IAS 37.docx

《IAS 37.docx》由会员分享,可在线阅读,更多相关《IAS 37.docx(34页珍藏版)》请在冰豆网上搜索。

IAS37

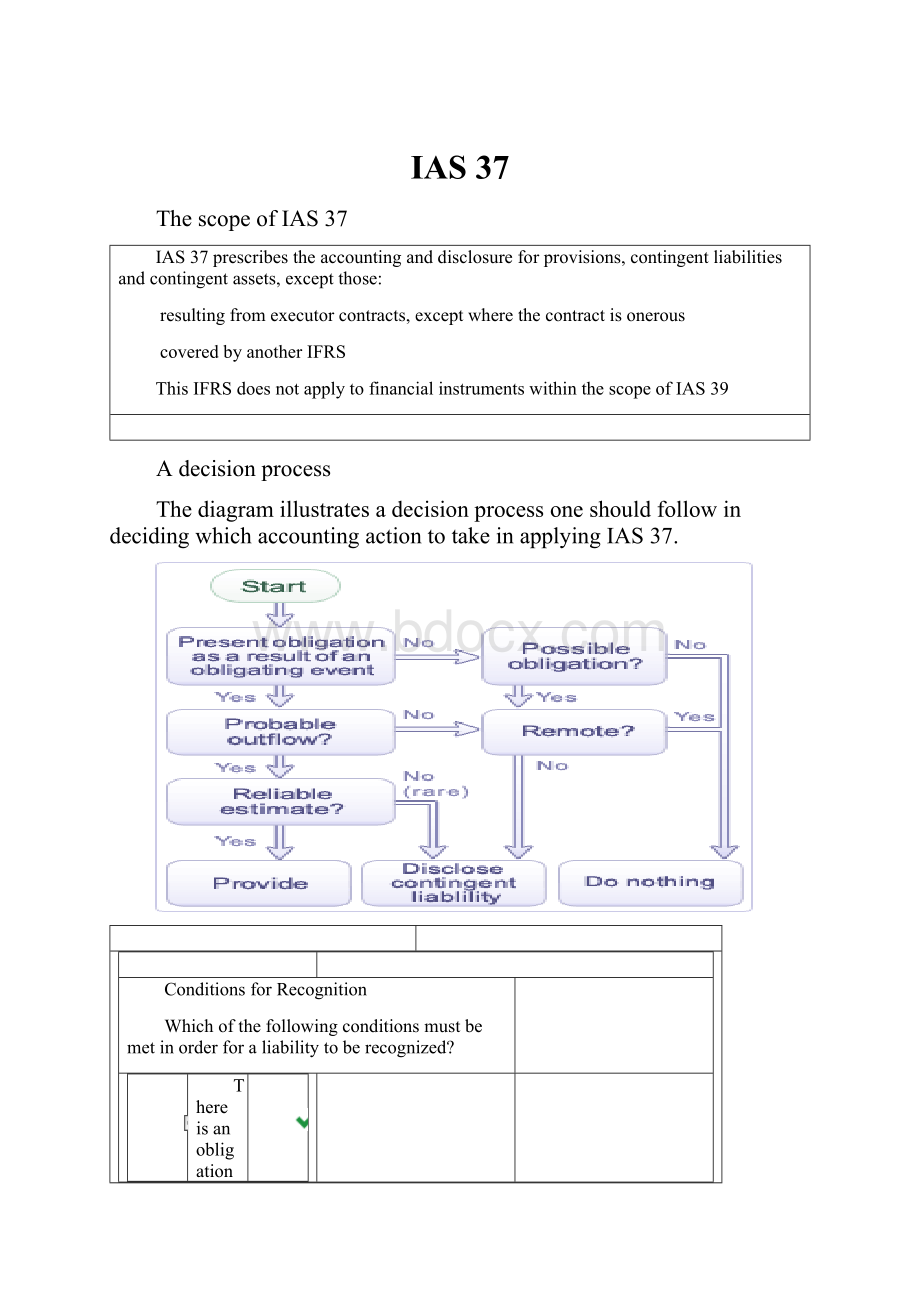

ThescopeofIAS37

IAS37prescribestheaccountinganddisclosureforprovisions,contingentliabilitiesandcontingentassets,exceptthose:

resultingfromexecutorcontracts,exceptwherethecontractisonerous

coveredbyanotherIFRS

ThisIFRSdoesnotapplytofinancialinstrumentswithinthescopeofIAS39

Adecisionprocess

ThediagramillustratesadecisionprocessoneshouldfollowindecidingwhichaccountingactiontotakeinapplyingIAS37.

ConditionsforRecognition

Whichofthefollowingconditionsmustbemetinorderforaliabilitytoberecognized?

