财务报告与分析三友会计名著译丛 第07章习题答案doc.docx

《财务报告与分析三友会计名著译丛 第07章习题答案doc.docx》由会员分享,可在线阅读,更多相关《财务报告与分析三友会计名著译丛 第07章习题答案doc.docx(14页珍藏版)》请在冰豆网上搜索。

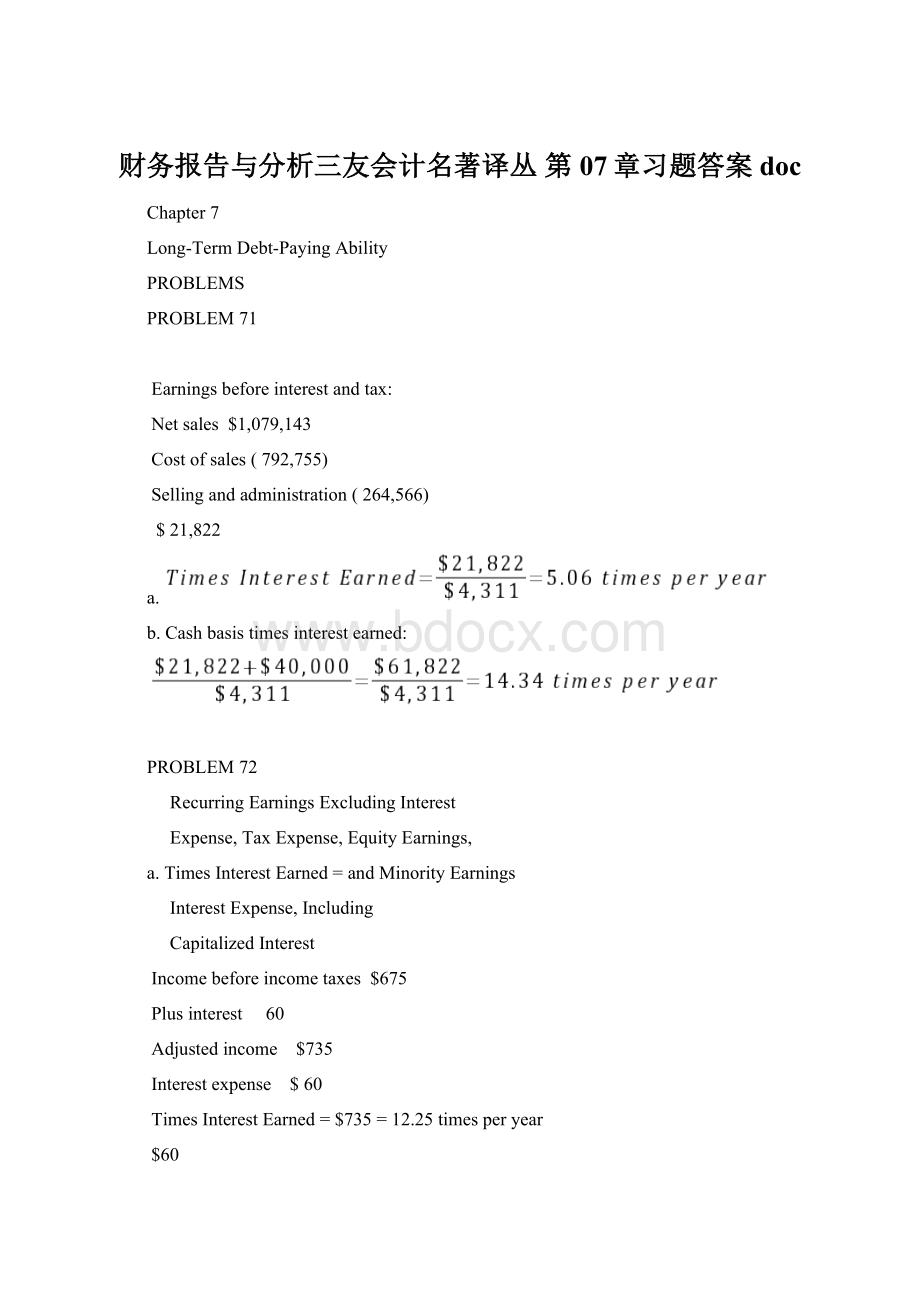

财务报告与分析三友会计名著译丛第07章习题答案doc

Chapter7

Long-TermDebt-PayingAbility

PROBLEMS

PROBLEM71

Earningsbeforeinterestandtax:

Netsales$1,079,143

Costofsales(792,755)

Sellingandadministration(264,566)

$21,822

a.

b.Cashbasistimesinterestearned:

PROBLEM72

RecurringEarningsExcludingInterest

Expense,TaxExpense,EquityEarnings,

a.TimesInterestEarned=andMinorityEarnings

InterestExpense,Including

CapitalizedInterest

Incomebeforeincometaxes$675

Plusinterest60

Adjustedincome$735

Interestexpense$60

TimesInterestEarned=$735=12.25timesperyear

$60

b.

