EVIEWS操作各种模型学习.docx

《EVIEWS操作各种模型学习.docx》由会员分享,可在线阅读,更多相关《EVIEWS操作各种模型学习.docx(49页珍藏版)》请在冰豆网上搜索。

EVIEWS操作各种模型学习

章、图形基础与回归

原始数据

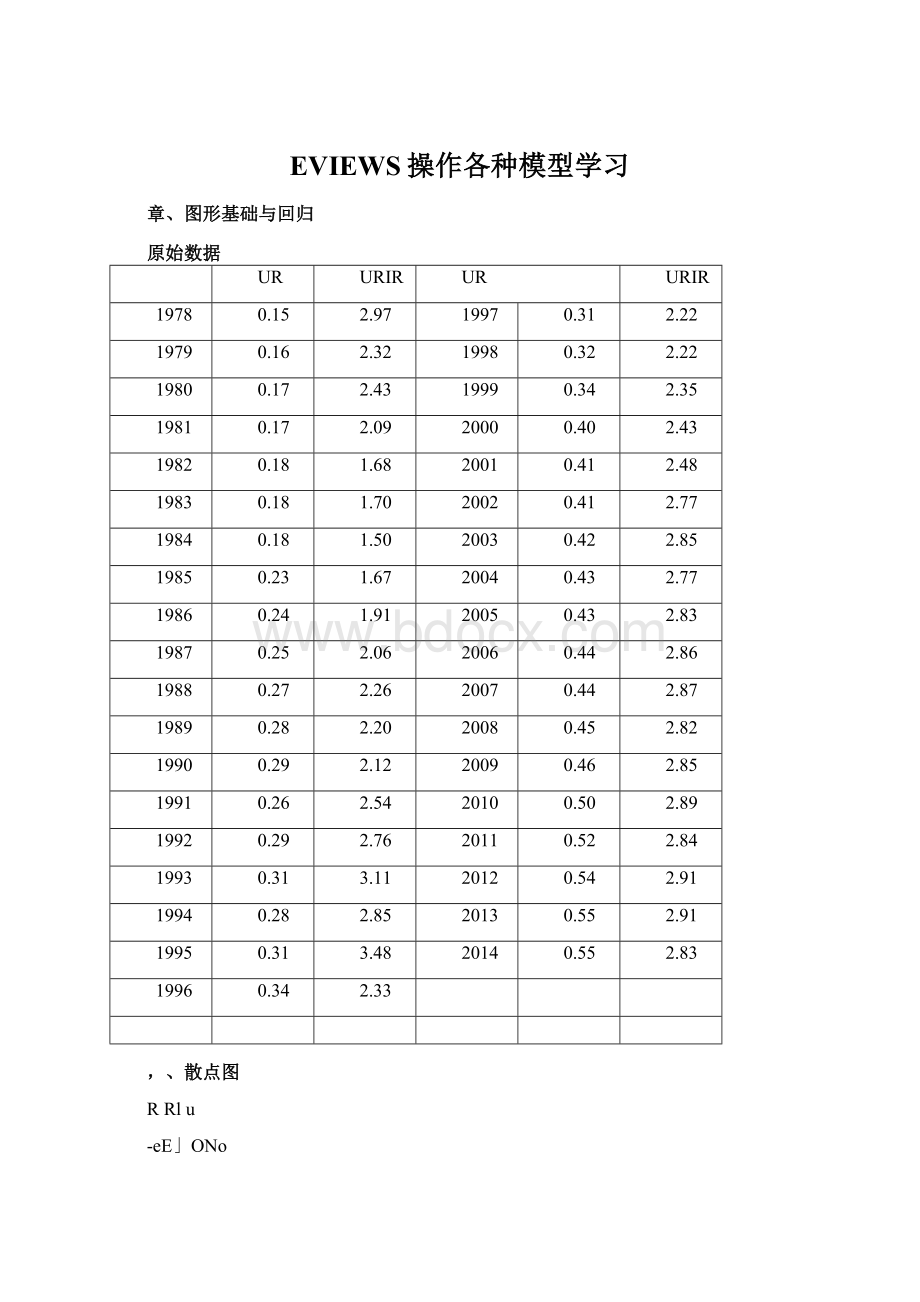

UR

URIR

UR

URIR

1978

0.15

2.97

1997

0.31

2.22

1979

0.16

2.32

1998

0.32

2.22

1980

0.17

2.43

1999

0.34

2.35

1981

0.17

2.09

2000

0.40

2.43

1982

0.18

1.68

2001

0.41

2.48

1983

0.18

1.70

2002

0.41

2.77

1984

0.18

1.50

2003

0.42

2.85

1985

0.23

1.67

2004

0.43

2.77

1986

0.24

1.91

2005

0.43

2.83

1987

0.25

2.06

2006

0.44

2.86

1988

0.27

2.26

2007

0.44

2.87

1989

0.28

2.20

2008

0.45

2.82

1990

0.29

2.12

2009

0.46

2.85

1991

0.26

2.54

2010

0.50

2.89

1992

0.29

2.76

2011

0.52

2.84

1993

0.31

3.11

2012

0.54

2.91

1994

0.28

2.85

2013

0.55

2.91

1995

0.31

3.48

2014

0.55

2.83

1996

0.34

2.33

,、散点图

RRlu

-eE」ONo

:

、分布图:

JB>3判断为正太分布

Series:

UR

Sample137

Observations37

Mean

0.336145

Median

0.312400

Maximum

0.547000

Minimum

0.15087-

Std.Dev.

0.120626

Skewness

0.143256

Kurtosis

1.887565

Jarque-Bera

2.034384

Probability

0.361609

三、UR的单因素联表

TabulationofUR

Date:

09/05/15Time:

21:

25

Sample:

137

Includedobservations:

37

Numberofcategories:

5

Value

Count

Percent

Cumulative

Count

Cumulative

Percent

[0.1,0.2)

7

18.92

7

18.92

[0.2,0.3)

9

24.32

16

43.24

[0.3,0.4)

6

16.22

22

59.46

[0.4,0.5)

11

29.73

33

89.19

[0.5,0.6)

4

10.81

37

100.00

Total

37

100.00

37

100.00

四、协方差与相关性

CovarianceAnalysis:

Ordinary

Date:

09/05/15Time:

21:

40

Sample:

137

Includedobservations:

37

Covariance

Correlation

UR

URIR

UR

0.014157

1.000000

URIR

0.033170

0.204852

0.615934

1.000000

Date:

09/05/15Time:

21:

44

Sample:

137

Includedobservations:

37

Correlationsareasymptoticallyconsistentapproximations

URrURlR(-i)

UR,URIR(+i>

lag

lead

Oi

0

0.6159

