会计学基础第三章答案.docx

《会计学基础第三章答案.docx》由会员分享,可在线阅读,更多相关《会计学基础第三章答案.docx(23页珍藏版)》请在冰豆网上搜索。

会计学基础第三章答案

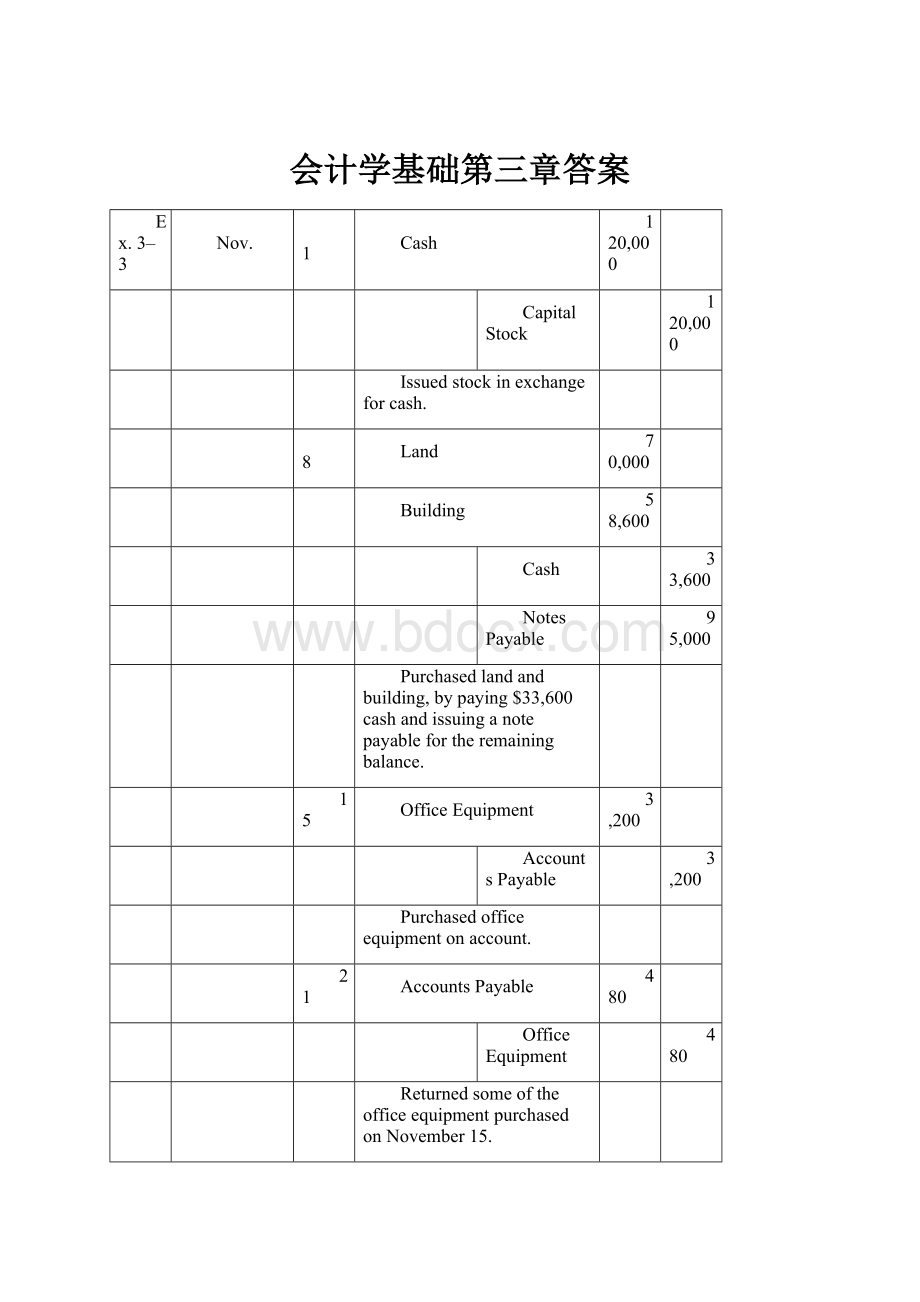

Ex.3–3

Nov.

1

Cash

120,000

CapitalStock

120,000

Issuedstockinexchangeforcash.

8

Land

70,000

Building

58,600

Cash

33,600

NotesPayable

95,000

Purchasedlandandbuilding,bypaying$33,600cashandissuinganotepayablefortheremainingbalance.

15

OfficeEquipment

3,200

AccountsPayable

3,200

Purchasedofficeequipmentonaccount.

21

AccountsPayable

480

OfficeEquipment

480

ReturnedsomeoftheofficeequipmentpurchasedonNovember15.

25

NotesPayable

12,000

Cash

12,000

Paidnotepayable.

