会计英语资产负债表及利润表.doc

《会计英语资产负债表及利润表.doc》由会员分享,可在线阅读,更多相关《会计英语资产负债表及利润表.doc(13页珍藏版)》请在冰豆网上搜索。

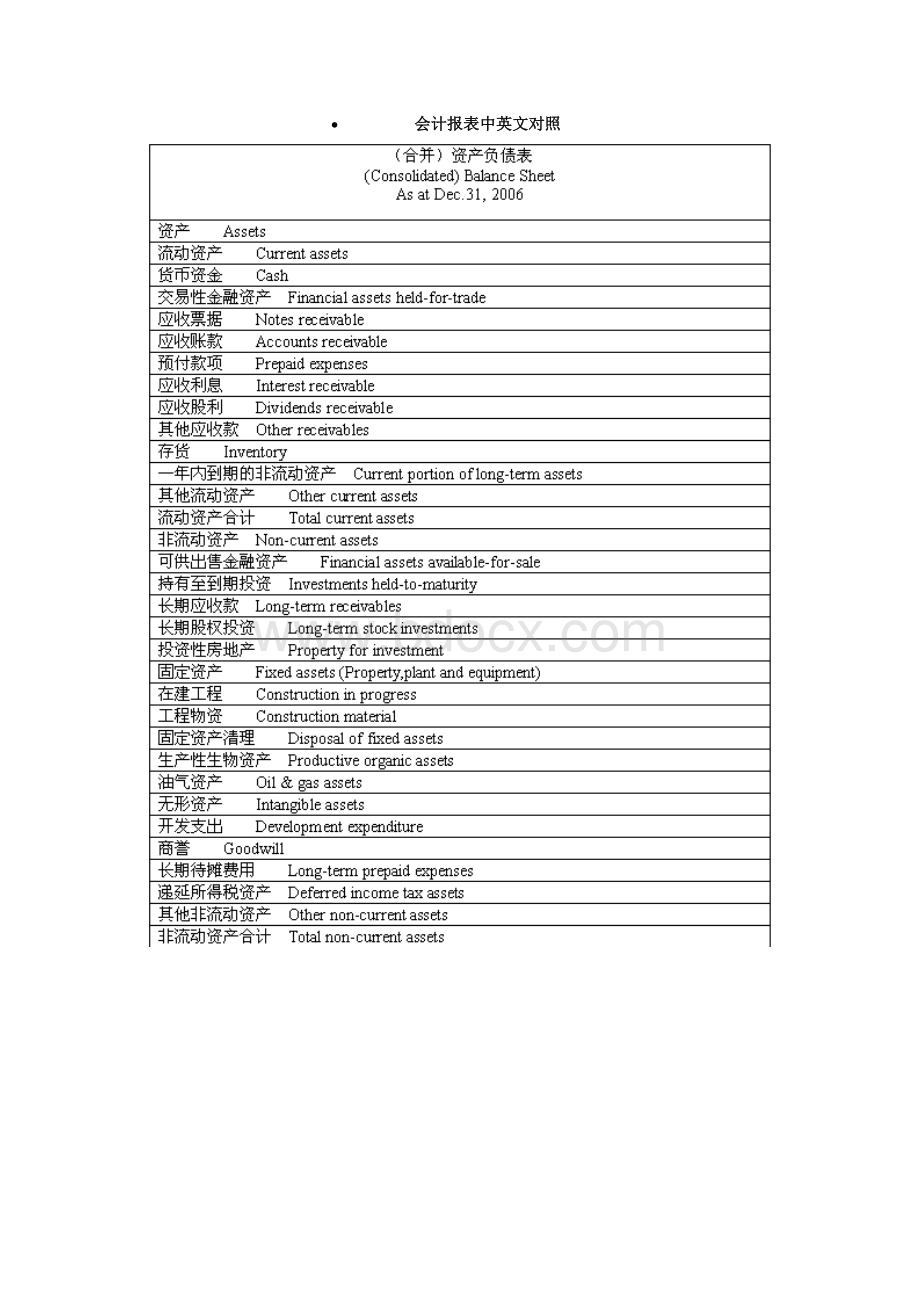

·会计报表中英文对照

Accounting

1.Financialreporting(财务报告)includesnotonlyfinancialstatementsbutalsoothermeansofcommunicatinginformationthatrelates,directlyorindirectly,totheinformationprovidedbyabusinessenterprise’saccountingsystem----thatis,informationaboutanenterprise’sresources,obligations,earnings,etc.

2.Objectivesoffinancialreporting:

财务报告的目标

Financialreportingshould:

(1)Provideinformationthathelpsinmakinginvestmentandcreditdecisions.

