assignment for accountingWord格式.docx

《assignment for accountingWord格式.docx》由会员分享,可在线阅读,更多相关《assignment for accountingWord格式.docx(7页珍藏版)》请在冰豆网上搜索。

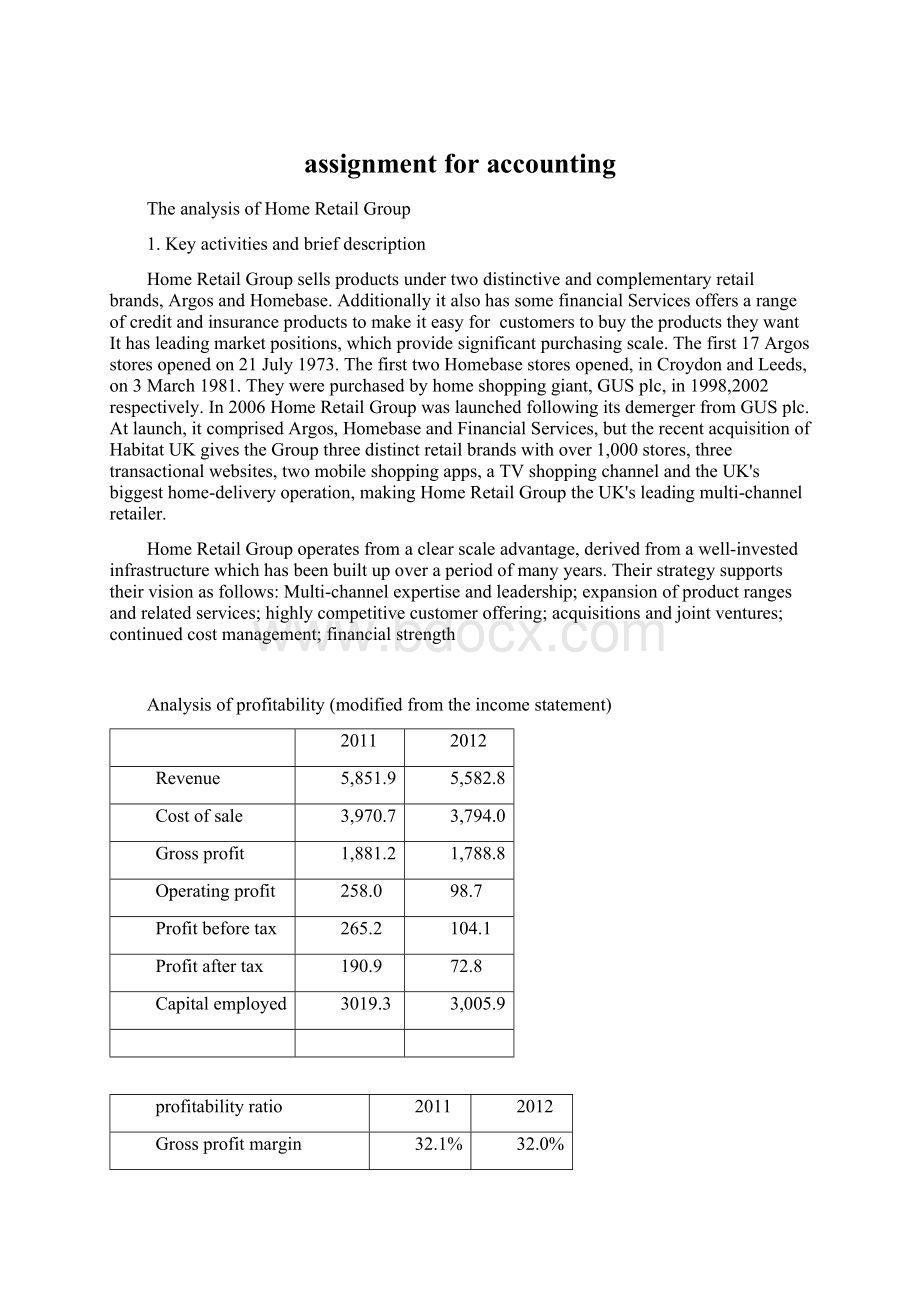

Costofsale

3,970.7

3,794.0

Grossprofit

1,881.2

1,788.8

Operatingprofit

258.0

98.7

Profitbeforetax

265.2

104.1

Profitaftertax

190.9

72.8

Capitalemployed

3019.3

3,005.9

profitabilityratio

Grossprofitmargin

32.1%

32.0%

Operatingprofitmargin

4.4%

1.7%

Pre-taxprofitmargin

4.5%

1.9%

Post-taxprofitmargin

3.3%

1.3%

Returnoncapitalemployed

8.5%

Returnonequity

7.0%

2.8%

Theprofitabilitythisyearisworsethanlastyear.

