Guide to Supply Chain Management7物流供应链管理指南7文档格式.docx

《Guide to Supply Chain Management7物流供应链管理指南7文档格式.docx》由会员分享,可在线阅读,更多相关《Guide to Supply Chain Management7物流供应链管理指南7文档格式.docx(35页珍藏版)》请在冰豆网上搜索。

lClarifywhysupplychaincompaniesareinbusiness

lRecognisetheimpactofsupplychainmanagementonthekeyfinancial

statements

lDemonstratehowsupplychainmanagementcanaddvalueandimprove

corporatefinancialperformance

9.1IntroductiontoSupplyChainFinance

9.1.1TheBusinessProcess

Supplychaincompaniesareusuallyinbusinesstogeneratecashandgiveareturnto

theirinvestors.Alsomakingaprofitisimportant,wecancalculateprofitbytaking

ourcostsfortheyearanddeductitfromthesalesfortheyear.However,whilst

companiesarestillabletocontinueoperatingwhenmakingnoprofitorhaving

lossesforseveralyears,theyimmediatelystopoperatingwhentheyrunoutofcash.

TheauthorsrecommendanexcellenttextonthissubjectwrittenbyTennent(2008),

whichguidespeoplethoughthemainfinancialprinciples,illustratestheirapplication

andfinallyprovidesatoolkitformanagingfinancialresponsibility.Inorderto

understandthedifferentfinancialparametersofacompany,thebusinessprocess

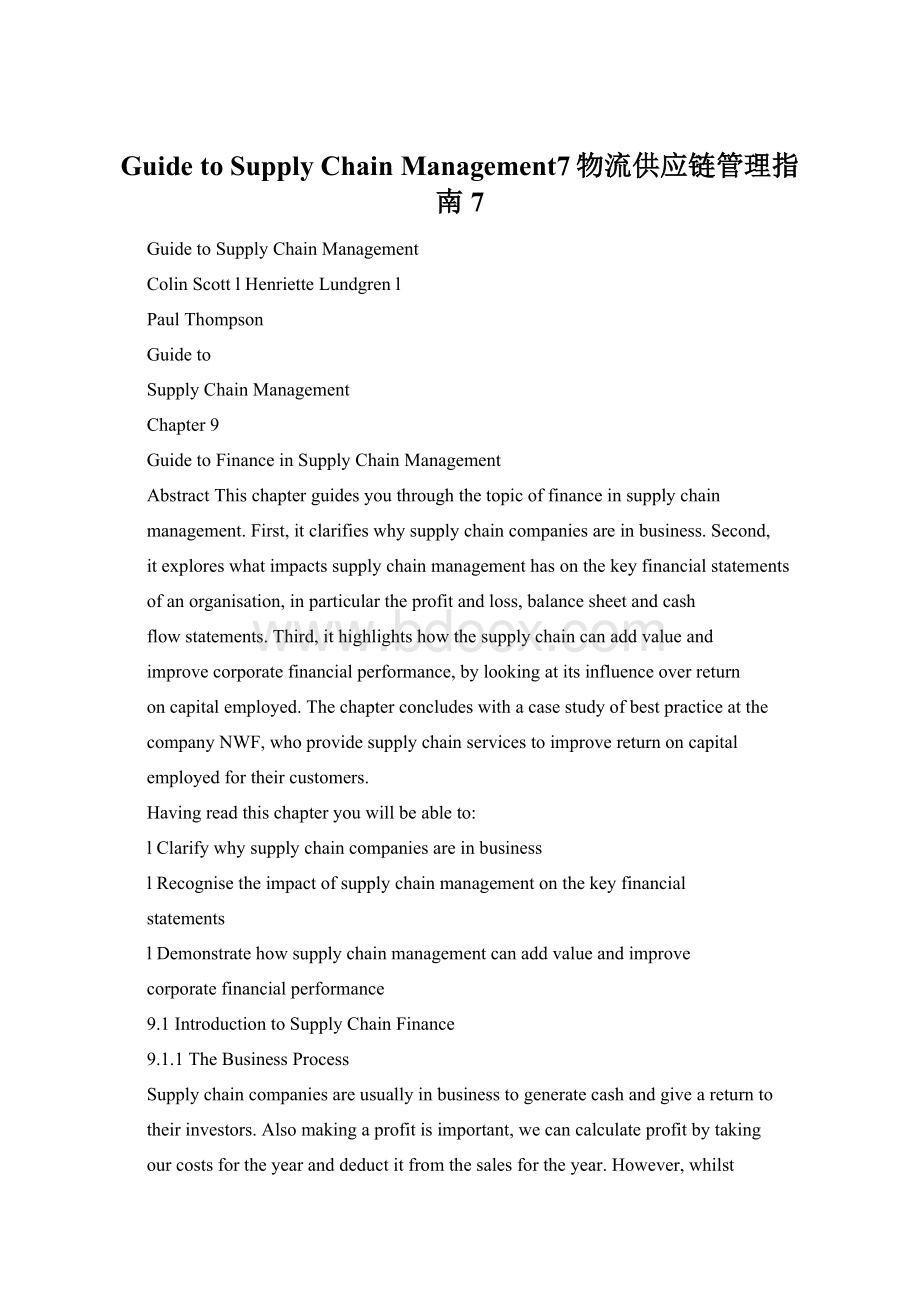

canbeillustrated(seeFig.9.1).

C.Scottetal.,GuidetoSupplyChainManagement,

DOI10.1007/978-3-642-17676-0_9,#Springer-VerlagBerlinHeidelberg2011

141

Let’sconsideranexampleandassumeyouwouldliketostartanewcompany

thatmanufacturesdrinks,similartoSchweppesortheCoca-ColaCompany.You

wouldneedsomeinitialcapitalinvestmentinordertobuyassets.Assetsare,for

example,thefactory,rawmaterialsorperhapstruckstodeliverthefinished

products.Theshareholdersandbanksontheleft,whichcanbeconsideredasthe

twosourcesofcapitalinvestment,providetheirinvestmentintheformofcash.This

isrepresentedbythearrowfromshareholdersandbankstoassetsinthecentreof

thediagram.

Oncetheassetshavebeenpurchased,yourcompanycanstartsellingthedrinks

product.Inordertodoso,employeesandsuppliersmustbepaidfortheirwork,

productsandservices.Thearrowfromassetstosalesandservicerepresentscash

flowoutofthebusinessastheemployeesandsuppliersarepaid.Thedrinks

productsarethensoldtocustomers,whopaythebusiness.Thisisdepictedbythe

