计量经济作业.docx

《计量经济作业.docx》由会员分享,可在线阅读,更多相关《计量经济作业.docx(27页珍藏版)》请在冰豆网上搜索。

计量经济作业

计量经济学平时作业

第二章第十题

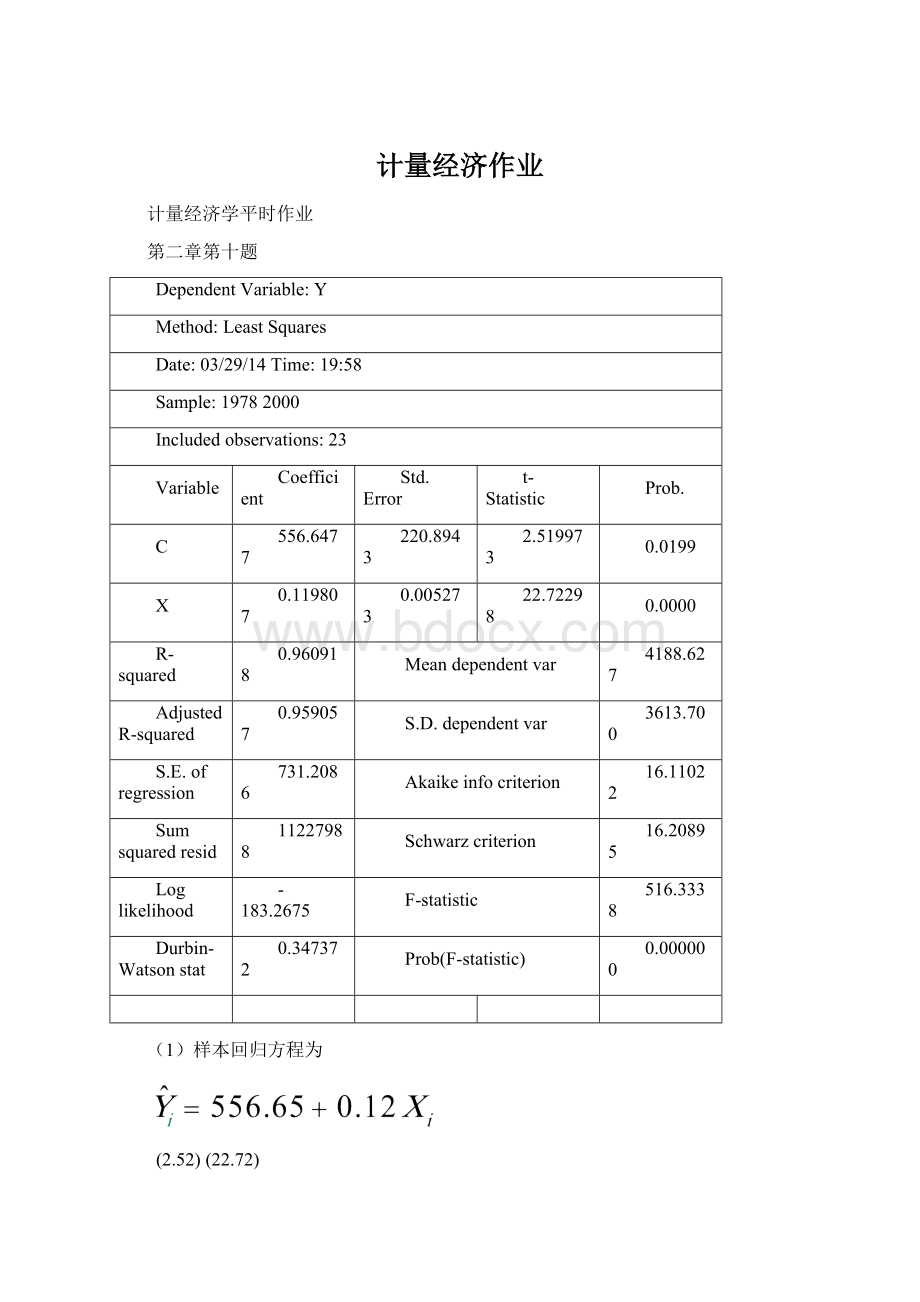

DependentVariable:

Y

Method:

LeastSquares

Date:

03/29/14Time:

19:

58

Sample:

19782000

Includedobservations:

23

Variable

Coefficient

Std.Error

t-Statistic

Prob.