30

Vehicles

9,400

Cash

1,400

NotesPayable

8,000

Purchasedvehiclesbypaying$1,400cashandissuinganotepayablefortheremainingbalance.

Ex.3–4

AVENSONINSURANCECompany

TrialBalance

November30,20__

Cash

$73,000

Land

70,000

Building

58,600

Officeequipment

2,720

Vehicles

9,400

Notespayable

$91,000

Accountspayable

2,720

Capitalstock

120,000

$213,720

$213,720

Ex.3–13

a.

July

18

Cash

1,500

CapitalStock

1,500

Issued500sharesofcapitalstocktoPatrickDoneganat$3pershare.

July

22

OfficeSupplies

100

AccountsPayable

100

Purchasedofficesuppliesonaccount.

July

23

MowingEquipment

2,000

Cash

400

NotesPayable

1,600

Purchasedmowingequipmentpaying$400cashandissuinga$1,600notepayableforthebalance.

July

24

FuelExpense

25

Cash

25

PaidforgasolinetobeusedinJuly.

July

25

AccountsReceivable

150

MowingRevenue

150

BilledLostCreekCemeteryformowingservices.PaymentisdueJuly30.

July

26

AccountsReceivable

200

MowingRevenue

200

BilledGolfViewCondominiumsformowingservices.

PaymentisdueAugust1.

July

30

Cash

150

AccountsReceivable

150

CollectedamountduefromLostCreekCemeteryformowingservicesprovidedJuly25.

July

31

SalariesExpense

80

Cash

80

PaidsalarytoTeddyGrimmforworkperformedinJuly.

30Minutes,Medium

Problem3–1

HEARTLANDCONSTRUCTION

b.

Transaction

Assets

=

Liabilities

+

Owners’Equity

Feb.1

+$500,000(Cash)

$0

+$500,000(Capital

Stock)

Feb.10

+$100,000(Land)

+$240,000(NotesPayable)

$0

+$200,000(OfficeBuilding)

–$60,000(Cash)

Feb.16

+$12,000(ComputerSystems)

$0

$0

–$12,000(Cash)

Feb.18

+$9,000(OfficeFurnishings)

+$8,000(AccountsPayable)

$0

–$1,000(Cash)

Feb.22

+$300(OfficeSupplies)

$0

$0

–$300(Cash)

Feb.23

+$36(AccountsReceivable)

$0

$0

–$36(ComputerSystems)

Feb.27

–$4,000(Cash)

-$4,000(AccountsPayable)

$0

Feb.28

+$36(Cash)

$0

$0

–$36(AccountsReceivable)

30Minutes,Medium

Problem3–2

ENVIRONMENTALSERVICES,INC.

a.

(1)

(a)

TheassetAccountsReceivablewasincreased.Increasesinassetsarerecordedbydebits.DebitAccountsReceivable,$2,500.

(b)

Revenuehasbeenearned.Revenueincreasesowners’equity.Increasesinowners’equityarerecordedbycredits.CreditTestingServiceRevenue,$2,500.

(2)

(a)

TheassetTestingSupplieswasincreased.Increasesinassetsarerecordedbydebits.DebitTestingSupplies,$3,800.

(b)

TheassetCashwasdecreased.Decreasesinassetsarerecordedbycredits.CreditCash,$800.

(c)

TheliabilityAccountsPayablewasincreased.Increasesinliabilitiesarerecordedbycredits.CreditAccountsPayable,$3,000.

(3)

(a)

TheliabilityAccountsPayablewasdecreased.Decreasesinliabilitiesarerecordedbydebits.DebitAccountsPayable,$100.

(b)

TheassetTestingSupplieswasdecreased.Decreasesinassetsarerecordedbycredits.CreditTestingSupplies,$100.

(4)

(a)

TheassetCashwasincreased.Increasesinassetsarerecordedbydebits.DebitCash,$20,000.

(b)

Theowners’equityaccountCapitalStockwasincreased.Increasesinowners’equityarerecordedbycredits.CreditCapitalStock,$20,000.

(5)

(a)

TheassetCashwasincreased.Increasesinassetsarerecordedbydebits.DebitCash,$600.

(b)

TheassetAccountsReceivablewasdecreased.Decreasesinassetsarerecordedbycredits.CreditAccountsReceivable,$600.

(6)

(a)

TheliabilityAccountsPayablewasdecreased.Decreasesinliabilitiesarerecordedbydebits.DebitAccountsPayable,$2,900($3,800-$800-$100).

(b)

TheassetCashwasdecreased.Decreasesinassetsarerecordedbycredits.CreditCash,$2,900.

(7)

(a)

TheDividendsaccountwasincreased.Dividendsdecreasetheowners’equityaccountRetainedEarnings.Decreasesinowners’equityarerecordedbydebits.DebitDividends,$6,800.