toprightarrowascashreceivedfromcustomers.Ifthebusinesssellsthedrinks

formorethanthecostsinvolvedwithmanufactureanddistribution,aprofitis

made.Thisprofitisthensubjecttotaxpaidtothegovernment.Finally,fromthe

cashremaining,returnsarepaidbacktotheshareholdersandbanksthrough

interestanddividendsasindicatedbythearrowonthebottomleft.Anymonies

leftovercanberetainedandreinvestedinthebusinesstogenerate,forexample,

growth.Nowletusconsiderthreeareascriticaltosupplychainfinance:

gearing,

returnsandhurdlerates.

Assets

Sales&

service

Your

company

Shareholders

&

banks

Capitalinvestment

Returns

Employees

suppliers

Customers

Government

Fig.9.1Thebusinessprocess

1429GuidetoFinanceinSupplyChainManagement

9.1.2Gearing

Thetermgearinginbusinessfinanceidentifieshowmuchcapitalinvestmentinthe

companyisfundedbyinternalorexternalfunds.Itisthemeasureoffinancial

leverage,demonstratingthedegreetowhichafirm’sactivitiesarefundedby

owner’sfunds,e.g.shareholders,versuscreditor’sfunds,e.g.banks.Capitalthat

islentbybanksisreferredtoasdebtandcapitalthatisinvestedbytheshareholders

isreferredtoasequity.Gearingisameasureandisexpressedas:

Gearing.Debtasapercentageoftotalfunds(debt+equity).

Inmanybusinesses,30–50%ofdebtisseenasanidealrangeofgearing.

Managersoftenaskwhybusinessesarenotsolelyfinancedbybankdebtalone.

Toanswerthisquestion,weneedtothinkaboutrisk.Banksfeelreluctanttotake

100%oftheriskaloneandthereforeprefertoengageincapitalinvestmentswherea

substantialpartisgivenbyshareholders.

9.1.3Returns

Let’sreturntoourdrinkscompanyexample.Inordertostartadrinkscompany,the

bankswillinjectsomeinvestment(say50%),andtheremainingcapitalwillhaveto

beobtainedfrominvestors(shareholders).Boththesepartieswillrequireareturn

fromthedrinksbusiness.Forexample,thebankswouldexpecta5%returnin

interestandshareholdersa10%return–thisseemslessfavourableforthebanks.If

thedrinkscompanygoesbankrupt,thebanksowntheassetsandtheshareholders

loseeverything.Bytakingmorerisktheshareholderscanreceivehigherdividends

(annualpayments)andcapitalgrowthofthesharestheyhaveinthebusiness.

