ch05.docx

《ch05.docx》由会员分享,可在线阅读,更多相关《ch05.docx(103页珍藏版)》请在冰豆网上搜索。

ch05

CHAPTER5

ExaminingtheBalanceSheetand

StatementofCashFlows

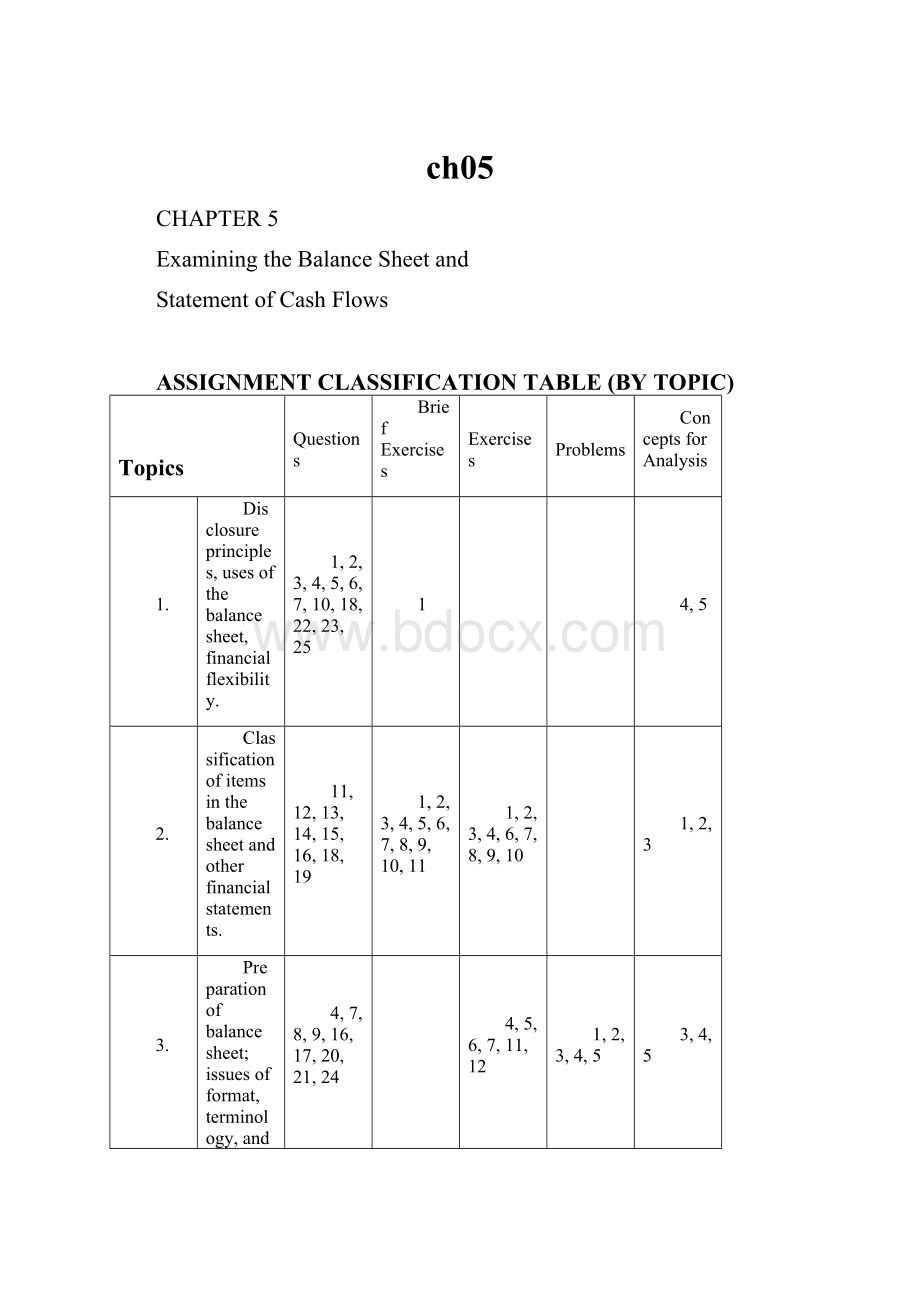

ASSIGNMENTCLASSIFICATIONTABLE(BYTOPIC)

Topics

Questions

BriefExercises

Exercises

Problems

ConceptsforAnalysis

1.

Disclosureprinciples,usesofthebalancesheet,financialflexibility.

1,2,3,4,5,6,7,10,18,22,23,25

1

4,5

2.

Classificationofitemsinthebalancesheetandotherfinancialstatements.

11,12,13,14,15,16,18,19

1,2,3,4,5,6,7,8,9,10,11

1,2,3,4,6,7,8,9,10

1,2,3

3.

Preparationofbalancesheet;issuesofformat,terminology,andvaluation.

4,7,8,9,16,17,20,21,24

4,5,6,7,11,12

1,2,3,4,5

3,4,5

4.

Statementofcashflows.

