Intermediate AccountingChapter 4Word文档下载推荐.docx

《Intermediate AccountingChapter 4Word文档下载推荐.docx》由会员分享,可在线阅读,更多相关《Intermediate AccountingChapter 4Word文档下载推荐.docx(25页珍藏版)》请在冰豆网上搜索。

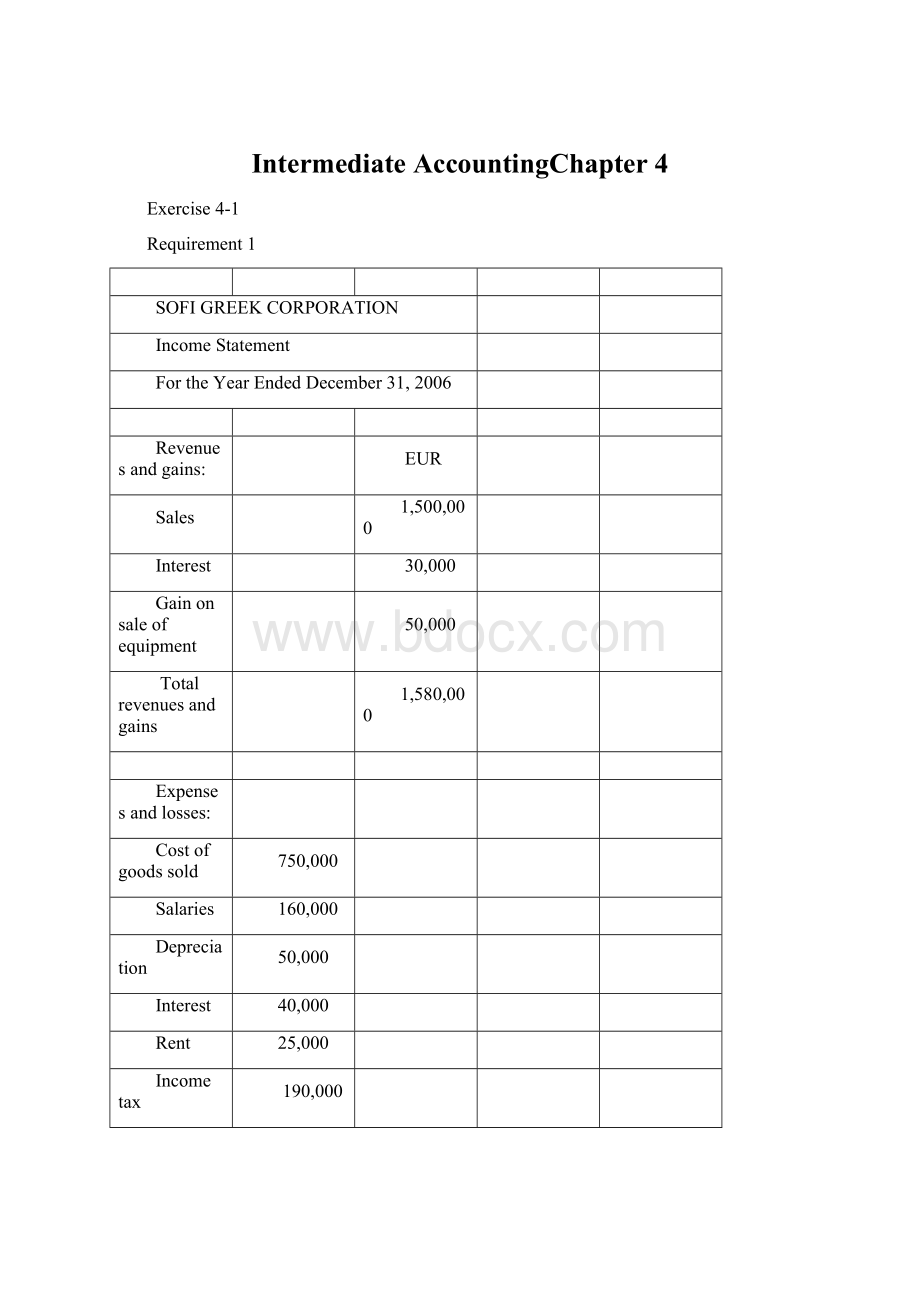

40,000

Rent

25,000

Incometax

190,000

Totalexpensesandlosses

1,215,000

Netincome

365,000

Earningspershare

3.65

Exercise4-1(concluded)

Requirement2

Salesrevenue

750,000

Grossprofit

Operatingexpenses:

Rent

25,000

Totaloperatingexpenses

235,000

Operatingincome

515,000

Otherincome(expense):

Interestrevenue

Interestexpense

(40,000)

Totalotherincome,net

40,000

Incomebeforeincometaxes

555,000

Incometaxexpense

3.65

Exercise4-2

THEAVINASHGROUP

StatementofIncomeandComprehensiveIncome(inpart)