Adjustedincomefrom(parta)$735

1/3ofoperatingleasepayments

(1/3x$150)50

Adjustedincome,includingrentals$785

Interestexpense$60

1/3ofoperatingleasepayments50

$110

FixedChargeCoverage=$785=7.14timesperyear

$110

PROBLEM73

RecurringEarnings,ExcludingInterest

Expense,TaxExpense,EquityEarning,

a.TimesInterestEarned=andMinorityEarnings________________

InterestExpense,Including

CapitalizedInterest

Incomebeforeincometaxesand

extraordinarycharges$36

Plusinterest16

(1)Adjustedincome52

(2)Interestexpense$16

TimesInterestEarned:

(1)dividedby

(2)=3.25timesperyear

RecurringEarnings,ExcludingInterest

Expense,TaxExpense,EquityEarnings,

andMinorityEarnings+InterestPortion

b.FixedChargeCoverage=OfRentals______________________________

InterestExpense,IncludingCapitalized

Interest+InterestPortionOfRentals

Adjustedincome(parta)$52

1/3ofoperatingleasepayments

(1/3x$60)20

(l)Adjustedincome,includingrentals$72

Interestexpense$16

1/3ofoperatingleasepayments20

(2)Adjustedinterestexpense$36

Fixedchargecoverage:

(1)dividedby

(2)=2.00timesperyear

PROBLEM74

a.DebtRatio=

b.Debt/EquityRatio=

c.RatioofTotalDebttoTangibleNetWorth=

TotalLiabilities=$174,979=$174,979=70.9%

TangibleNetWorth$249,222$2,324$246,898

d.KaufmanCompanyhasfinancedover41%ofitsassetsbytheuseoffundsfromoutsidecreditors.TheDebt/EquityRatioandtheDebttoTangibleNetWorthRatioareover70%.Whethertheseratiosarereasonabledependsuponthestabilityofearnings.

PROBLEM7-5

Ratio

Transaction

Times

Interest

Earned

Debt

Ratio

Debt/

Equity

TotalDebt/

Tangible

NetWorth

a.Purchaseofbuildingsfinancedbymortgage

b.Purchaseinventoryonshort-termloan

c.Declarationandpaymentofcashdividend

d.Declarationandpaymentofstockdividend

e.Firmincreasesprofitsbycuttingcostofsales

f.Appropriationofretainedearnings

g.Saleofcommonstock

h.Repaymentoflong-termbankloan

i.Conversionofbondstocommonstock

j.Saleofinventoryatgreaterthancost

-

-

0

0

+

0

0

+

+

+

+

+

+

0

-

0

-

-

-

-

+

+

+

0

-

0

-

-

-

-

+

+

+

0

-

0

-

-

-

-

PROBLEM76

a.TimesInterestEarned:

Timesinterestearnedrelatesearningsbeforeinterestexpense,tax,minorityearnings,andequityincometointerestexpense.Thehigherthisratio,thebettertheinterestcoverage.Thetimesinterestearnedhasimprovedmateriallyinstrengtheningthelongtermdebtposition.Consideringthatthedebtratioandthedebttotangiblenetworthhaveremainedfairlyconstant,theprobablereasonfortheimprovementisanincreaseinprofits.

Thetimesinterestearnedonlyindicatestheinterestcoverage.Itislimitedinthatitdoesnotconsiderotherpossiblefixedcharges,anditdoesnotindicatetheproportionofthefirmsresourcesthathavecomefromdebt.

DebtRatio:

Thedebtratiorelatesthetotalliabilitiestothetotalassets.

Thelowerthisratio,thelowertheproportionofassetsthathavebeenfinancedbycreditors.

ForArodexCompany,thisratiohasbeensteadyforthepastthreeyears.Thisratioindicatesthatabout40%ofthetotalassetshavebeenfinancedbycreditors.Formostfirms,a40%debtratiowouldbeconsideredtobereasonable.

Thedebtratioislimitedinthatitrelatesliabilitiestothebookvalueoftotalassets.Manyassetswouldhaveavaluegreaterthanbookvalue.Thistendstooverstatethedebtratioand,therefore,usuallyresultsinaconservativeratio.Thedebtratiodoesnotconsiderimmediateprofitabilityand,therefore,canbemisleadingastothefirm’sabilitytohandlelongtermdebt.

DebttoTangibleNetWorth:

Thedebttotangiblenetworthrelatestotalliabilitiestoshareholders'equitylessintangibleassets.Thelowerthisratio,thelowertheproportionoftangibleassetsthathasbeenfinancedbycreditors.

ArodexCompanyhashadastableratioofapproximately81%forthepastthreeyears.Thisindicatesthatcreditorshavefinanced81%asmuchastheshareholdersaftereliminatingintangiblesfromtheshareholderscontributionformostfirms,thiswouldbeconsideredtobereasonable.Thedebttotangiblenetworthratioismoreconservativethanthedebtratiobecauseoftheeliminationofintangibleitems.Itisalsoconservativeforthesamereasonthatthedebtratiowasconservative,inthatbookvalueisusedfortheassetsandmanyassetshaveavaluegreaterthanbookvalue.Thedebttotangiblenetworthratioalsodoesnotconsiderimmediateprofitabilityand,therefore,canbemisleadingastothefirm'sabilitytohandlelongtermdebt.