Thereisanobligationthatisreliablymeasurable

Anoutflowofeconomicbenefitsisprobable

Thereisanobligationthatwillbeconfirmedbyfutureevents

Anoutflowofeconomicbenefitsispossible

Thereisapresentobligationasaresultofpastevents

Futureoperatinglossesareprobable

Welldone.

Aliabilityshouldberecognisedwhen:

anenterprisehasapresentobligationasaresultofapastevent

anoutflowofresourcesembodyingeconomicbenefitswillprobablyberequiredtosettletheobligation

theamountoftheobligationcanbereliablyestimated

Scenario1

Year-endforOKRadiosisfastapproachingcompletion,andasafinancialmanager,thereareseveralissuesyouwillbedealingwithtoday.

Hi,Thisisadebatewe'vebeenhaving-canyouhelp?

OKRadiosdoesnotgivewarrantiestocustomerspurchasingourkeyproduct.However,overanumberofyearswehavehadapolicyofrepairingorreplacingdefectivegoodswithinthreeyearsofsale.Judgingbytheirpastrecord,therewillprobablybeacertainproportionofgoodsreturned.

JohnandNickibelievethattheobligationtorepairortoreplacethegoodsshouldberecognisedwhendefectivegoodsarereturnedbythecustomer,whilePaulinsiststhattheobligatingeventisthesaleofthegoods.Canyouhelp?

Thanks

Mandy

So,asyoucangatherfromMandy'semail,someoftheteambelievethattheobligatingeventisthesaleofthegoods,whileothersbelieveitisthereturnofthegoods.

WhichofthefollowingeventsobligatesOKRadiostorepairtheradio?

Thereturnofthegoodsbythecustomer

Thesaleofthegoodstothecustomer

Neither-thereisnoobligatingevent

Welldone.

Theobligatingeventfortheprovisionisthesaleofthegoods-itisatthistimethatavalidexpectationarisesonthepartofthecustomersthatfaultygoodswillberepairedorreplaced.

Atthispointtheentitycannotrealisticallyavoidtheoutflowofeconomicbenefits.

Scenario2

Thanksforyourhelpwithdeterminingtheobligatingeventoftheliability.Sorrytobotheryouagain,butIunderstandtherearetwotypesofobligatingevents,namelyconstructiveandlegalobligation.Istheaccountingdifferentforeachtypeofobligation?

Whatkindofobligationdowehave?

Andhowdoesthetypeofobligationaffecttheaccounting?

Thetypeofobligation

Aconstructiveobligationcreatesanexpectation,whereasalegalobligationcreateslegalrights.ThepastpracticeofrepairingtheradioscreatesanexpectationthatallfaultyradioswillberepairedbyOKRadios.OKRadiosnowhasnorealisticalternativetohonouringtheirpolicyasexpected.

Howthetypeaffectstheaccounting

Thetypeoftheobligationdoesnotchangetheaccounting.Ratherthisknowledgehelpsindecidingwhentorecogniseaprovision.OKRadioswillrecogniseaprovisionwhentheymakeasale.Ifitwasalegalobligation,theobligatingeventwouldbeacourtrulingagainstOK.OKwouldonlybeabletorecognisetheliabilityafterthecustomerhasmadetheclaimagainstOKanditisprobablethatOKwilllosethecourtcase.

Whichofthefollowingconditionsdoyoubelievetobenecessaryforrecognisingaliability?

SelectoneormoreoptionsandclickConfirm.

Apossibleobligationoftheentity

Anobligationarisingfrompastevents

Anobligationwhichwillbeconfirmedbyfutureevents

Apresentobligationoftheentity

Thesettlementisexpectedtoleadtoanoutflowofeconomicbenefits

Whatisanobligatingevent?

Apasteventthatleadstoapresentobligationiscalledanobligatingevent.IAS37definesanobligatingeventas:

∙aneventthatcreatesalegalorconstructiveobligationthatresultsintheentityhavingnorealisticalternativetosettlingthatobligation

Anentitywillhavenorealisticalternativetosettlinganobligationcreatedbyaneventonly:

∙wherethesettlementoftheobligationcanbeenforcedbylaw(alegalobligation),or

∙wheretheeventcreatesvalidexpectationsinotherpartiesthatitwilldischargetheobligation(aconstructiveobligation)

Anobligatingevent?

Duringthefestiveseason,atelephoneentityputsupanoticeinitswindow,tellingcustomersthatiftheybuyanewtelephone,theywillreceiveasecondhandsetforfree.Thecustomerthereforeexpectstogettwotelephonesforthepriceofone.Isthereanobligatingeventhere?

Ifso,whichofthefollowingisit?

