删除变量UADF检验及模型函数估计doc.docx

《删除变量UADF检验及模型函数估计doc.docx》由会员分享,可在线阅读,更多相关《删除变量UADF检验及模型函数估计doc.docx(18页珍藏版)》请在冰豆网上搜索。

删除变量UADF检验及模型函数估计doc

删除变量|U=(M2/Mo),建立模型:

经检验:

所有序列(变量)二阶(差分)单整,故可以得出他们之间存在协整关系。

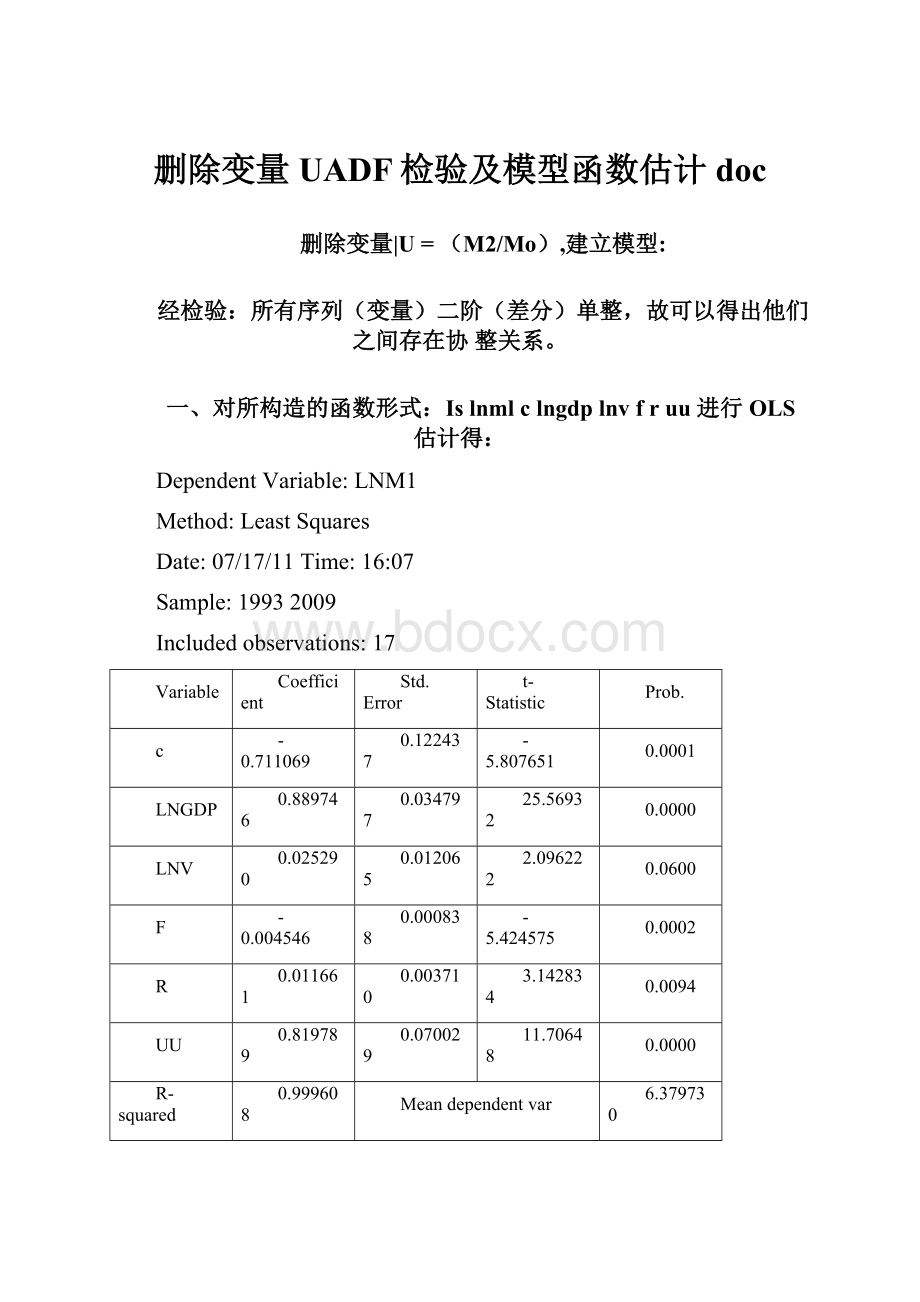

一、对所构造的函数形式:

Islnmlclngdplnvfruu进行OLS估计得:

DependentVariable:

LNM1

Method:

LeastSquares

Date:

07/17/11Time:

16:

07

Sample:

19932009

Includedobservations:

17

Variable

Coefficient

Std.Error

t-Statistic

Prob.

c

-0.711069

0.122437

-5.807651

0.0001

LNGDP

0.889746

0.034797

25.56932

0.0000

LNV

0.025290

0.012065

2.096222

0.0600

F

-0.004546

0.000838

-5.424575

0.0002

R

0.011661

0.003710

3.142834

0.0094

UU

0.819789

0.070029

11.70648

0.0000

R-squared

0.999608

Meandependentvar

6.379730

AdjustedR-squared

0.999429

S・D.dependentvar

0.800568

S・E・ofregression

0.019128

Akaikeinfocriterion

-4.804743

Sumsquaredresid

0.004025

Schwarzcriterion

-4.510668

Loglikelihood

46.84032

Hannan-Quinncriter.

-4.775512

F-statistic

5603.099

Durbin-Watsonstat

2.559494

Prob(F-statistic)

0.000000

因为变量LnV不显著,

将其删除

重新估计:

IsInm1'

cIngdpfi

DependentVariable:

LNM1

Method:

LeastSquares

Date:

07/17/11Time:

16:

10

Sample:

19932009

Ineludedobservations:

17

Variable

Coefficient

Std.Error

t-Statistic

Prob.

c

-0.871897

0.108072

-8.067773

0.0000

LNGDP

0.949776

0.022389

42.42107

0.0000

F

-0.005148

0.000892

-5.772612

0.0001

R

0.008510

0.003842

2.214954

0.0469

UU

0.767808

0.074177

10.35100

0.0000

R-squared

0.999451

Meandependentvar

6.379730

AdjustedR-squared

0.999268

S・D.dependentvar

0.800568

S・E.ofregression

0.021665

Akaikeinfocriterion

-4.586298

ruu

LNM1=-0.871897137169+0.949776234674*LNGDP-0.00514818980363*F+0.00851005559974*R+0.767808226881*UU……

(1);

口各个变量均通过显著性水平0.05的检验。

二、对回归的残差序列E1进行平稳性检验:

NullHypothesis:

E1hasaunitroot

Exogenous:

Constant

LagLength:

0(AutomaticbasedonSIC,MAXLAG=3)

t-Statistic

Prob.*

AugmentedDickey-Fullerteststatistic

-5.107454

0.0011

Testcriticalvalues:

1%level

-3.920350

5%level

-3.065585

10%level

-2.673459

其中El为当前模型的残弟序列,由输出结果,可见序列E无单位根,LnMl与各序列协整。

短期动态货币需求函数估计:

按照Hendry建模理论(年度数据从滞后2期开始,季度数据从滞后8期开始删除不显著变量,本实例中我们均采用年度数据,故从滞后2期开始),首先建立一个能够代表数据生成过程(DGP)的口回归分布滞后模型(ADL),然后逐步简化,最后得到包含变量间长期稳定关系的简单的模型。

为使模型尽量包含被解释变量的有效信息,初始阶数设为2。

因样本数冇限,先考虑删除变量uu(-2):

IsInm1cInm1(-1)Inm1(-2)Ingdplngdp(-1)lngdp(-2)ff(-1)f(-2)rr(-1)r(-2)uuuu(-1)

DependentVariable:

LNM1

Method:

LeastSquares

Date:

07/17/11Time:

16:

58

Sample(adjusted):

19952009

Ineludedobservations:

15afteradjustments

Variable

Coefficient

Std.Error

t-Statistic

Prob.

c

-9.055962

0.614180

-14.74480

0.0431

LNM1(-1)

-1.004107

0.109155

-9.198899

0.0689

LNM1(-2)

-2.931779

0.302015

-9.707409

0.0654

LNGDP

2.485006

0.241660

10.28307

0.0617

LNGDP(-1)

-0.698886

0.349553

-1.999368

0.2952

LNGDP(-2)

3.001560

0.229923

13.05466

0.0487

F

0.042536

0.004507

9.438230

0.0672

F(-1)

-0.002784

0.003329

-0.836107

0.5567

F(-2)

0.002340

0.000726

3.224337

0.1915

R

-0.072725

0.009422

-7.718481

0.0820

R(-1)

0.007009

0.003713

1.887663

0.3101

R(-2)

-0.103633

0.007958

-13.02260

0.0488

UU

0.302357

0.051051

5.922635

0.1065

UU(-1)

1.877907

0.168009

11.17742

0.0568

R-squared

0.999998

Meandependentvar

6.548951

AdjustedR-squared

0.999977

S・D.dependentvar

0.686755

S・E.ofregression

0.003324

Akaikeinfocriterion

-9.416429

Sumsquaredresid

1.11E-05

Schwarzcriterion

-8.755582

Loglikelihood

84.62322

Hannan-Quinncriter.

