachingcertainsalestargets)

N/A

Thesales/purchasecontractrenewedyearly.

21.Whatpoliciesareappliedbytheentitytoaccountfortheallowancefordoubtfulaccounts?

Thegeneralbaddebtprovisionwithspecificbaddebtprovisionwasprovidedforaccountsreceivablesandotherreceivables.

Thepolicyofgeneralprovisionisasfollows:

Bal.within1Yr0.5%

Bal.over1Yr100.0%

22.Doestheentityhavesignificantinterestbearingreceivablesornotesreceivable?

Ifso,howisinterestincomerecognized?

N/A

23.Doestheentityenterintoanysecuritizationtransactions(salesofaccountsreceivable)?

Factoringarrangements?

N/A

Component:

–Inventory

USGAAPBackground

Theprimarybasisofaccountingforinventoriesiscost,nothigherthanthenetamountrealizablefromthesubsequentsaleofinventories.Costistheacquisitionandproductioncostsoftheinventory.Abnormalcosts,suchasidlefacilitycosts,excessivespoilage,orrehandlingcostsareincludedincurrentperiodincomeratherthandeferredasaportionofinventorycosts.

Questions

Responses

24.Brieflydescribe

(1)majorclassesofinventory,

(2)costsincludedwithininventoryand(3)howeachofthoseclassesofinventoryisvalued.

1)Themajorclassesofinventoriesarerawmaterial/workinginprogress/finishedgoods/Goodsintransit

2)Themajorcostsincludedwithininventoryarerawmaterialcost/labourcostandgeneralproductioncost

3)Theclassofinventoriesisvaluedaccordingtotheactualcostallocatedfordifferentstatusoftheproducts.

25.Brieflydescribethemethodology(FIFO,LIFO,average)bywhichcos

升级会员

升级会员