C

556.6477

220.8943

2.519973

0.0199

X

0.119807

0.005273

22.72298

0.0000

R-squared

0.960918

Meandependentvar

4188.627

AdjustedR-squared

0.959057

S.D.dependentvar

3613.700

S.E.ofregression

731.2086

Akaikeinfocriterion

16.11022

Sumsquaredresid

11227988

Schwarzcriterion

16.20895

Loglikelihood

-183.2675

F-statistic

516.3338

Durbin-Watsonstat

0.347372

Prob(F-statistic)

0.000000

(1)样本回归方程为

(2.52)(22.72)

=0.96F=516.33

经济意义:

解释变量的系数为0.12,说明国内生产总值没增加1亿元,将有0.12亿元为财政收入,这是符合经济意义的。

散点图如下:

(2)

1).拟合优度检验:

=0.96

说明在总离差平方和中有96%的部分被回归直线解释,仅有4%未被解释,因此,样本回归直线对样本点的拟合优度较好。

2).显著性检验:

给出显著性水平

,自由度v=23-2=19,得临界值

=2.09

故t0=2.52>2.09t1=22.72>2.09,故回归系数均显著不为零,X对Y有显著影响。

(3)

点预测:

X=105709

故Y=13241.73

区间预测:

Y的区间预测为(11480.79,15000.67)

第三章第七题(课件)

DependentVariable:

Y

Method:

LeastSquares

Date:

04/1/14Time:

21:

11

Sample:

110

Includedobservations:

10

Variable

Coefficient

Std.Error

t-Statistic

Prob.

C

626.5093

40.13010

15.61195

0.0000

X1

-9.790570

3.197843

-3.061617

0.0183

X2

0.028618

0.005838

4.902030

0.0017

R-squared

0.902218

Meandependentvar

670.3300

AdjustedR-squared

0.874281

S.D.dependentvar

49.04504

S.E.ofregression

17.38985

Akaikeinfocriterion

8.792975

Sumsquaredresid

2116.847

Schwarzcriterion

8.883751

Loglikelihood

-40.96488

F-statistic

32.29408

Durbin-Watsonstat

1.650804

Prob(F-statistic)

0.000292

(1).估计参数

=626.5093,

=-9.790570,

=0.028618

=302.41,

=0.902218,

=0.874281

(2).F检验:

:

由表可知,F统计量为32.29,给定显著性水平0.05,则

=4.74,因为F统计量大于4.74,所以拒绝原假设,总体回归方程是显著的,即该社区家庭消费支出与商品单价和家庭月收入之间在总体上存在显著的线性关系。

T检验:

由表可知,

,给定显著性水平0.05,查表得

=2.37,

和

的绝对值都大于2.37,所以否定

即商品单价对该社区家庭消费有显著影响,家庭月收入对该社区家庭消费也有显著影响。

置信区间:

经计算得

两个端点分别为-17.374和-2.206,

的两个端点分别为0.015和0.043,所以

95%的置信区间是(-17.374,-2.206),

95%的置信区间是(0.015,0.043)。

第四章第三题

由题意得:

两边取对数,可得到

令=,=,,=,=,=,=,

即可将原函数模型转化成标准的二元线性回归模型

W

X1

X2

8.222204

8.032107

4.727388

7.274147

7.429183

4.204693

7.468724

7.916724

4.430817

7.280208

7.587726

3.295837

8.546616

8.685587

5.789960

7.736814

7.472370

4.787492

7.204276

6.844922

4.060443

6.487334

6.543826

3.433987

5.913989

5.895724

2.772589

7.371716

7.828831

4.189655

6.424399

6.881134

4.060443

6.426391

6.246126

3.332205

8.395972

8.239042

4.110874

8.656785

9.069701

5.537334

7.485138

7.936982

4.418841

7.125339

7.500220

3.496508

6.700362

7.020021

3.761200

7.549451

7.626648

4.110874

8.214154

8.718191

5.480639

8.462293

9.130025

5.402677

7.687186

7.960899

4.382027

7.839825

7.842133

4.564348

8.021896

8.473847

5.402677

7.692857

8.088037

5.093750

DependentVariable:

Y

Method:

LeastSquares

Date:

04/07/14Time:

10:

02

Sample:

131

Includedobservations:

31

Variable

Coefficient

Std.Error

t-Statistic

Prob.