INR

1,354,000

Othercomprehensiveincome(loss):

Foreigncurrencytranslationgain,netoftax

140,000

Unrealizedlossesoninvestmentsecurities,

netoftax

(56,000)

Totalothercomprehensiveincome

84,000

Comprehensiveincome

1,438,000

StatementofComprehensiveIncome

Unrealizedlossesoninvestmentsecurities

Exercise4-3

lECOLECORPORATION

StatementofIncomeandComprehensiveIncome

2,400,000

1,400,000

1,000,000

Sellingandadministrative

450,000

550,000

Incomebeforeincometaxesandextraordinaryitem

510,000

Incometaxexpense*

153,000

Incomebeforeextraordinaryitem

Extraordinaryitem:

Gainonearlydebtextinguishment(netof120,000

taxexpense)

Netincome

Othercomprehensiveincome:

Unrealizedholdinggainsoninvestmentsecurities,

357,000

280,000

637,000

56,000

693,000

Earningspershare:

Extraordinarygain

0.36

0.28

0.64

*30%x510,000

Exercise4-4

LEDHASENCORPORATION

Rentalrevenue

80,000

2,480,000

1,200,000

Salaries

300,000

100,000

90,000

Lossonsaleofequipment

20,000

Lossfrominventorywrite-down

200,000

208,000

2,168,000

Lossfromflooddamage(netof48,000taxbenefit)

312,000

(72,000)

240,000

Extraordinaryloss

1.04

(.24)

.80

*40%x520,000

Exercise4-4(concluded)

FortheYearEndedDecember31,2006EUR

2,400,000

Depreciation

650,000

(20,000)

(90,000)

Totalotherincome(expense),net

(30,000)

Incomebeforetaxesandextraordinaryitem

520,000

208,000

1.04

(.24).80

Exercise4-5

ALIANTCOMPANY

PartialIncomeStatement

Incomefromcontinuingoperations

350,000

Discontinuedoperations:

Lossfromoperationsofdiscontinuedcomponent

(includinglossondisposalof400,000)*

(520,000)

Incometaxbenefit

Lossondiscontinuedoperations

(312,000)

38,000

3.50

Lossfromdiscontinuedoperations

(3.12)

.38

*Lossondiscontinuedoperations:

Lossonsaleofassets(400,000)

Operatingloss(120,000)

Totalbefore-taxloss(520,000)

Less:

Incometaxbenefit(40%)208,000

Net-of-taxloss(312,000)

Exercise4-6

FIGUROCORPORATION

600,000

320,000

280,000

Selling

67,000

Administrative

87,000

Restructuringcosts

55,000

209,000

71,000

Interestanddividends

32,000

(26,000)

6,000

77,000

Incometaxexpense*

30,800

Gainonearlydebtextinguishment(netof34,400

46,200

51,600

97,800

.46

.52

0.98

*40%x77,000

Exercise4-7

ESTRELLAENTERPRISES,INC.

FortheYearEndedDecember31,2006

400,000

(includingimpairmentlossof50,000)*

(195,000)

Incometaxbenefit

78,000

(117,000)

283,000

Operatingloss(145,000)

Impairmentloss(250,000-200,000)(50,000)

Netbefore-taxloss(195,000)

Incometaxbenefit(40%)78,000

Netafter-taxlossondiscontinuedoperations(117,000)

Lossfromoperationsofdiscontinuedcomponent*

(145,000)

Incometaxbenefit

58,000

(87,000)

313,000

*Includesonlytheoperatinglossduringtheyear.Thereisnoimpairmentloss.

Exercise4-8

ENRIQUESCOMPANY

Incomefromcontinuingoperations*

547,200

Incomefromoperationsofdiscontinuedcomponent

(includinglossondisposalof350,000)

150,000

Incometaxexpense

60,000

Incomeondiscontinuedoperations

90,000

Netincome

637,200

*Incomefromcontinuingoperations:

Incomebeforeconsideringadditionalitems1,000,000

Decreaseinincomeduetorestructuringcosts(88,000)

Before-taxincomefromcontinuingoperations912,000

Incometaxexpense(40%)(364,800)

Incomefromcontinuingoperations547,200

Exercise4-9

Thisisachangeinaccountingestimate.

Whenanestimateisrevisedasnewinformationcomestolight,accountingforthechangeinestimateisquitestraightforward.Wedonotrestateprioryears'

financialstatementstoreflectthenewestimate.Instead,wemerelyincorporatethenewestimateinanyrelatedaccountingdeterminationsfromthereon.Iftheafter-taxincomeeffectofthechangeinestimateismaterial,theeffectonnetincomeandearningspersharemustbedisclosedinanote,alongwiththejustificationforthechange.

Requirement3

850,000Cost

170,000Olda

升级会员

升级会员