FUNDAMENTAL ACCOUNTING Lesson notes 14Word文件下载.docx

《FUNDAMENTAL ACCOUNTING Lesson notes 14Word文件下载.docx》由会员分享,可在线阅读,更多相关《FUNDAMENTAL ACCOUNTING Lesson notes 14Word文件下载.docx(18页珍藏版)》请在冰豆网上搜索。

Studentsmajorinaccounting0hours

Otherstudents6hours

Teachingcontents

Introduction

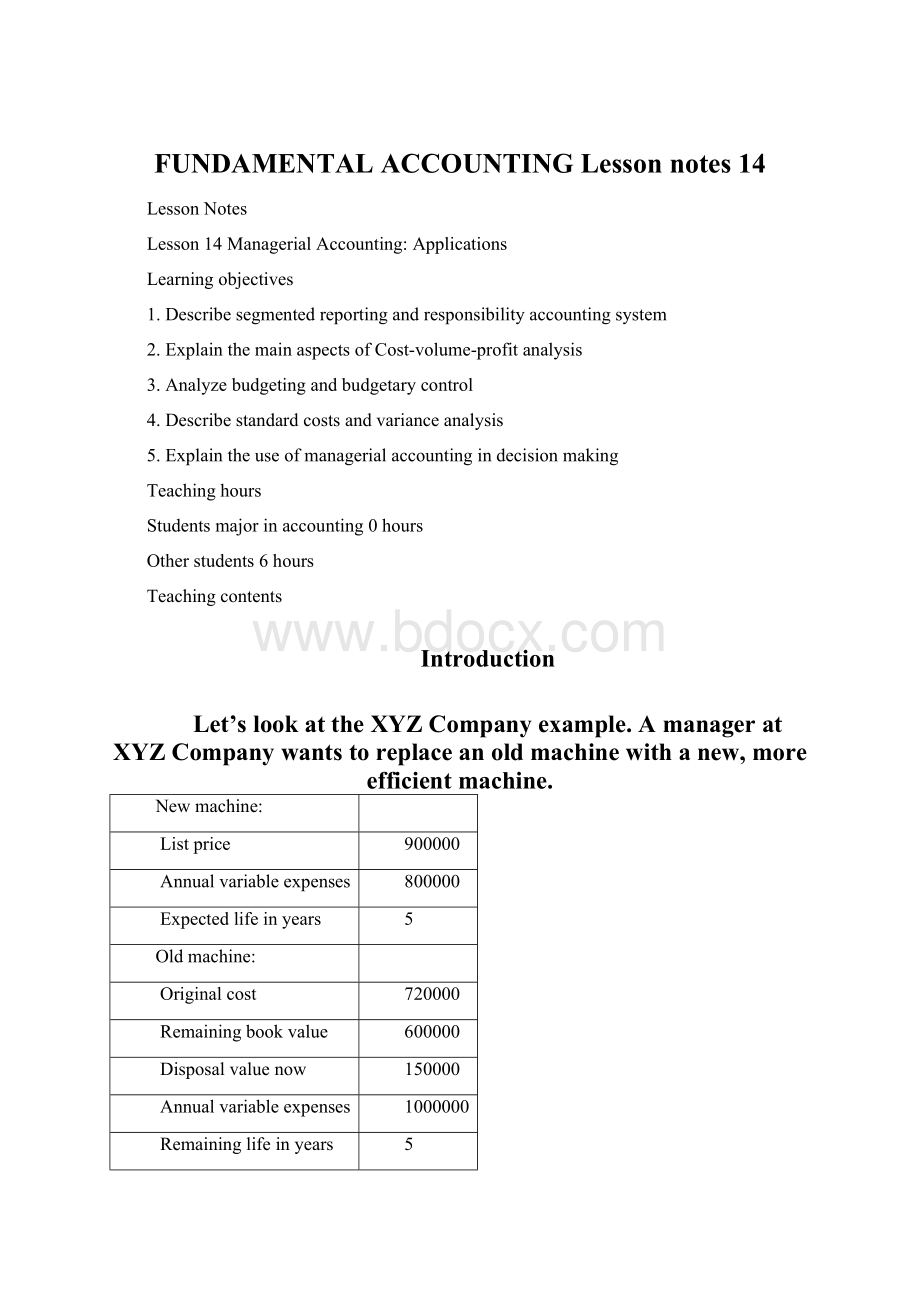

Let’slookattheXYZCompanyexample.AmanageratXYZCompanywantstoreplaceanoldmachinewithanew,moreefficientmachine.

Newmachine:

Listprice

900000

Annualvariableexpenses

800000

Expectedlifeinyears

5

Oldmachine:

Originalcost

720000

Remainingbookvalue

600000

Disposalvaluenow

150000

1000000

Remaininglifeinyears

XYZ’ssalesare$2000000peryear.Fixedexpenses,otherthanamortization,are$700000peryear.Shouldthemanagerpurchasethenewmachine?