25,26,27,28,29,30,31,32

12,13,14,15,16

13,14,15,16,17,18

6,7

6

ASSIGNMENTCLASSIFICATIONTABLE(BYLEARNINGOBJECTIVE)

LearningObjectives

BriefExercises

Exercises

Problems

1.Explaintheusesandlimitations

ofabalancesheet.

7

2.Identifythemajorclassifications

ofthebalancesheet.

1,2,3,4,

6,8,9

3.Prepareaclassifiedbalancesheetusing

thereportandaccountformats.

1,2,3,4,5,6,7,8,9,

10,11

1,2,3,4,5,

6,7,9,10,

11,12,17

1,2,3,4,

5,6,7

4.Determinewhichbalancesheetinformationrequiressupplementaldisclosure.

10

4

5.Describethemajordisclosuretechniques

forthebalancesheet.

6.Indicatethepurposeofthestatement

ofcashflows.

7.Identifythecontentofthestatement

ofcashflows.

13

8.Prepareastatementofcashflows.

12,13,14,15

14,15,16,

17,18

6,7

9.Understandtheusefulnessofthestatement

ofcashflows.

16

15,16,18

6,7

ASSIGNMENTCHARACTERISTICSTABLE

Item

Description

LevelofDifficulty

Time

(minutes)

E5-1

Balancesheetclassifications.

Simple

15–20

E5-2

Classificationofbalancesheetaccounts.

Simple

15–20

E5-3

Classificationofbalancesheetaccounts.

Simple

15–20

E5-4

Preparationofaclassifiedbalancesheet.

Simple

30–35

E5-5

Preparationofacorrectedbalancesheet.

Simple

30–35

E5-6

Correctionsofabalancesheet.

Complex

30–35

E5-7

Currentassetssectionofthebalancesheet.

Moderate

15–20

E5-8

Currentvs.long-termliabilities.

Moderate

10–15

E5-9

Currentassetsandcurrentliabilities.

Complex

30–35

E5-10

Currentliabilities.

Moderate

15–20

E5-11

Balancesheetpreparation.

Moderate

25–30

E5-12

Preparationofabalancesheet.

Moderate

30–35

E5-13

Statementofcashflows—classifications.

Moderate

15–20

E5-14

Preparationofastatementofcashflows.

Moderate

25–35

E5-15

Preparationofastatementofcashflows.

Moderate

25–35

E5-16

Preparationofastatementofcashflows.

Moderate

25–35

E5-17

Preparationofastatementofcashflowsandabalancesheet.

Moderate

30–35

E5-18

Preparationofastatementofcashflows,analysis.

Moderate

25–35

P5-1

Preparationofaclassifiedbalancesheet,periodicinventory.

Moderate

30–35

P5-2

Balancesheetpreparation.

Moderate

35–40

P5-3

Balancesheetadjustmentandpreparation.

Moderate

40–45

P5-4

Preparationofacorrectedbalancesheet.

Complex

40–45

P5-5

Balancesheetadjustmentandpreparation.

Complex

40–50

P5-6

Preparationofastatementofcashflowsand

abalancesheet.

Complex

35–45

P5-7

Preparationofastatementofcashflowsand

abalancesheet.

Complex

40–50

CA5-1

Reportingforfinancialeffectsofvariedtransactions.

Moderate

25–30

CA5-2

Currentassetandliabilityclassification.

Moderate

30–35

CA5-3

Identifyingbalancesheetdeficiencies.

Moderate

20–25

CA5-4

Critiqueofbalancesheetformatandcontent.

Simple

25–30

CA5-5

Presentationofproperty,plant,andequipment.

Simple

20–25

CA5-6

Cashflowanalysis.

Complex

40–50

ANSWERSTOQUESTIONS

1.Thebalancesheetprovidesinformationaboutthenatureandamountsofinvestmentsinenterpriseresources,obligationstoenterprisecreditors,andtheowners’equityinnetenterpriseresources.Thatinformationnotonlycomplementsinformationaboutthecomponentsofincome,butalsocontributestofinancialreportingbyprovidingabasisfor

(1)computingratesofreturn,

(2)evaluatingthecapitalstructureoftheenterprise,and(3)assessingtheliquidityandfinancialflexibilityoftheenterprise.

2.Solvencyreferstotheabilityofanenterprisetopayitsdebtsastheymature.Forexample,whenacompanycarriesahighleveloflong-termdebtrelativetoassets,ithaslowersolvency.Informationonlong-termobligations,suchaslong-termdebtandnotespayable,incomparisontototalassetscanbeusedtoassessresourcesthatwillbeneededtomeetthesefixedobligations(suchasinterestandprincipalpayments).

3.Financialflexibilityistheabilityofanenterprisetotakeeffectiveactionstoaltertheamountsandtimingofcashflowssoitcanrespondtounexpectedneedsandopportunities.Anenterprisewithahighdegreeoffinancialflexibilityisbetterabletosurvivebadtimes,torecoverfromunexpectedsetbacks,andtotakeadvantageofprofitableandunexpectedinvestmentopportunities.Generally,thegreaterthefinancialflexibility,thelowertheriskofenterprisefailure.