Thegrossprofitmargindecreaseslightly.Becausethefinancialcrisis,onthefactthatworking-classfamilieswerehammeredbytherecessionandhaven'

tgotoutofit.Theyreducetheconsumptionevenundersomeofthepromotionalactivities.Thereforrevenuedropsby4.6%from2011to2012,thecostofsaleincreaseby4.45%atthesametime.Butoverall,thegrossprofitmarginishighstillmorethan30%.

Intherespectoftheoperatingprofitmargin,thefigurefluctuatealot,whichdecreasefrom4.4%to1.7%.ThebigerosionofGPMcomesfromthesellingcosts,whichisabigandimportantpartofretailindustry.Additionally,theadministrativecostsincreasemorethan10%,whichthemainfactorsthatleadtoagreatincreaseintotalnetoperatingexpenseanddecreasetheoperatingprofitmargin.Inthiscase,itisnotagoodopportunityformanagementinvestorstoinvestthiscompany.Sothecompanyneedstocontrolthecostofsaleandadministrationaswellasincreasethecompetitiontogetthemostmarketsharetoincreaserevenueandimprovetheprofitability.

Thepre-taxprofitmargindeclinesfrom4.5%to1.9%,whichduetothedecreaseoffinanceincomeismorethantheincreaseoffinanceexpense.ThePostTPMalsodropsfrom3.3%to1.3%althoughthetaxexpensefellbyover£

33.

ROEandROCEaretwoimportantratios,whiletheydropfrom7%to2.8%and8.5%to3.3%respectively.Thecapitalemployeddecrease44%from2011to2012,becauseequitydecreasesmorethanborrowingsincrease.ROEalsodecreases,whichmeanslessprofitisavailabletoshareholdersasdividends.

Equityinvestorsshouldanalysisinvestmentratio

Figurescanbeseenformthetable:

Earningspershare

23.1

9.1

Dividendpershare

14.2

4.7

Dividendcover

1.626760563

1.93617

Dividendyield

1.10383536

0.500332668

Priceearningsratio

3.253246753

11.74725275

Althoughthenumberofshareholdershasdecreasenearly3.5%theEPShasreducedfrom£

23.1to£

9.1.Themostimportantreasonisthedropofprofit.Itisabadnewsforequityinvestors.

Dividendpershare2012almosthalfofthatin2011,notonlybecausein2012theBoardofDirectorsdoesnotrecommendafinaldividendinrespectoftheyearended3March2012,butalsoduetothefewerinterimdividend.Thisfiguremeansinvestorswillgetfewerdividendsfromthe

Thedividendcoverincreasefrom1.6to1.9,itmeanstheabilitytopaydividendsbecomestronger.Butduetothelimitationofratioanalysisandthesituationofdividendsdistribution,

Liquidityratio

currentasset

1,898.70

1,731.20

currentliability

1,118.50

1,002.70

inventory

1,016.80

933.2

tradepayable

58.70

55.8

costofsale

3,970.70

3,794.00

currentratio

1.69754135

1.726538346

liquidratio

0.788466696

0.795851202

inventorydays

93.46765054

89.77807064

Tradepayabledays

45.90651522

45.74525567

Tradereceivabledays

31.66672363

32.22549617

Toanalysisthefinancialpositionofthiscompany,bothcurrentratioandliquidratioincreasedwhichmeanstheshorttermdebtpayingabilityincreased.Theliquidratioislessthan1,mainlybecauseofthelargenumberofinventoriesforresale.

Theinventorydaysdecreasefrommorethan93daysin2011toabout90daysin2012,itisalittlehigh,anddonotmatchthe“justintime”principle,butitstillcanbeacceptbecauseofthewholesaleandretailindustry.Largeinventoriesincreasethecostofstoreandmanagementbutitprovidesenoughchoicesforcustomersandensuresthemarketsharetocertainextent.

Tradepayabledaysin2012almostthesameasthatin2011.Oneandahalfmonthlessthanperiodoftradereceivabledays,whichmeansthecompanycanusethetradereceivabletomeetthetradepayableandlesstheuseofcash.