Themanagerrecommendsthatthecompanynotpurchasethenewmachinesincedisposaloftheoldmachinewouldresultinaloss:

Remainingbookvalue

Disposalvalue

-150000

Lossfromdisposal

450000

(1)Isitcorrect?

(2)What’syourcommenttothemanager’sdecision?

Afterlearningthischapter,youwillknowhowtoemploythetoolsofmanagerialaccountingandmakedecisionscorrectly.

SegmentedReportingandResponsibilityAccountingSystems

SegmentedReportingOrganizationsmaybreakdowntheiroperationsintovarioussegments,suchasdivisions,stores,services,ordepartments.Thus,managementneedsreportsoneachsegmentforcostmanagementandperformanceevaluation.

Segmentsmaybeevaluatedasacostcentre,aprofitcentre,whereprofitcentrereportsincludeinformationonasegment’srevenuesandcosts,andaninvestmentcentre.

Somecostsaredirectandsomeareindirect,andindirectcostsmaybeallocatedtovariousdepartments.Servicedepartmentcostsaresharedindirectexpensesofoperationdepartments.Theymaybeallocatedusingavarietyofbases.Pleaserefertothefollowingtable:

ServiceDepartment

CommonAllocationBases

GeneralOffice

Numberofemployees

Personnel

Payroll

Advertising

Sales

Purchasing

NumberofPurchaseOrders

Cleaning

Floorspaceoccupied

Maintenance

ResponsibilityAccountingSystemResponsibilityaccountingsystemisanaccountingsystemwhichassignsmanagerstheresponsibilityforcostsandexpensesundertheircontrol.

Responsibilityaccountingbudgetsarepreparedpriortoeachaccountingperiod.Responsibilityaccountingperformancereportscompareactualcostsandexpensestobudgetedamounts

Cost-volume-profitAnalysis

CVPanalysisisusedtoanswerthequestionssuchas

(1)HowmuchmustIselltoearnmydesiredincome?

(2)HowwillincomebeaffectedifIreducesellingpricestoincreasesalesvolume?

(3)HowwillincomebeaffectedifIchangethesalesmixofmyproducts?

....

ThebasicassumptionsofCVPanalysisisthatCVPanalysisassumesrelationscanbeexpressedasstraightlineswithintherelevantrange,whichmeansthatunitsellingpriceremainsconstant,unitvariablecostsremainconstant,andtotalfixedcostremainconstant.Iftheexpectedcostandrevenuebehaviourisdifferentfromtheassumptions,thentheresultsofCVPanalysisareoflimiteduse.

Theobjectiveofthecostanalysisisdeterminationoftotalfixedcostandthevariableunitcost.Thebasicmethodstoestimatethetotalcostsequationinclude:

(1)scatterdiagram;

(2)high-lowmethod;

and(3)least-squaresregression.Hereleast-squaresregressionisusuallycoveredinadvancedcostaccountingcourses.Itiscommonlyusedwithcomputersoftwarebecauseofthelargenumberofcalculationsrequired.

Break-evenAnalysisThebreak-evenpointistheuniquesaleslevelatwhichacompanyneitherearnsaprofitnorincursaloss.Thebreak-evenpointmaybeexpressedinunitsorindollarsofsales.

ComputingIncomefromExpectedSalesTheincomegivenapredictedlevelofsalescanbecomputedasfollows:

SalesVolumeNeededtoEarnaTargetIncomeBreak-evenformulascanbeadjustedtoshowthesalesvolumeneededtoearnanyamountofincome.

MarginofSafetyMarginofsafetyisusedtoestimatehowmuchsalescandecreasebeforethecompanyincursaloss?

SensitivityAnalysisSensitivityanalysisisusedtoestimatetheeffectsofchangesinvariablessuchassalesprice,variablecosts,andfixedcosts.CVPanalysiscanbeusedtoshowtheeffectsofsuchchanges.

BudgetingandBudgetaryControl

BudgetsBudgetsareformalstatementsofacompany’splansexpressedinmonetaryterms,whichattempttocapturethefutureactivitiesofanorganization.Theyareusedbybusinesses,not-for-profit,government,educational,andothertypesoforganizations.

Theimportanceofbudgetinginclude

(1)definesgoalsandobjectives;

(2)promotesanalysisandafocusonthefuture;

(3)motivatesemployees;

(4)providesabasisforevaluatingperformance;

(5)coordinatesbusinessactivities;

(6)communicatesplansandinstructions.

BudgetCommitteeconsistsofmanagersfromalldepartmentsoftheorganization.Itprovidescentralguidancetoinsurethatindividualbudgetssubmittedfromalldepartmentsarerealisticandcoordinated.Flowofbudgetdataisabottom-upprocess.