0.&159

1

0.5767

0.6549

2

0.4997

0.6515

3

0.4282

0.6384

4

0.3795

0.5755

5

0.3621

0.4990

6

0.3267

0.4159

7

0.3292

0.2918

8

0.2983

0.1732

9

0.2585

0.0795

10

0.1997

0.0124

11

0.1420

-0.0556

12

□0809

-0.0998

13

0.0097

-0.1538

14

-0.0231

■0.1740

15

-0.033B

-0.1790

16

-0.0565

*0.1401

17

-0.0433

-0.1238

18

-0.0316

-0.0532

19

-0.0395

-0.0939

20

-0.1629

-0.1381

五、CDF经验分布图

六、Q-Q图

URIR

QuantilesofURIR

七、回归散点图

UR

邻近拟合散点图:

(分布回归的结果)

八、实际值、拟合值、残差值折线图

ResidualActualFitted

9

StandardizedResiduals

九、回归模型预测

URF—±2S.E

Forecast:

URF

Actual:

UR

Forecastsample:

137

Includedobservations:

37

RootMeanSquaredError0.093736

MeanAbsoluteError0.072711

MeanAbs.PercentError25.93140

TheilInequalityCoefficient0.133790

BiasProportion0.000000

VarianeeProportion0.237674

CovarianeeProportion0.762326

十、两回归系数的联合检验置信区间是一个椭圆区域

C

(1)

!

^一、Wald系数约束条件检验

WaldTest:

Equation:

Untitled

TestStatistic

Value

df

Probability

F-statisticChi-square

272.1503

272.1503

(1.35)

1

0.0000

0.0000

NullHypothesisSummary:

NormalizedRestriction[=Q)

Value

Std.Err,

-1+C

(1)+C

(2)

-0,907527

0.055012

RestrictionsarelinearincgeAI匚ients

Chow分割点检验结果

ChowBreakpointTest1991

NullHypothesis:

Nobreaksatspecifiedbreakpoints

Varyingregressors:

Allequationvariables

EquationSample:

19782014

F'Statistic

11.00551

Prob.F(2r33)

0.0002

Loglikelihoodratio

18.90797

Prob,Chi-Square

(2)

0.0001

WaldStatistic

22.01103

Prob.Chi-Squa(e

(2)

0.0000

F、LR的P值显著,表示:

模型无显著的结构变化

十二、Chow稳定性检验(p75)

Chow预测结果:

ChowForecastTest:

Forecastfrom1991to2014

F-statistic

Loglikelihoodratio

4.744782

89.83840

PfOb.F(24,11)

Prob.Chi-Square(24)

0.0050

0.0000

TestEquation:

DependentVariable:

URMethod:

LeastSquares

Date:

09/07/15Time:

10:

31

Sample:

197S1990

Included!

observations:

13

Coefficient

Std.Errort-Statistic

Prob.