(b)

TheassetCashwasdecreased.Decreasesinassetsarerecordedbycredits.CreditCash,$6,800.

Problem3–2

ENVIRONMENTALSERVICES,INC.(continued)

Problem3–2

ENVIRONMENTALSERVICES,INC.(concluded)

c.

Therealizationprinciplerequiresthatrevenueberecordedwhenitisearned,evenifcashforthegoodsorservicesprovidedhasnotbeenreceived.

d.

Thematchingprinciplerequiresthatrevenueearnedduringanaccountingperiodbematched(offset)withexpensesincurredingeneratingthisrevenue.Testingsuppliesarerecordedasanassetwhentheyarefirstpurchased.Asthesesuppliesareusedinaparticularaccountingperiod,theircostwillbematchedagainsttherevenueearnedinthatperiod.

35Minutes,Medium

Problem3–3

WEIDASURVEYING,INC.

a.

IncomeStatement

BalanceSheet

Transaction

Revenue

Expenses

=

NetIncome

Assets

=

Liabilities

+

Owners’

Equity

Sept.1

NE

I

D

D

NE

D

Sept.3

I

NE

I

I

NE

I

Sept.9

I

NE

I

I

NE

I

Sept.14

NE

I

D

NE

I

D

Sept.25

NE

NE

NE

NE

NE

NE

Sept.26

I

NE

I

I

NE

I

Sept.29

NE

NE

NE

D

D

NE

Sept.30

NE

NE

NE

D

NE

D

Problem3–3

WEIDASURVEYING,INC.(concluded)

c.

Threesituationsinwhichacashpaymentdoesnotinvolveanexpenseinclude:

(1)thepaymentofacashdividend,

(2)thepaymentofaliabilityforapreviouslyrecordedexpense,and(3)thepurchaseofanasset,includingexpensespaidinadvancesuchasinsurance,rent,andadvertising.

50Minutes,Strong

Problem3–4

AERIALVIEWS

a.

IncomeStatement

BalanceSheet

Transaction

Revenue

Expenses

=

NetIncome

Assets

=

Liabilities

+

Owners’

Equity

June1

NE

NE

NE

I

NE

I

June2

NE

NE

NE

I

I

NE

June4

NE

I

D

D

NE

D

June15

I

NE

I

I

NE

I

June15

NE

I

D

D

NE

D

June18

NE

I

D

D

NE

D

June25

NE

NE

NE

NE

NE

NE

June30

I

NE

I

I

NE

I

June30

NE

I

D

D

NE

D

June30

NE

I

D

NE

I

D

June30

NE

NE

NE

NE

I

D

Problem3–4

AERIALVIEWS(continued)

Problem3–4

AERIALVIEWS(continued)

Problem3–4

AERIALVIEWS(continued)

Problem3–4

AERIALVIEWS(continued)

Problem3–4

AERIALVIEWS(continued)

Problem3–4

AERIALVIEWS(concluded)

60Minutes,Strong

Problem3–5

DR.SCHEKTER,DVM

a.

IncomeStatement

BalanceSheet

Transaction

Revenue

Expenses

=

NetIncome

Assets

=

Liabilities

+

Owners’

Equity

May1

NE

NE

NE

I

NE

I

May4

NE

NE

NE

I

I

NE

May9

NE

NE

NE

NE

NE

NE

May16

NE

NE

NE

I

I

NE

May21

NE

NE

NE

NE

NE

NE

May24

I

NE

I

I

NE

I

May27

NE

I

D

NE

I

D

May28

NE

NE

NE

NE

NE

NE

May31

NE

I

D

D

NE

D

Problem3–5

DR.SCHEKTER,DVM(continued)

Problem3–5

DR.SCHEKTER,DVM(continued)

c.

Cash

NotesPayable

May1

400,000

May4

100,000

May4

150,000

May24

1,900

May9

130,000

May28

100

May16

20,000

May31Bal.

150,000

May21

5,000

May31

2,800

May31Bal.

144,200

AccountsReceivable

AccountsPayable

May24

300

May28

100

May16

30,000

May27

400

May31Bal.

200

May31Bal.

30,400

OfficeSupplies

CapitalStock

May21

5,000

May1

400,000

May31Bal.

5,000

May31Bal.

400,000

MedicalInstruments

VeterinaryServiceRevenue

May9

130,000

May24

2,200

May31Bal.

130,000

May31Bal.

2,200

OfficeFixtures&Equipment

AdvertisingExpense

May16

50,000

May27

400

May31Bal.

50,000

May31Bal.

400

Land

SalaryExpense

May4

70,000

May31

2,800

May31Bal.

70,000

May31Bal.

2,800

升级会员

升级会员