CollectiveinferencesonemaydrawfromtheratiosofArodex,Company:

OverallitappearsthatArodexCompanyhasareasonableandimprovinglongtermdebtposition.Thedebtratioandthedebttotangiblenetworthratiosindicatethattheproportionofdebtappearstobereasonable.Thetimesinterestearnedappearstobereasonableandimproving.

ThestabilityofearningsandcomparisonwithindustryratioswillbeimportantinreachingaconclusiononthelongtermdebtpositionofArodexCompany.

b.Ratiosarebasedonpastdata.Thefutureiswhatisimportant,anduncertaintiesofthefuturecannotbeaccuratelydeterminedbyratiosbaseduponpastdata.

Ratiosprovideonlyoneaspectofafirm'slong-termdebt-payingability.Otherinformation,suchasinformationaboutmanagementandproducts,isalsoimportant.

Acomparisonofthisfirm'sratioswithratiosofotherfirmsinthesameindustrywouldbehelpfulinordertodecideiftheratiosarereasonable.

PROBLEM77

RecurringEarnings,ExcludingInterest

a.1.TimesInterestExpense,TaxExpense,EquityEarnings,

Earned=andMinorityEarnings_________________

InterestExpense,Including

CapitalizedInterest

$162,000=8.1timesperyear

$20,000

2.DebtRatio=TotalLiabilities

TotalAssets

$193,000=32.2%

$600,000

3.Debt/EquityRatio=TotalLiabilities

Stockholders'Equity

$193,000=47.4%

$407,000

4.DebttoTangibleNetWorthRatio=TotalLiabilities

TangibleNetWorth

$193,000=49.9%

$407,000$20,000

b.Newassetstructureforallplans:

Assets

Currentassets$226,000

Property,plant,and

equipment554,000

Intangibles20,000

Totalassets$800,000

LiabilitiesandEquity

PlanA

CurrentLiabilities$93,000$200,000,000/100=

Longtermdebt100,0002,000,000shares

Preferredstock250,000

Commonequity357,000Nochangeinnetincome

$800,000

PlanB

Currentliabilities$93,000$200,000,000/10=

Longtermdebt100,00020,000,000shares

Preferredstock50,000

Commonstock120,000

Premiumoncommonstock300,000

Retainedearnings137,000Nochangeinnetincome

$800,000

PlanC

Currentliabilities$93,000OperatingIncome$162,000

Longtermdebt300,000Interestexpense52,000*

Preferredstock50,000110,000

Commonequity357,000Taxes(40%)44,000

$800,000NetIncome$66,000

*$20,000+16%($200,000)=$52,000

1.RecurringEarnings,ExcludingInterestExpense,

TimesInterestTaxExpense,EquityEarnings,andMinorityEarnings

Earned=InterestExpense,IncludingCapitalizedInterest

PlanAPlanBPlanC

2.Debt=TotalLiabilities

RatioTotalAssets

PlanAPlanBPlanC

3.Debt/EquityRatio=

PlanAPlanBPlanC

4.DebttoTangibleNetWorth=

PlanAPlanBPlanC

c.PreferredStockAlternative:

Advantages:

1.Lesserdropinearningspersharethanunderthecommonstockalternative.

2.Nottheabsolutereductioninearningsthataccompaniedthedebtalternative.

3.TherewouldbeanimprovementintheDebtRatio,Debt/EquityRatio,andTotalDebttoTangibleNetWorthRatio.

4.Doesnothavethereducedtimesinterestearnedthataccompaniedalternativeofissuinglongtermdebt.

Disadvantages:

1.Anincreaseinthefixedpreferreddividendchargethatthefirmmustpaybeforeanydividendscanbepaidtocommonstockholders.

CommonStockAlternative:

Advantages:

1.Noincreaseinfixedobligations.

2.TherewouldbeanimprovementintheDebtRatio,Debt/EquityRatio,andtheTotalDebttoTangibleNetWorthRatio.

3.Nottheabsolutereductioninearningsthataccompaniedthedebtalternative.

4.Doesnothavethereducedtimesinterestearnedthataccompaniedalternativeofissuinglongtermdebt.

Disadvantages:

1.Maximumdilutioninearningspershareofthethreealternatives.

Long-TermBondsAlternative:

Advantages:

1.Higherearningspersharethanwithcommonstock.

Disadvantages:

1.MaterialdeclineinTimesInterestEarned.

2.AmaterialincreaseintheDebtRatio,Debt/EquityRatio,

andTotalDebttoTangibleNetWorthRatio.

3.Absolutereductioninearnings.

4.Increaseintheinterestfixedchargethatmustbepaid.

d.The10%pre

升级会员

升级会员