-9.423468

F-statistic

45957.56

Durbin-Watsonstat

3.141988

Prob(F-statistic)

0.003651

二、F(・1)最不显著,

删除它,

加入uu(・2),

IsInm1cInm1(-1)Inm1(-2)Ingdplngdp(-1)lngdp(-2)ff(-2)rr(-1)r(-2)uuuu(-1)uu(-2)

DependentVariable:

LNM1

Method:

LeastSquares

Date:

07/1刀11Time:

17:

01

Sample(adjusted):

19952009

Includedobservations:

15afteradjustments

Variable

Coefficient

Std.Error

t-Statistic

Prob.

c

-12.89349

5.568058

-2.315618

0.2595

LNM1(-1)

-1.635948

0.950277

-1.721548

0.3350

LNM1(-2)

-3.878068

1.621899

-2.391066

0.2522

LNGDP

1.688993

0.953514

1.771335

0.3272

LNGDP(-1)

0.365671

1.794032

0.203826

0.8720

LNGDP(-2)

4.209730

1.566896

2.686668

0.2268

F

0.063352

0.032094

1.973983

0.2985

F(-2)

0.002852

0.000474

6.012757

0.1049

R

-0.076977

0.015734

-4.892565

0.1284

R(-1)

0.002984

0.006767

0.440884

0.7356

R(-2)

-0.132886

0.045488

-2.921369

0.2100

UU

0.166956

0.162842

1.025261

0.4921

UU(-1)

2.550522

1.074927

2.372739

0.2539

UU(-2)

0.450076

0.633246

0.710744

0.6066

R-squared

0.999998Meandependentvar

6.548951

AdjustedR-squared

0.999974

S・D.dependentvar

0.686755

S・E・ofregression

0.003532

Akaikeinfocriterion

-9.295243

Sumsquaredresid

1.25E-05

Schwarzcriterion

-8.634396

Loglikelihood

83.71432

Hannan-Quinncriter.

-9.302282

F-statistic

40712.36

Durbin-Watsonstat

2.861110

Prob(F-statistic)

0.003879

结果显示,模型的参数显著性更差。

结合一、二,构建模型:

IsInm1cInm1(-1)Inm1(-2)Ingdplngdp(-1)lngdp(-2)ff(-2)rr(-1)r(-2)uuuu(-1)

DependentVariable:

LNM1

Method:

LeastSquares

Date:

07/17/11Time:

17:

02

Sample(adjusted):

19952009

Includedobservations:

15afteradjustments

Variable

Coefficient

Std.Error

t-Statistic

Prob.

c

-8.962392

0.556615

-16.10161

0.0038

LNM1(-1)

-0.964646

0.090718

-10.63344

0.0087

LNM1(-2)

-2.734078

0.173178

-15.78771

0.0040

LNGDP

2.352540

0.168192

13.98725

0.0051

LNGDP(-1)

-0.894218

0.239658

-3.731229

0.0649

LNGDP(-2)

3.105674

0.178150

17.43290

0.0033

F

0.040739

0.003651

11.15777

0.0079

F(・2)

0.002820

0.000410

6.884451

0.0205

R

-0.066849

0.005784

-11.55756

0.0074

R(-1)

0.006893

0.003420

2.015449

0.1814

R(-2)

-0.101033

0.006751

-14.96478

0.0044

uu

0.278238

0.038822

7.166955

0.0189

UU(-1)

1.793263

0.123585

14.51032

0.0047

删除LNGDP(・1)、

R(-1)

IsInm1cInm1(-1)Inm1(-2)Ingdplngdp(-2)ff(-2)rr(-2)uuuu(-1)

DependentVariable:

LNM1

Method:

LeastSquares

Date:

07/17/11Time:

17:

08

Sample(adjusted):

19952009

Includedobservations:

15afteradjustments

Variable

Coefficient

Std.Error

t-Statistic

Prob.

c

-9.615586

1.092128

-8.804451

0.0009

LNM1(-1)

-1.213228

0.131889

-9.198865

0.0008

LNM1(-2)

-2.680661

0.350357

-7.651234

0.0016

LNGDP

1.754064

0.111670

15.70763

0.0001

LNGDP(-2)

2.985912

0.345016

8.654416

0.0010

F

0.045525

0.007065

6.443940

0.0030

F(-2)

0.003005

0.000837

3.588955

0.0230

R

-0.057862

0.010737

-5.388866

0.0057

R(-2)

-0.103145

0.013522

-7.628184

0.0016

UU

0.224446

0.074535

3.011259

0.0395

UU(-1)

2.016339

0.223473

9.022734

0.0008

R-squared

0.999976

Meandependentvar

6.548951

AdjustedR-squared

0.999915

S・D.dependentvar

0.686755

S・E.ofregression

0.006317

Akaikeinfocriterion

-7.146120

Sumsquaredresid

0.000160

Schwarzcriterion

-6.626883

Loglikelihood

64.59590

Hannan-Quinncriter.