Clicktheonecorrectoption,andthenclickConfirm.

Thepostingofthenoticeinthewindow

Thesaleofthefirsttelephone

Thereisnoobligatingevent

Welldone.

Byplacingthenotice,theentityhascreatedavalidexpectationonthepartofthecustomerthatanadditionalhandsetwillbeprovidedforfreeifthecustomerbuysthefirsthandset.

Theobligatingevent,therefore,isthesaleofthehandset.Thisisanexampleofaconstructiveobligation.

Alegalobligationisanobligationthatderivesfromacontract(throughitsexplicitorimplicitterms),legislation,orotheroperationoflaw

Example:

Aentityisfoundguiltyofbreachingacontract,anditwillberequiredtopayindemnities.Theamountandtimingoftheobligationareuncertain

Aconstructiveobligationisanobligationthatderivesfromanentity'sactionswhere:

∙byanestablishedpatternofpastpractice,publishedpoliciesoraspecificcurrentstatement,theentityhasindicatedtootherpartiesthatitwillacceptcertainresponsibilities,and

∙asaresult,theentityhascreatedavalidexpectationonthepartofthoseotherpartiesthatitwilldischargethoseresponsibilities

Example:

Astoreadvertisesaguaranteeonitsgoods,specifyingthatcustomerswillgetarefundiftheyarenotsatisfied.Althoughthereisnowrittencontractorlegalobligation,thestoreiscreatingavalidexpectationthatitwillhonouritsguarantee

EstimatingtheProbability

Acourtcase

Welldone-nowtomoveontootherissuesarisingatOKRadios.

TwoofOKRadios'consultantshaveresigned.Thereasongivenwasa15%reductionintheirusualsalaries-theyhadrefusedtoworkovertimeastheyhadinpreviousmonths,becausetheywantedtospendmoretimewiththeirfamilies.Subsequently,theemployeeshavetakentheemployertocourt,suingforconstructivedismissal(creatingunfavourableworkingconditions).Thecaseisnowinthefinalstages,andarulingisexpectedwithintheweek.

Theentity'slawyersbelievethatthecourtwillruleinfavouroftheemployees.TheyhavebroughttoOK'sattentionasimilarrecentcaseinwhichthecourtawardedtheemployeestwoyears'salary,rulingthattheywereconstructivelydismissed.

Accordingtoourlawyers,we'reprobablylookingatapayoutonthiscourtcase.Theiropinionabouttheprobabilityisasfollows:

∙a70%chanceofapayoutoftwoyears'salary(€100,000peremployee)

∙a20%chanceofapayoutofthreeyears'salary(€150,000peremployee)

∙a10%chanceofapayoutofoneyear'ssalary(€50,000peremployee)

Canyouletmeknowifthisissufficientinformationtoestablishtheprobabilityoftheoutcomeandifyouwantmetorecogniseaprovisionforthis?

OKRadiosareinvolvedinacourtcasewithtwoformeremployees,andDavidwantstoknowifOKshouldmakeaprovisionfortheoutflowofresourcesthatmayresultfromthecase.

Selecttheactionsyouwouldtaketoestablishtheprobabilityoftheliability.

Consulttheemployees

Assesstheopinionofthelawyers

Studysimilarrecentcases

Assessalloftheevidenceavailable

Welldone.

Youshouldassessallavailableevidence,includingrecentsimilarcasesandtheopinionsofthelawyers.Thestrongestevidencesupportingtheprobabilityofoutflowofeconomicbenefitsisthelawyers'opinionandexperienceofprevioussimilarcourtcases.

BestEstimateforMostLikelyOutcome

GivethebestestimateoftheliabilityregardingthecaseforconstructivedismissalbroughtbyOKRadios'formeremployees,basedonthemostlikelyoutcome.

UsethefiguresDavidSmithmailedtoyou.

Clicktheonecorrectoption,andthenclickSubmit.

€110,000

€300,000

€200,000

Welldone.

Asthereisa70%chancethattheliabilitywillbefor€100,000peremployee(i.e.€200,000),thisisthemostlikelyoutcome.Asthisliabilityisarisingoutofasingleissue,thisisprobablythebestestimate.

Davidtellsmeweshouldraisealiabilityof€200,000forthependingcourtcase.ButIunderstandthatthereisanotherwayofcalculatingprovisionstoo.Canyougiveusafigureforthe"expectedoutflow"aswell?

Isuggestwecomparethefigures,sowehavealltheinformation–youknowhowtheauditorsare?

!

Measurement–ExpectedOutflow

SarahhassentaMemorequestinganothercalculationofthefiguresregardingtheconstructivedismissalcase,toshowtheexpectedoutflowunder

升级会员

升级会员