URIR

C

-0014716

0.241289

0.037436-0393094

0.0787753.063016

07018

0.0100

R-squared

AdjustedR-squared

S.Eofregression

SumsquaredresidLoglikelihoodF-statistic

Prob(F-statistic)

0.013853

*0.075797

0.051024

0.028637

21.32073

0.154523

0.701762

Lieandependentvar

S.Ddependentvar.Akaikeinfocriterion

SchwarzcriterionHannan-Ouinncriter.

Durbin-Watsonstat

0.210827

0.049193

2972421-2.885505-2990286

0.127458

十三、零均值附近的递归残差曲线图

2

2•递归OLS的CUSUM检验曲线图(p78)

CUSUM5%Significance

*注:

红线为5%的临界值线,在1991年后的CUSUM曲线变得十分陡峭,说明:

回归方程系数并不是稳定的。

3.—步预测检验:

N-StepProbabilityRecursiveResiduals

One-Step

Probability

Recursiv

eResiduals

*注:

上部分是递归残差,下部分是检验显著性的概率

.3

RecursiveC⑴Estimates士2S.E.

RecursiveC

(2)Estimates士2S.E.

十四、White异方差检验

Obs*R-squared=10.4,其P值=0.0055表示残差存在异方差性。

F统计量表示:

检验辅助方程的整体显著性,下图中整体显著。

HeteroskedasticityTest:

White

F-statistic

6.658663

Prob.F(2.34)

0.0036

Obs*R-squared

10.41354

ProbChi-Square

(2)

0.0055

ScaieCexplainedSS

10,36651

Prob.ChkSquare{2)

0,0056

TestEquation:

DependentVariaDle:

RESIDA2Method:

LeastSquares

Date:

09/07/15Time:

11:

02

Sample:

19782014

Irt匚ludedobservations:

37

CoefficientStd.Errort-StatisticProb.

C

0.039819

0.0458S60.867779

0.3916

URIR

-0.042859

0038582-1110863

0.2744

URIRA2

0.011780

0.0079411.483508

0.1472

R-squared

0.281447

Meandependentvar

0.008786

AdjustedR-squared

0239179

S.D.dependentvar

0013287

S.Eofregression

0.011590

Akaikeinfocriterion

-5999002

Sumsquaredresid

0.004567

£匚hwamcriterion

-5.869187

Loglikelihood

1139963

Hannan*Quinnenter.

-5953754

F-statistic

6.658663

Durbin-Watsonstat

0.374222

Prob(F-statistic)

0.003629

十五、WLS加权最小二乘法

DependentVariable:

UR

Method:

LeastSquaresDate:

09/07/15Time:

11:

29

Sample:

19782014includedobservations:

37

Weightingseries:

W

Coefficient

Std.Error

t-Statistic

Prob.

URIR

0.168557

0.031139

5,413033

0.0000

C

-0.086069

0.076542

-1.124465

0.2685

WeightedStatistics

R-squared

0.455684

(Jeandependentvar

0.328603

AdjustedR-squared

0440132

S.Ddependentvar

0.100794

SE,ofregression

0.090040

Akaikeinlacriterion

*1.924588

Sumsquaredresid

0.283752

Schwarzcriterion

-1,837512

LogliKelitiaod

37.50488

Hannan-Quinncriter

-1893890

F-statistic

29.30092

Durbin-Watsonstat

0.279531

Prob(F-statistic)

0.000005

UnweightedStatisti匚s

R-squared

□378738

Meandependentvar

0.33614S

AdjustedR-squared

0.350987

SD.dependentvar

0.120526

S.E.ofregression

0.096427

Sumsquaredresid

0.325433

Durbin-Watsonstat

0.310271

十六、残差自相关图及其Q检验统计量

CorrelogramofResiduals

Date:

09/07/15Time:

15:

50

Sample:

19782014

Includedobservations:

37

AutocorrelationPartialCorrelationACPACQ-StatProb

1

1

1

1

1

□1

10.7120.71220.3330000

205730133338500000

1

二

1匚

II

30.380-014239.9630.000

1

1[

1

40.239-005942.4520.000

II

]1

1(

1

50.111-0.05543.0060000

II

】>

H

]1

60.0600.05243.1760.000

1

]>

H

]1

70.0530.07843.3100.000

II

]>

H

]1

&0.0680.04243.5390.000

II

]>

1(

II

90.056-0.05143.6980.000

1

1>

1

]1

100.0340.05044.0750000

1

11

1

]1

110.11S008244.3430000

1

□1

1

11

120.157007246.2730000

1

n>

1

:

1

130.217011449.1000.000

II

ZI|

1[

1

140.203-0.06751.6340.000

1

□>

1匚

1

150148-0.11953.1140.000

1

1

1匚

1

150024-0.17153.1520.000

1-16阶的p值都小于0.01,说明拒绝原假设,残差序列存在自相关性。

十七、残差自相关LM检验结果

Breuscn-GocrrreyserialCorrslatJonLMT©st:

F-statistic

Otl£*R-£.口1_1自「耳€]

N石4640•尹

Rrot>F<2,33)

Pro.Chi-Scilj岂

DOOOO

0.0000

TestEqliation:

DepenitjentVaria&le'RSSIO

Metnodii_eastSquares

Date:

09/07/15Time:

1

Sampile:

19ZB201^

lindudiedolbservations.37

PreSainnp0&llue1日口些旦日「孕导iClinH导settozi^ro

Coefficient

Std.Error

t-Statisti匚

Proti.

URIRo

RESIDC-1)

RESIDC-2)

-O„O49356O-12B67OO.63&8SSOJ284L8O9

0.02:

3318OO日口日64Q.16S1Z3

Ck"4374

-2.0724212

2"40IS日

3.92OB26

163332J2

0.0461O04-2^0.0004O-11il9

R-SQuarecl

AdjustedR-squarecdlS.E.ofreoresslionSLimscjuoreclresidlLoo111h(□F-statistic

Prob(F-statistic>

O„61S958

OS81045

0.061509

O.121^852

S2.79260

64271

O.DDOOO1

MeandependentvarS.DdependentvarAKalKeinTocriterionSchwar-z.criterion

M^nin^n-Ouinn:

crirtierDurbin-Watson

O0-95029-2.637-453-2„4I333OO-2.S76OS6

1„2O4229

F与Obs两个的P值显示:

存在自相关

十八、Newey-West—致协方差估计

Dependentvariable:

UR

Method:

LeastSquares

Date:

09/07/15Time:

1635

Sample:

19782014

Includedobservations:

37

NeweyAVestHACStandardErrors&Covariance(lagtruncation=3)

Coefficient

StdLErrort-Statistic

Prob.

URIR

0.161922

0.0508133,186620

0.0030

C

-0.069449

0.109907-0.631837

0.5316

R-squared

0.379375

Meandependentvar

0.336145

AdjustedR-squared

0.361643

S.Ddependentvar

0.120626

S.E.ofregression

0.096377

Akaikeinfocriterion

-1.788557

Sumsquaredresid

0.325099

Schwarzcriterion

-1,701481

Loglikelihood

35.08831

Hannan-Quinncriter.

*1.757959

F-statistic

2139474

Durbin-Watsonstat

0.289676

Prob(F-statistic)

0.000049

十九、两阶段TSLS估计检验结果

DependentVariable:

URl^ethod:

Two-StageLeastSquares

Date:

09/07/15Time:

16:

43

Sample:

19782014

Indudedobservations:

37

InstrumentlistCUR

Coefficient

Std.Errort-Statistic

Prob.

URIR

0.426813

0.0922754.625445

0.0000

C

*0732965

0.232564-3.151675

0.0033

R-squared

-0.635916

Meandependentvar

0.336145

AdjustedR-squared

-0.682657

S.D.dependentvar

0.120626

S.E,ofregression

0.156473

Sumsquaredredid

0856934

F-statistic

2139474

Durbin-Watsonstat

0.632913

Prob(F-statistic)

0.000049

SecontTStageSSR

4.14E*30

二十、广义矩估计GMM检验结果

toependentVariable:

UR

Method:

GeneralizedMethodofMoments

Date:

09/07/15Time:

16:

51

Sample:

19782014

Includedobservations:

37

升级会员

升级会员