C

1.153994

0.727611

1.586004

0.1240

X1

0.609236

0.176378

3.454149

0.0018

X2

0.360796

0.201591

1.789741

0.0843

R-squared

0.809925

Meandependentvar

7.493997

AdjustedR-squared

0.796348

S.D.dependentvar

0.942960

S.E.ofregression

0.425538

Akaikeinfocriterion

1.220839

Sumsquaredresid

5.070303

Schwarzcriterion

1.359612

Loglikelihood

-15.92300

F-statistic

59.65501

Durbin-Watsonstat

0.793209

Prob(F-statistic)

0.000000

所以所得回归方程为

。

第五章第六题

DependentVariable:

Y

Method:

LeastSquares

Date:

04/21/14Time:

16:

40

Sample:

120

Includedobservations:

20

Variable

Coefficient

Std.Error

t-Statistic

Prob.

C

272.3635

159.6773

1.705713

0.1053

X

0.755125

0.023316

32.38690

0.0000

R-squared

0.983129

Meandependentvar

5199.515

AdjustedR-squared

0.982192

S.D.dependentvar

1625.275

S.E.ofregression

216.8900

Akaikeinfocriterion

13.69130

Sumsquaredresid

846743.0

Schwarzcriterion

13.79087

Loglikelihood

-134.9130

F-statistic

1048.912

Durbin-Watsonstat

1.301684

Prob(F-statistic)

0.000000

1.

即为人均消费支出与可支配收入之间的线性模型。

2.

怀特检验

WhiteHeteroskedasticityTest:

F-statistic

14.63595

Probability

0.000201

Obs*R-squared

12.65213

Probability

0.001789

因为TR*2>

=3.841,所以该回归模型中存在异方差。

由图示法也可以得到相同的结果。

3.

E1与X^1/2

DependentVariable:

E1

Method:

LeastSquares

Date:

04/21/14Time:

17:

18

Sample:

120

Includedobservations:

20

Variable

Coefficient

Std.Error

t-Statistic

Prob.

X^(1/2)

2.315339

0.243625

9.503697

0.0000

R-squared

0.326056

Meandependentvar

177.2539

AdjustedR-squared

0.326056

S.D.dependentvar

107.2046

S.E.ofregression

88.00868

Akaikeinfocriterion

11.84145

Sumsquaredresid

147165.0

Schwarzcriterion

11.89124

Loglikelihood

-117.4145

Durbin-Watsonstat

1.382822

E1与X

DependentVariable:

E1

Method:

LeastSquares

Date:

04/21/14Time:

17:

21

Sample:

120

Includedobservations:

20

Variable

Coefficient

Std.Error

t-Statistic

Prob.

X

0.028126

0.002424

11.60484

0.0000

R-squared

0.520566

Meandependentvar

177.2539

AdjustedR-squared

0.520566

S.D.dependentvar

107.2046

S.E.ofregression

74.22977

Akaikeinfocriterion

11.50091

Sumsquaredresid

104691.1

Schwarzcriterion

11.55070

Loglikelihood

-114.0091

Durbin-Watsonstat

1.960065

E1和X^2

DependentVariable:

E1

Method:

LeastSquares

Date:

04/21/14Time:

17:

24

Sample:

120

Includedobservations:

20

Variable

Coefficient

Std.Error

t-Statistic

Prob.

X^2

3.30E-06

3.29E-07

10.03804

0.0000

R-squared

0.384817

Meandependentvar

177.2539

AdjustedR-squared

0.384817

S.D.dependentvar

107.2046

S.E.ofregression

84.08445

Akaikeinfocriterion

11.75023

Sumsquaredresid

134333.7

Schwarzcriterion

11.80001

Loglikelihood

-116.5023

Durbin-Watsonstat

1.688103

EI和X^3/2

DependentVariable:

E1

Method:

LeastSquares

Date:

04/21/14Time:

17:

25

Sample:

120

Includedobservations:

20

Variable

Coefficient

Std.Error

t-Statistic

Prob.