Gearingratio

Debttoequity

Netdebttoequity

-0.07400777

-0.058113235

Interestcover

5.139442231

2.039256198

Netinterestcover

Thedebttoequitydropsfrom14.49%to10.15%whichmeansthatthecompanyrelieslessonthemoneyfromborrowing.Thedecreaseindicatesthatthecompany’slong-termdebtpayingabilityimproved.

Netdebttoequityislessthandebttoequitybecauseofthedeductionofcashfromthenon-currentliabilities.Thisratiodecreasesfrom7.09%in2011to4.33%in2012andthedeviationfromlastyearmeansthelowerriskofthebusinessfailingin2012.

WhenitcomestoInterestcover,thedecreaseofthisratiodemonstratethattheabilitytopaytheinterestbecomeweakerandthedecreaseofprofitabilityandstability.

Cashflowpershare

0.321785156

0.258558446

Thecashflowpershareshowsthepercentageofnetcashflowfromoperatingactivitiesandtotalnumberofequityshare.Althoughthetotalnumberofequitysharesdecrease,theratiostilldecrease,becausethenetcashflowfromoperatingactivitiesdropsmorethan20%.ThisratioismorethanEPS,duetothenetcashflowgeneratedbythecompany’snormaloperatingactivitiesalsoincludethecostsdeductedfromtheprofits,butdonotaffectthecashoutflowadjustments,suchasdepreciationcharges.Sothecashflowislessthantheprofit.CFPSindicatethehighestamountofcashdividends,whileEPScannotshowthisability.

Appendix:

Profitability:

1.Grossprofitmargin=grossprofit/revenue

2011:

=1,881.20/5,851.90=0.321

2012:

=1,788.80/5,582.80=0.320

2.Operatingprofitmargin=operatingprofit/revenue

=258/5,851.90=0.044

=98.7/5,582.80=0.018

3.pre-taxprofitmargin=pre-taxprofit/revenue

=265.2/5,851.90=0.045

=104.1/5,582.80=0.019

4.post-taxprofitmargin=post-taxprofit/revenue

=190.9/5,851.90=0.033

=72.8/5,582.80=0.013

5.Returnoncapitalemployed=operatingprofit/totalcapitalemployed

=258/3,019.3=0.085

=98.7/3,005.9=0.033

6.Returnonequity=profitaftertax/equity

=190.9/2,741.20=0.070

=72.8/2,625.4=0.028

Investmentratio

1.Earningspershare(EPS)=profitaftertax/totalnumberofequityshares*100

=23.1

=9.1

1.Dividendpershare(DPS)itisgiven

2011:

=(38.1+79.9)/831.3=14.2pperordinaryshare

=37.6/803.3=4.7pperordinaryshare.

2.Dividendcover(DC)=EPS/DPS

=23.1/14.2=1.626760563

=9.1/4.7=1.93617

3.Dividendyield=totaldividend/currentmarketprice*100

ThecurrentmarketpricecangetfromtheLondonexchangestockwhichis106.90for22Nov2012

Thecurrentmarketpricefor22Nov2011cangetformhistoricalpriceYAHOOfinance,whichwas75.15.

=118/106.90=1.10383536

=37.6/75.15=0.500332668

4.PriceEarningsratio=currentmarketprice/EPS

=75.15/23.1=3.253246753

=106.90/9.1=11.74725275

Liquidity

1.Currentratio=currentasset/currentliability=

=1,898.70/1,118.50=1.69754135

=1,731.20/1,002.70=1.7265383

2.Liquidratio=(currentasset-inventory)/currentliability=

=881.9/1,118.50=0.788466696

=798.0/1,002.70=0.7958512

3.Inventorydays=(inventory/costofsales)*365

=(1,016.80/3,970.70)*365=93.46765054

=(933.2/3,794.00)*365=89.778071

4.Tradereceivabledays=tradereceivables/revenue*365

=507.7/5,851.90*365=31.66672363

=492.9/5,582.80*365=32.22549617

5.tradepayablesdays=(tradepayables/costofsales)*365

=499.4/3,970.70*365=45.90651522

=475.5/3,794.00*365=45.74525567

Gearing

1.debttoequity=non-currentborrowings/equity*100

=0/2,625.4=0

=0/2,741.2=0

2.Netdebtequity=Borrowingslesscash/Totalequity

=(0-194.3)/2,625.4=-0.07400777

=(0-159.3)/2,741.2=-0.058113235

3.Interestcover=operatingprofit/interest

=258/50.2=5.139442

升级会员

升级会员