-7.151651

F-statistic

16544.36

Durbin-Watsonstat

3.567015

Prob(F-statistic)

0.000000

虽然都通过了,

服力,应增加样本容量。

对于LnM2:

同理,LnM2与其他变量二阶单整,故可以对它们进行I■办整关系检验。

构造与LnMl的类似函数,得到估计结果:

IsInm2cIngdpInvfruu

DependentVariable:

LNM2

Method:

LeastSquares

Date:

07/17/11Time:

16:

33

Sample:

19932009

Includedobservations:

17

Variable

Coefficient

Std.Error

t-Statistic

Prob.

c

-0.642088

0.033720

-19.04200

0.0000

LNGDP

1.024316

0.009583

106.8850

0.0000

LNV

-0.004459

0.003323

-1.341862

0.2067

F

・1.45E-05

0.000231

-0.062754

0.9511

R

-0.010236

0.001022

-10.01699

0.0000

UU

0.610529

0.019286

31.65631

0.0000

R-squared

0.999974

Meandependentvar

7.337301

AdjustedR-squared

0.999962

S・D.dependentvar

0.855129

S・E.ofregression

0.005268

Akaikeinfocriterion

-7.383774

Sumsquaredresid

0.000305

Schwarzcriterion

-7.089699

Loglikelihood

68.76208

Hannan-Quinnenter.

-7.354543

F-statistic

84316.59

Durbin-Watsonstat

1.805058

Prob(F-statistic)

0.000000

删除变量LNV、F,重新定义:

IsInm2cIngdpruu

DependentVariable:

LNM2

Method:

LeastSquares

Date:

07/17/11Time:

16:

36

Sample:

19932009

Ineludedobservations:

17

Variable

Coefficient

Std.Errort-Statistic

Prob.

c

-0.609940

0.024676-24.71820

0.0000

LNGDP

1.014727

0.004905206.8710

0.0000

R

-0.009558

0.000888-10.76388

0.0000

UU

0.618246

0.01769434.94077

0.0000

R-squared

0.999969

Meandependentvar

7.337301

AdjustedR-squared

0.999962

S・D.dependentvar

0.855129

S・E.ofregression

0.005264

Akaikeinfocriterion

-7.453626

Sumsquaredresid

0.000360

Schwarzcriterion

-7.257576

Loglikelihood

67.35582

Hannan-Quinncriter.

-7.434138

F-statistic

140753.6

Durbin-Watsonstat

1.519792

Prob(F-statistic)

0.000000

所以估计函数形式为:

LNM2=-0.609940064088+1.01472690347*LNGDP-0.00955847425234*R

+0.618246494611*UU……

(2)

接下來,对当前模型的残并序列E2进行ADF检验:

NullHypothesis:

E2hasaunitroot

Exogenous:

None

LagLength:

0(AutomaticbasedonSIC,MAXLAG=3)

t-Statistic

Prob.*

AugmentedDickey-Fullerteststatistic

-2.870820

0.0071

Testcriticalvalues:

1%level

-2.717511

5%level

-1.964418

10%level

-1.605603

冇结果可知:

E2无单位根,即序列平稳。

公式(3)中各序列存在协整关系。

短期动态模型(修正模型):

IsInm2cInm2(-1)lnm2(-2)Ingdplngdp(-1)lngdp(-2)rr(-1)r(-2)uuuu(-1)uu(-2)(变量的确定应该是根据长期的模型确定的吧,所以没把LnV、F这两个不显著的变量加入到ECM中)

DependentVariable:

LNM2

Method:

LeastSquares

Date:

07/17/11Time:

16:

42

Sample(adjusted):

19952009

Ineludedobservations:

15afteradjustments

Variable

Coefficient

Std.Error

t-Statistic

Prob.

c

-0.970701

0.232131

-4.181701

0.0249

LNM2(-1)

0.458461

0.251274

1.824546

0.1656

LNM2(-2)

-1.032037

0.273756

-3.769919

0.0327

LNGDP

0.885618

0.037914

23.35857

0.0002

LNGDP

升级会员

升级会员