Budgethorizonsareusuallyforoneyear,butmayextendforseveralyears.Theannualoperatingbudgetmaybedividedintoquarterlyormonthlybudgets.

Rollingbudgetsmeanthatthebudgetmaybeatwelve-monthbudgetthatrollsforwardonemonthasthecurrentmonthiscompleted.

MasterBudgetMasterbudgetisaformal,comprehensiveplanforthefutureofacompany.Itconsistsofseveralbudgetslinkedtogethertoformacoordinatedplanfortheorganization.

SalesBudgetSalesbudgetisthestartingpointinthebudgetingprocess.Mostoftheotherbudgetsarelinkedtothesalesbudget.Salespersonnelareofteninvolvedindevelopingthesalesbudgets.

MerchandisePurchasesBudgetMerchandisepurchasesbudgetprovidesdetailedinformationaboutthepurchasesnecessarytofulfillthesalesbudgetandprovideadequateinventories.

Thequantitypurchasedisaffectedby:

(1)Just-in-timeinventorysystems,whichenablepurchasesofsmaller,frequentlydeliveredquantities;

(2)Safetystockinventorysystems,whichprovideprotectionagainstlostsalescausedbydelaysinsuppliershipments.

SellingExpenseBudgetSellingexpensebudgetliststhetypesandamountsofsellingexpenses.Predictionsofexpensesarebasedonthesalesbudgetandpastexperience.

GeneralandAdministrativeExpenseBudgetGeneralandadministrativeexpensebudgetliststhepredictedoperatingexpensesnotlistedinthesalesbudget.Itincludesbothcashandnon-cashexpensesandisoftenpreparedbytheofficemanagerorpersonresponsibleforgeneraladministration.

CapitalExpendituresBudgetCapitalexpendituresbudgetliststhecashinflowsoroutflowspertainingtothedisposaloracquisitionofcapitalequipment,anditisusuallyaffectedbytheorganization’slong-termplans.

CashBudgetCashBudgetliststheexpectedcashinflowsandoutflowsfortheperiod.Itisatoolusedbymanagementtoavoidexcesscashbalancesorcashshortages.Informationfromotherbudgetsisusedinitspreparation.Informationfromthecashbudgetisusedtopreparethebudgetedincomestatementandbalancesheet.

ProductionandManufacturingBudgetsManufacturingcompaniesneedtoprepareadditionalbudgetsthatinclude:

productionbudgets,directmaterialspurchasebudgets,directlabourbudgets,andmanufacturingoverheadbudgets.

Productionandmanufacturingbudgetsprovidesdetailedinformationabouttheproductionnecessarytofulfillthesalesbudgetandprovideadequateinventories.

Directmaterialsbudgetprovidesdetailedinformationaboutthepurchasesofrawmaterialsnecessarytofulfilltheproductionbudgetandprovideadequateinventories.

Directlabourandmanufacturingoverheadbudgetsprovidesinformationaboutthelabourandmanufacturingoverheadcostsgiventhelevelofproductionfortheperiod.

PreparingFinancialBudgets

BudgetaryControl

CapitalBudgetingCapitalbudgetinganalyzesalternativelong-terminvestmentsanddecidingwhichassetstoacquireorsell.Thesedecisionsrequirecarefulanalysissince:

(1)Theoutcomeisuncertain;

(2)Largeamountsofmoneyareusuallyinvolved;

(3)Investmentinvolvesalong-termcommitment;

(4)Anydecisionmaybedifficultorimpossibletoreverse.

Zero-basedBudgetingZero-basedbudgetingarepreparedassumingnopreviousactivitiesfortheactivitiesbeingplanned.Managersmustjustifytheamountsbudgetedforeachactivity.Itispopularamonggovernmentandnon-profitorganizations.

FixedBudgetFixedbudgetsarepreparedforasingle,predictedlevelofactivity.Performanceevaluationisdifficultwhenactualactivitydiffersfromthepredictedlevelofactivity.Forexample:

Howmuchoftheunfavourablecostvarianceisduetohigheractivity,andhowmuchisduetopoorcostcontrol?

Toanswerthesequestions,wemustflexthebudgettotheactuallevelofactivity

Flexible(Variable)BudgetsFlexiblebudgetsarepreparedafteraperiod’sactivitiesarecomplete.Theyshowrevenuesandexpensesthatshouldhaveoccurredattheactuallevelofactivity.Flexiblebudgetsrevealcostvariancesduetogoodcostcontrolorlackofcostcontrol,whichimproveperformanceevaluation.

Sinceflexiblebudgetsprepareabudgetfordifferentactivitylevels,wemustknowhowcostsbehavewi

升级会员

升级会员