会计专业英语教案一Word文档格式.docx

《会计专业英语教案一Word文档格式.docx》由会员分享,可在线阅读,更多相关《会计专业英语教案一Word文档格式.docx(18页珍藏版)》请在冰豆网上搜索。

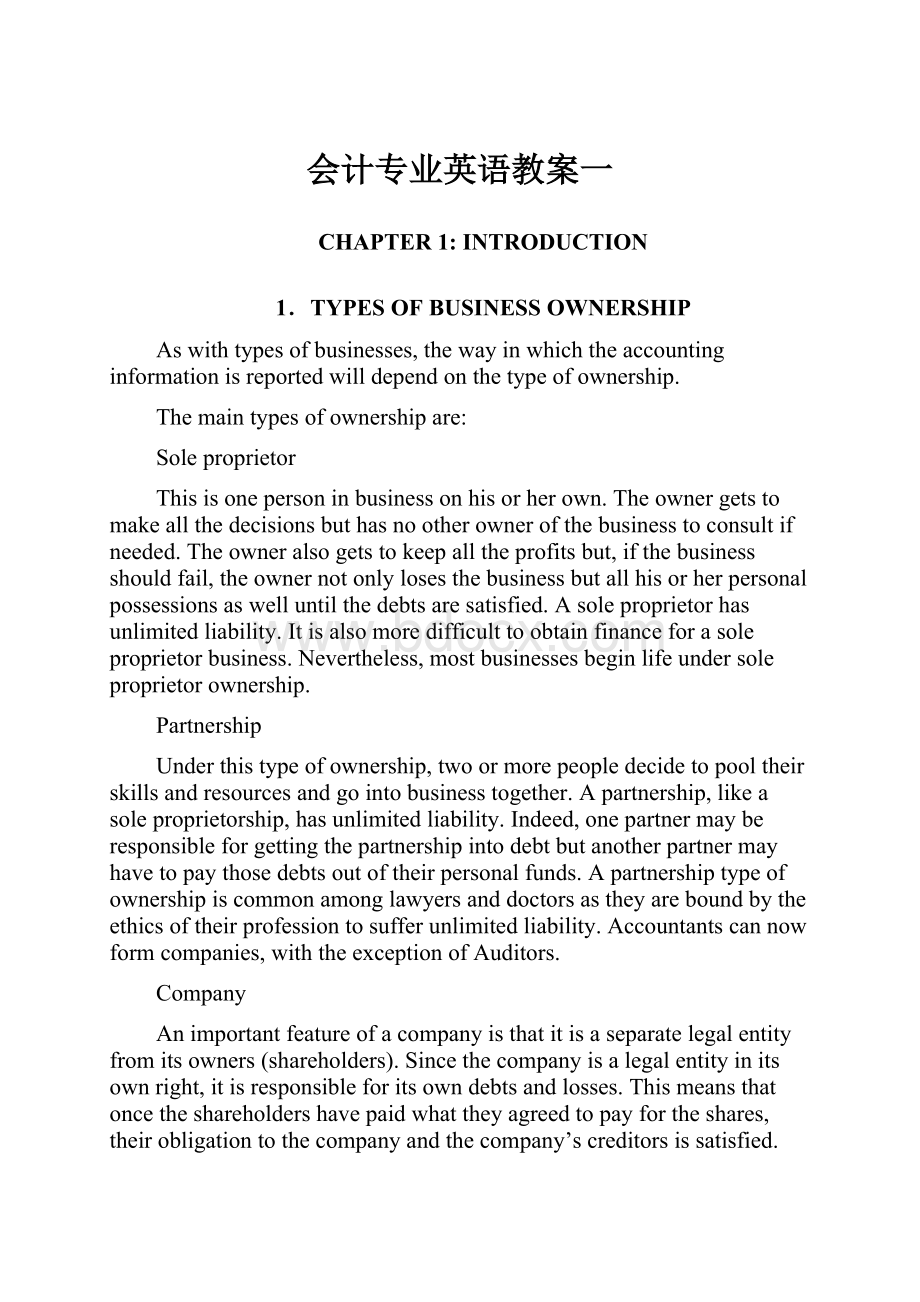

DurationExpiresbyowner’sExpiresbychoicePerpetual

ofLifechoiceordeathoforwithdrawalofsuccession

ownerpartner

TransferabilityIfproprietorsellsPartnershipshareUsually

ofOwnershiphisinterest,thecannotbesoldtransferable

Interestsbusinessiswithoutagreement

reconstitutedofotherpartners:

undernewnewpartnership

ownershipformed

SourcesofOwner’sfundsandPartners’fundsShares,

Financeloansandloansdebentures,

loans

ProfitAllaccruetoSharedaccordingDividends

Sharingownertopartnershipdeclaredby

agreementordirectors

PartnershipAct1908

OwnershipOneownerTwoormoreOneormore

CapitalProvidedbyPartnerscontributeDividedinto

owneraccordingtoshares

partnershipagreement

LiabilityforUnlimitedUnlimitedLimitedto

firm’sdebtstheamount

outstandingon

sharecapital

ManagementOwnerEachpartnerAppointedbyshareholders

2.UsersofFinancialInformation

InternalUsers

⏹Managerswhoplan,organizeandrunabusiness

⏹Marketingmanagers

⏹Productionsupervisors

⏹Financedirectors

⏹Companyofficers

External

⏹Investors

⏹Creditors

⏹Others

⏹Regulatoryagencies

⏹Taxauthorities

⏹Customers

⏹LaborUnions

⏹Economicplanners

3.TypesofBusinessActivity

FinancingActivities

⏹Borrowingcreatesliabilities

⏹Bankloans

⏹Debtsecurities

⏹Goodsoncreditorpayables

⏹Sellingstockcreatesstockholders’equity

InvestingActivities

⏹Obtainingresourcesorassetstooperatethebusiness

⏹Land

⏹Buildings

⏹Vehicles

⏹Computers

⏹Furniture

⏹Equipment

OperatingActivities

⏹Primaryactivityofbusiness

Sellinggoods

Providingservices

Manufacturing

CostofSales

Advertising

Payingemployees

Payingutilities

Revenuesaretheincreasesinassetsresultingfromthesaleofaproductorservice

Expensesarethecostofassetsconsumedorservicesusedingeneratingrevenue.

Ifrevenue>

expense=NetIncome

Ifrevenue<

expense=NetLoss!

4.ContentandPurposeofFinancialStatements

⏹Accountantscommunicatewithusersthroughfourfinancialstatements

TheObjectiveofFinancialStatements

⏹Theobjectiveoffinancialstatementsistoprovideinformationaboutthefinancialposition,performanceandchangesinfinancialpositionofanenterprisethatisusefultoawiderangeofusersinmakingeconomicdecisions.

FourFinancialStatements

⏹IncomeStatement

⏹RetainedEarningsStatement

⏹BalanceSheet

⏹StatementofCashFlows

THEINCOMESTATEMENT

PURPOSEOFTHEINCOMESTATEMENT

ThepurposeoftheIncomeStatementistoreporttheresultsofthebusinessoperationsforagivenperiodoftime,calledtheAccountingPeriod.

ItmeasuresProfit(orLoss)fortheperiodbydeductingExpensesfromIncome,usingtheformula

INCOME–EXPENSES=PROFIT(LOSS)FORTHEPERIOD

USESOFTHEINCOMESTATEMENT

∙Managersallocateresourcesbasedontheperformanceofthebusiness

∙Itcanbeusedtodiscoverifthebusinessismaintaininganadequatemarginonsales

∙TheInlandRevenueDepartment(IRD)usesittoassesstaxationliability

∙Unionsmayexamineitaspartofsalarydiscussions

∙Investorsareinterestedinjudgingtheperformanceofthebusinesstoassessthemanagementperformance,andtojudgebothfuturebusinesssuccessandreturnoninvestment

∙Itcanbesubmittedtobanksinsupportofaloanapplication,toassistbankstojudgeincomepotential(torepaytheloan!