4.Somesituationsinwhichestimatesaffectamountsreportedinthebalancesheetinclude:

a)allowancefordoubtfulaccounts.

b)depreciablelivesandestimatedsalvagevaluesforplantandequipment.

c)warrantyreturns.

d)determiningtheamountofrevenuesthatshouldberecordedasunearned.

Whenestimatesarerequired,thereissubjectivityindeterminingtheamounts.Suchsubjectivitycanimpacttheusefulnessoftheinformationbyreducingthereliabilityofthemeasures,eitherbecauseofbiasorlackofverifiability.

5.Anincreaseininventoriesincreasescurrentassets,whichisinthenumeratorofthecurrentratio.Therefore,inventoryincreaseswillincreasethecurrentratio.Ingeneral,anincreaseinthecurrentratioindicatesacompanyhasbetterliquidity,sincetherearemorecurrentassetsrelativetocurrentliabilities.

Notetoinstructors—Wheninventoriesincreasefasterthansales,thismaynotbeagoodsignalaboutliquidity.Thatis,inventorycanonlybeusedtomeetcurrentobligationswhenitissold(andconvertedtocash).Thatiswhysomeanalystsusealiquidityratio—theacidtestratio—thatexcludesinventoriesfromcurrentassetsinthenumerator.

6.Liquiditydescribestheamountoftimethatisexpectedtoelapseuntilanassetisconvertedintocashoruntilaliabilityhastobepaid.Therankingoftheassetsgiveninorderofliquidityis:

(1)(d)Short-terminvestments.

(2)(e)Accountsreceivable.

(3)(b)Inventories.

(4)(c)Buildings.

(5)(a)Goodwill.

7.Themajorlimitationsofthebalancesheetare:

(1)Thevaluesstatedaregenerallyhistoricalandnotatfairvalue.

(2)Estimateshavetobeusedinmanyinstances,suchasinthedeterminationofcollectibilityofreceivablesorfindingtheapproximateusefullifeoflong-termtangibleandintangibleassets.

(3)Manyitems,eventhoughtheyhavefinancialvaluetothebusiness,presentlyarenotrecorded.Oneexampleisthevalueofacompany’shumanresources.

QuestionsChapter5(Continued)

8.SomeitemsofvaluetotechnologycompaniessuchasIntelorIBMarethevalueofresearchanddevelopment(newproductsthatarebeingdevelopedbutwhicharenotyetmarketable),thevalueofthe“intellectualcapital”ofitsworkforce(theabilityofthecompanies’employeestocomeupwithnewideasandproductsinthefastchangingtechnologyindustry),andthevalueofthecompanyreputationornamebrand(e.g.,the“IntelInside”logo).Inmostcases,thereasonswhythevalueoftheseitemsarenotrecordedinthebalancesheetconcernthelackofreliabilityoftheestimatesofthefuturecashflowsthatwillbegeneratedbythese“assets”(forallthreetypes)andtheabilitytocontroltheuseoftheasset(inthecaseofemployees).Beingabletoreliablymeasuretheexpectedfuturebenefitsandtocontroltheuseofanitemareessentialelementsofthedefinitionofanasset,accordingtotheConceptualFramework.

9.Classificationinfinancialstatementshelpsusersbygroupingitemswithsimilarcharacteristicsandseparatingitemswithdifferentcharacteristics.Currentassetsareexpectedtobeconvertedtocashwithinoneyearoroneoperatingcycle,whicheverislonger—property,plantandequipmentwillprovidecashinflowsoveralongerperiodoftime.Thus,separatinglong-termassetsfromcurrentassetsfacilitatescomputationofusefulratiossuchasthecurrentratio.

10.Separateamountsshouldbereportedforaccountsreceivableandnotesreceivable.Theamountsshouldbereportedgross,andanamountfortheallowancefordoubtfulaccountsshouldbededucted.Theamountandnatureofanynontradereceivables,andanyamountsdesignatedorpledgedascollateral,shouldbeclearlyidentified.

11.Available-for-salesecuritiesshouldbereportedasacurrentassetonlyifmanagementexpectstoconvertthemintocashasneededwithinoneyearortheoperatingcycle,whicheverislonger.Ifavailable-for-salesecuritiesarenotheldwiththisexpectation,theyshouldbereportedaslong-terminvestments.

12.Therelationshipbetweencurrentassetsandcurrentliabilitiesisthatcurrentliabilitiesarethoseobligationsthatarereasonablyexpectedtobeliquidatedeitherthroughtheuseofcurrentassetsorthecreationofothercurrentliabilities.

13.Thetotalsellingpriceoftheseasonticketsis$20,000,000(10,000X$2,000).Ofthisamount,$9,000,000hasbeenearnedby12/31/07

升级会员

升级会员