9.1.4HurdleRates

Asyoualreadyknow,thereturnrateshavetwomaincomponents:

thecostofdebt

capitalandcostofequitycapital.ThisisreferredtoastheCostOfCapital(COC).

Mostcompaniesarefinancedbyacombinationofdebtandequitysotheyneedto

findabalancedcombinationofthesetwo.Forexample,50%ofthecompanymight

befinancedbydebtand50%byequity.Ifdebtrequiresa5%andequitya15%

returnthentheWeightedAverageCostofCapital(WACC)is10%.This10%

WACCisknownasthe“hurdlerate”.Thehurdleratecanbedescribedasthe

requiredreturnforaproject.Acompanyplanningtoinvestinanewfactory,for

example,needstomakesurethatthereturnoftheinvestmentisgreaterthanthe

WACCbeforetheinvestmentstartspayingofffinancially.Supplychainprojects

needtosatisfyatleastthereturnstothelenders,orthereisnobenefittothebusiness

andnofinancialreasonwhytheprojectshouldtakeplace.

9.1IntroductiontoSupplyChainFinance143

Managerswhoworkinthirdpartylogisticscompanieshavetheevenhardertask

ofjumpingtwohurdles.Notonlydotheirsolutionsneedtoyieldgreaterreturns

thantheircustomers’hurdlerate,theyalsoneedtosatisfytheirowncompany

hurdleratesbeforetheycangoaheadandimplementanysolution.

9.2HowCompaniesCascadeFinancialInformation

Companiescascadefinancialinformationusingthreefinancialstatements:

profit

andlossaccount,balancesheetandcashflowstatement(Stickneyetal.2009).The

profitandlossaccountisadetailedsummaryofthesalesrevenueforonefinancial

yearandtheassociatedcosts.Thebalancesheetsummariseshowthecompanyhas

beenfinanced.Thecashflowstatementshowsthecashinandthecashoutforthe

business,inagivenyear.Rememberfromthebusinessprocesscoveredearlierthat

thefourarrowsrepresentcash.

9.2.1ProfitandLoss

TheProfitandLoss(P&

L)accountissometimesreferredtoastheincomestatement,

anditessentiallycaptureshowmuchmoneygoesintoandoutofthe

company.Itusuallyconsistsoffourparts(seeFig.9.2).

Part1

RevenueX

Costofsales

Grossprofit

(Y)

Z

Part2

Operatingexpenses

Operatingprofit

Part3

Interest(Y)

Tax

Profitaftertax

Part4

Dividend

Retainedprofit

Fig.9.2Profitandlossaccount

1449GuidetoFinanceinSupplyChainManagement

Thefirstpartisatradingaccount,showingthetotalsalesrevenuelessthecosts

ofsalesandanychangesinthevalueofstockfromthelastaccountingperiod.This

givesthegrossprofit(orloss).Thesecondpartshowsanyotherincome(apartfrom

trading)andlistsadministrativeandothercoststoarriveatanoperatingprofit(or

loss).Fromthisoperatingprofittheappropriatecorporationtaxisdeductedtogive

thethirdpart,whichisthenetprofitaftertax.Inthefourthpart,dividends(returns

toshareholders)aresubtractedfromprofitaftertax;

thisresultsinretainedprofit.

SupplychainactivitiescanimpacttheP&

Lverysignificantlybyinfluencing

bothrevenueandcost.Itisusefulatthispointtoconsiderfourcriteriaagainstwhich

wecanillustratethisinfluence:

lQuality

lService

lCost

lTime

Shouldmanufacturingbesubstandardorthedistributionprocessesnotdeliverthe

requiredqualityofaproduct,saleswilldecrease.Ifweforecastinefficiently,itmight

resultinashortdeliverytoacustomer,sothattheservicelevelisaffected.Costcan

beconsideredfromacompetitiveperspectiveratherthantheabsolutenumber.Iftwo

productsareverysimilar,butoneismoreexpensivethantheothertoproduce

becauseitssupplychainislessefficient,salesrevenueislikelytobeless.Insome

ofthecompaniesinwhichtheauthorshaveworked,supplychaincostsmade

upbetween25and70%oftotalcosts.Examplesofsupplychaincostsare:

lRawmaterialpurchases

lSalaries

lFactoryconversioncosts

lDepreciationonsupplychainassets

lFacilityenergycosts

lInsuranceandutilitiesforfacilities

lFuelforvesselsandvehicles

lInventorystorageandinterest

升级会员

升级会员