)

∙Externalusers,inparticular,canassess

oInvestmentvalue(isthereagoodreturnonassets?

oCreditworthiness(isthebusinessearningenoughtopaysuppliers?

oAbilitytoearnincome

∙Overallitisusefulinevaluatingthepastperformanceofthebusiness

CLASSIFYINGTHEINCOMESTATEMENT

Incomecanbeclassifiedas

a)Revenue(or,foratradingorganisation,TradingRevenue)and

b)OtherIncome

Revenueisallrevenueincludedindeterminingtheoperatingprofitoftheperiod,andisthemainsourceofrevenueforthefirm.Forexample,foratradingbusinessthiswilbethesaleofgoods.

OtherIncomeissupplementaryrevenues,notfromthemainactivitiesofthefirm,\.Forexamplerentingoutsomesparewarehousespace.

Expensescanbeclassifiedas

a)TradingExpenses

b)SellingandDistributionExpenses

c)AdministrativeExpenses

d)FinancialExpenses

e)OtherExpenses

Expensesmaybefurtherclassifiedintovariousgroupsthatsuitaparticularbusiness.Eachgroupcontainstypesofexpensesthathaveasimilarnature.Acommonclassificationis:

a)TradingExpenses-thosethatrelatedirectlytobringingthegoodsintothebusinessforresale.

Forexamplecustomsduty,cartageinwards,packaging.

b)Sellinganddistributionexpenses–thoseexpensesincurredtoincreasethesalesofabusinessanddistributetheproducttothecustomers.

Forexamplesalessalariesandwages,advertising,salesvanexpenses,cartageoutwards.

c)Administrativeexpenses–thoseexpensesincurredinordertoorganiseabusiness.

Forexampleelectricity,rates,telephone,rent,officesalariesandwages,insurance,accountancyfees.

d)Financialexpenses–thoseexpensesincurredinfinancingthebusiness.

Forexamplebaddebts,interestonloan,interestonmortgage,discountallowed.

ExamplesofOtherExpensesarelossonsaleofproperty,donations

RetainedEarningsStatement(alsocalledchangesinequity)

⏹Showschangesinretainedearningsforperiod:

month,quarter,year

⏹Beginningbalance

⏹AddNetIncomefromincomestatement.

⏹DeductDividends

⏹Endingbalance

ForaSoleProprietor,TheCapital,orEquity,thatshowsontheTrialBalanceistheOPENINGCapital.TransactionsoccurduringthefinancialyearthatwillaffecttheEquity,causingittohaveincreasedordecreasedbytheendofthefinancialyear.ThechangefromOpeningtoClosingCapitalisusuallyshownwithintheEquitysectionatthebottomoftheBalanceSheet,asshowninthefollowingexampleforRichard’sRhubarbShop:

EXAMPLE:

AccountsPayable35,000

AccountsReceivable45,000

BankLoanLongTerm175,000

BankOverdraft21,000

Land(cost)195,000

Inventory213,000

Cashonhand2,000

SharesinotherCompanies8,000

Goodwill5,000

Capital(opening)238,800

Drawings10,200

OtherInformation:

Profitfortheyearended31March2016was$8,400

Required:

CompleteafullyclassifiedBalanceSheet

ANSWER:

Richard’sRhubarbShop

BalanceSheetasat31March2016

$$$

CurrentAssets

CashonHand2,000

AccountsReceivable45,000

Inventory213,000260,000

Non-CurrentAssets

Property,PlantandEquipment

Land195,000

Investments

Sharesinothercompanies8,000

Intangibles

Goodwill5,000208,000

TotalAssets468,000

CurrentLiabilities

BankOverdraft21,000

AccountsPayable35,00056,000

Non-CurrentLiabilities

BankLoan175,000

TotalLiabilities231,000

NETASSETS$237,000

EQUITY

Capital(opening)238,800

Plus:

Profitfortheperiod8,400

247,200

Less:

Drawings10,200

Capital(closing)$237,000

THEBALANCESHEET

THEPURPOSEOFTHEBALANCESHEET

ThepurposeoftheBalanceSheetistoshowthefinancialpositionofabusinessataparticularpointoftime.

Itreportstheassetsofthebusinessandhowtheseassetshavebeenfunded.Theassetscanbefundedbyliabilities(externalfunding)orowner’sequity(inter

升级会员

升级会员