(2)Provideinformationthatenablesassessingfuturecashflows.

(3)Provideinformationthatenablesuserstolearnabouteconomicresources,claimsagainstthoseresources,andchangesinthem.

3.Basicaccountingassumptions基本会计假设

(1)Economicentityassumption会计主体假设

Thisassumptionsimplysaysthatthebusinessandtheownerofthebusinessaretwoseparatelegalandeconomicentities.Eachentityshouldaccountandreportitsownfinancialactivities.

(2)Goingconcernassumption持续经营假设

Thisassumptionstatesthattheenterprisewillcontinueinoperationlongenoughtocarryoutitsexistingobjectives.

Thisassumptionenablesaccountantstomakeestimatesaboutassetlivesandhowtransactionsmightbeamortizedovertime.

Thisassumptionenablesanaccountanttouseaccrualaccountingwhichrecordsaccrualanddeferralentriesasofeachbalancesheetdate.

(3)Timeperiodassumption会计分期假设

Thisassumptionassumesthattheeconomiclifeofabusinesscanbedividedintoartificialtimeperiods.

Themosttypicaltimesegment=CalendarYear

Nextmosttypicaltimesegment=FiscalYear

(4)Monetaryunitassumption货币计量假设

Thisassumptionstatesthatonlytransactiondatathatcanbeexpressedintermsofmoneybeincludedintheaccountingrecords,andtheunitofmeasureremainsrelativelyconstantovertimeintermsofpurchasingpower.

Inessence,thisassumptiondisregardstheeffectsofinflationordeflationintheeconomyinwhichtheentityoperates.

Thisassumptionprovidessupportforthe"HistoricalCost"principle.

4.Accrual-basisaccounting权责发生制会计

5.Qualitativecharacteristics会计信息质量特征

(1)Reliability可靠性

Foraccountinginformationtobereliable,itmustbedependableandtrustworthy.

Accountinginformationisreliabletotheextendthatitis:

Verifiable:

meansthatinformationhasbeenobjectivelydetermined,arrivedat,orcreated.Morethanonepersoncouldconsiderthefactsofasituationandreachasimilarconclusion.

Representationallyfaithful:

thatsomethingiswhatitisrepresentedtobe.Forexample,ifamachineislistedasafixedassetonthebalancesheet,thenthecompanycanprovethatthemachineexists,isownedbythecompany,isinworkingcondition,andiscurrentlybeingusedtosupporttherevenuegeneratingactivitiesofthecompany.

Neutral:

meansthatinformationispresentedinaccordancewithgenerallyacceptedaccountingprinciplesandpractices,andwithoutbias.

(2)Relevance相关性

Relevantinformationiscapableofmakingadifferenceinthedecisionsofusersbyhelpingthemtoevaluatethepotentialeffectsofpast,present,orfuturetransactionsorothereventsonfuturecashflows(predictivevalue)ortoconfirmorcorrecttheirpreviousevaluations(confirmatoryvalue).

(3)Understandability可理解性

Understandabilityisthequalityofinformationthatenablesuserswhohaveareasonableknowledgeofbusinessandeconomicactivitiesandfinancialreporting,andwhostudytheinformationwithreasonablediligence,tocomprehenditsmeaning.

(4)Comparability可比性

Comparability:

suggeststhataccountinginformationthathasbeenmeasuredandreportedinasimilarmannerbydifferententerprisesshouldbecapableofbeingcomparedbecauseeachoftheenterprisesisapplyingthesamegenerallyacceptedaccountingprinciplesandpractices.

Consistency:

suggeststhatanentityhasusedthesameaccountingprincipleorpracticefromoneperiodtoanother,therefore,ifthedollaramountreportedforacategoryisdifferentfromoneperiodtothenext,thenchancesarethatthedifferenceisduetoachangelikeanincreaseordecreaseinsalesvolumeratherthanbeingduetoachangeinthemethodofcalculatingthedollaramount.

(5)Substanceoverform实质重于形式

Substanceoverformemphasizestheeconomicsubstanceofaneventeventhoughitslegalformmayprovideadifferentresult.

Itrequiresthatbusinessenterpriseshouldperformaccountingrecognition,measurementandreportinginaccordancewiththeeconomicsubstanceratherthanthelegalformofaneventortransaction.

(6)Materiality重要性

Informationismaterialifitsomissionormisstatementcouldinfluencetheresourceallocationdecisionsthatusersmakeonthebasisofanentity’sfinancialreport.Materialitydependsonthenatureandamountoftheitemjudgedintheparticularcircumstancesofitsomissionormisstatement.Decidingwhenanamountismate

升级会员

升级会员