X^(3/2)

0.000316

2.68E-05

11.78825

0.0000

R-squared

0.533588

Meandependentvar

177.2539

AdjustedR-squared

0.533588

S.D.dependentvar

107.2046

S.E.ofregression

73.21471

Akaikeinfocriterion

11.47338

Sumsquaredresid

101847.5

Schwarzcriterion

11.52316

Loglikelihood

-113.7338

Durbin-Watsonstat

2.093814

W=1/e

WhiteHeteroskedasticityTest:

F-statistic

0.032603

Probability

0.967983

Obs*R-squared

0.076420

Probability

0.962511

TestEquation:

DependentVariable:

STD_RESID^2

Method:

LeastSquares

Date:

04/25/14Time:

10:

09

Sample:

120

Includedobservations:

20

Variable

Coefficient

Std.Error

t-Statistic

Prob.

C

6196.481

11798.68

0.525184

0.6062

X

-0.165323

3.304793

-0.050025

0.9607

X^2

4.80E-06

0.000211

0.022745

0.9821

R-squared

0.003821

Meandependentvar

5342.798

AdjustedR-squared

-0.113377

S.D.dependentvar

3140.196

S.E.ofregression

3313.430

Akaikeinfocriterion

19.18684

Sumsquaredresid

1.87E+08

Schwarzcriterion

19.33620

Loglikelihood

-188.8684

F-statistic

0.032603

成立消除了异方差,所以

=6196.48,

=-0.165

W=1/x

WhiteHeteroskedasticityTest:

F-statistic

1.111395

Probability

0.351865

Obs*R-squared

2.312660

Probability

0.314639

TestEquation:

DependentVariable:

STD_RESID^2

Method:

LeastSquares

Date:

04/25/14Time:

10:

12

Sample:

120

Includedobservations:

20

Variable

Coefficient

Std.Error

t-Statistic

Prob.

C

-67139.63

78728.82

-0.852796

0.4056

X

25.38176

22.05183

1.151004

0.2657

X^2

-0.001467

0.001408

-1.042164

0.3119

R-squared

0.115633

Meandependentvar

29670.20

AdjustedR-squared

0.011590

S.D.dependentvar

22238.71

S.E.ofregression

22109.46

Akaikeinfocriterion

22.98288

Sumsquaredresid

8.31E+09

Schwarzcriterion

23.13224

Loglikelihood

-226.8288

F-statistic

1.111395

Durbin-Watsonstat

1.713243

Prob(F-statistic)

0.351865

消除了异方差,所以参数为

=-67139.63,

=25.38.

第六章第五题

1.一元线性模型

DependentVariable:

Y

Method:

LeastSquares

Date:

05/04/14Time:

08:

09

Sample:

19602001

Includedobservations:

42

Variable

Coefficient

Std.Error

t-Statistic

Prob.

C

-3028.563

655.4268

-4.620749

0.0000

X

0.697492

0.019060

36.59467

0.0000

R-squared

0.970997

Meandependentvar

10765.23

AdjustedR-squared

0.970272

S.D.dependentvar

20154.12

S.E.ofregression

3474.938

Akaikeinfocriterion

19.19099

Sumsquaredresid

4.83E+08

Schwarzcriterion

19.27373

Loglikelihood

-401.0108

F-statistic

1339.170

Durbin-Watsonstat

0.178439

Prob(F-statistic)

0.000000

一元线性回归估计方程Y=-3028.563+0.697x

2.残差图

3.DW=0.178439

一阶自相关检验存在

Breusch-GodfreySerialCorrelationLMTest:

F-statistic

327.3780

Probability

0.000000

Obs*R-squared

37.52921

Probability

0.000000

TestEquation:

DependentVariable:

RESID

Method:

LeastSquares

Date:

05/05/14Time:

08:

14

Presamplemissingvaluelaggedresidualssettozero.

Variable

Coefficient

Std.Error

t-Statistic

Prob.

C

-312.6482

221.1676

-1.413626

0.1656

X

0.026360

0.007930

3.324113

0.0020

RESID(-1)

1.366995

0.155705

8.779407

0.0000

RESID(-2)

-0.319088

0.178289

-1.789723

0.0815

R-squared

0.901828

Meandependentvar

-3.29E-12

AdjustedR-squared

0.894077

S.D.dependentvar

3432.299

S.E.ofregression

1117.068

Akaikeinfocriterion

16.96520

Sumsquaredresid

47417961

Schwarzcriterion

17.13069

Loglikelihood

-352.2691

F-statistic

116.3582

Durbin-Watsonstat

1.756459

Prob(F-statistic)

0.000000

P=1-0.178439/2=0.91

4.广义差分法

DependentVariable:

Y1

Method:

L

升级会员

升级会员