金融计量学例题.docx

《金融计量学例题.docx》由会员分享,可在线阅读,更多相关《金融计量学例题.docx(27页珍藏版)》请在冰豆网上搜索。

金融计量学例题

中国香港股市模型

一、研究目的

研究中国香港股市变化规律,分析影响股价变动的主要因素。

二、影响因素分析

被解释变量Y是香港恒生指数,影响因素主要从以下三个方面考虑:

(1)股票市场自身交易情况,用成交额X1(百万美元)综合反映。

(2)国民经济发展状况,除了反映经济发展水平的人均生产总值X2(现价美元)之外,由于不动产是香港投资上致富的主要源泉,房地产交易也是香港经济十分重要的组成部分,因此要考虑另外两个影响因素:

建筑业总开支X3(百万美元)和房地产买卖金额X4(百万美元),以便分析整个国民经济以及各个重要组成部分的发展对香港股市的影响

(3)金融环境的变化,取九九金价X5(美元/两)、港汇指数x6、优惠利率X7等因素,从贵金属、汇率、利率等方面反映金融环境对香港股价波动的影响。

恒生指数及其影响因素的统计资料

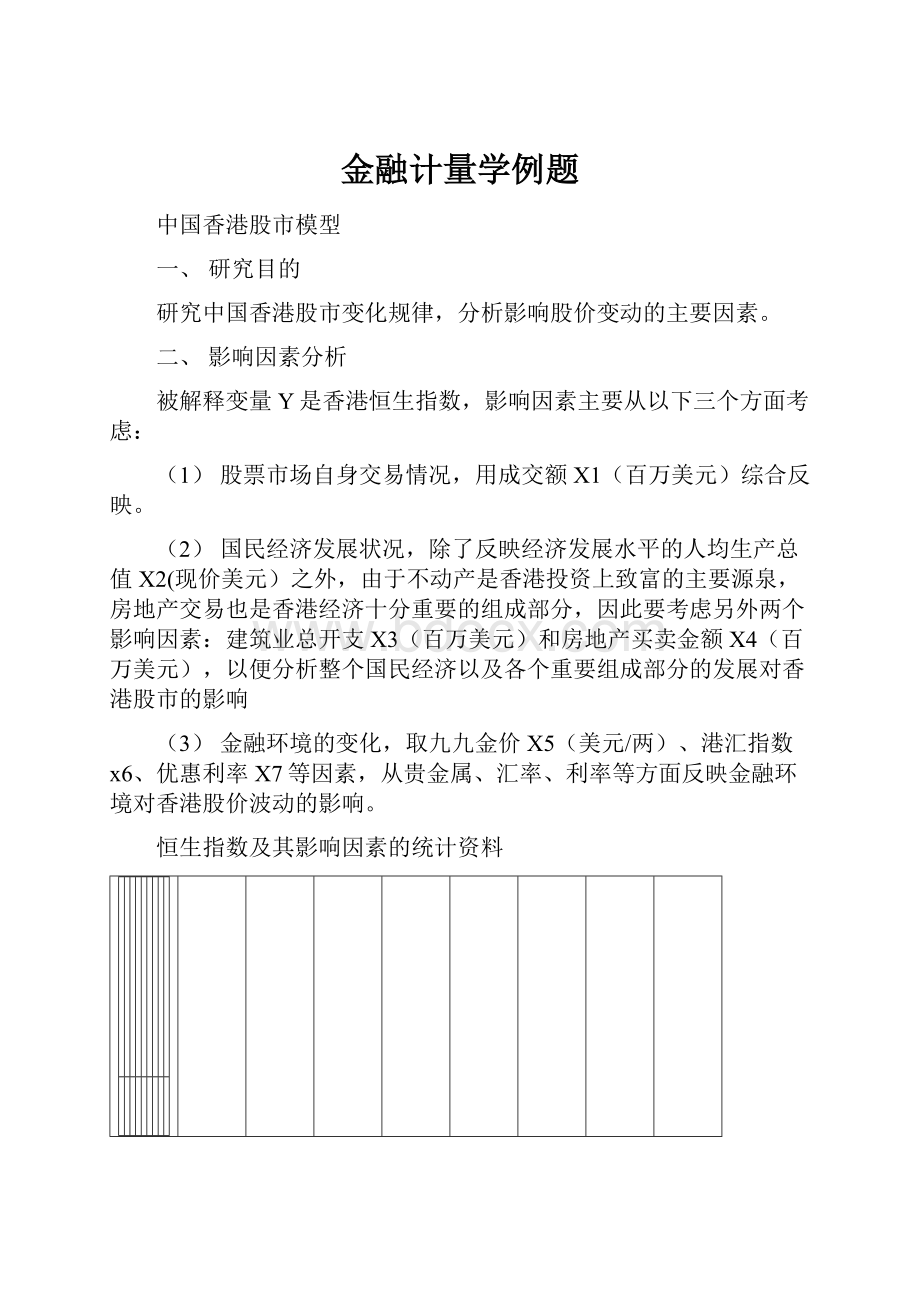

恒生指数

成交额

人均生

产总值

建筑业

总开支

房地产

买卖金额

九九金价

港汇指数

利率

y

x1

x2

x3

x4

x5

x6

x7

1991

172.9

11246

10183

4110

11242.5

681

105.9

9

1992

352.94

10335

10414

3996

12693.94

791

107.4

6.5

1993

447.67

131156

13134

4689

16681.34

607

114.4

6

1994

404.02

6127

15033

6876

22131.88

714

110.8

4.75

1995

409.51

27419

17389

8636

31353.64

911

99.4

4.75

1996

619.17

25633

21715

12339

43528.81

1231

91.1

9.5

1997

1121.17

95684

27075

16623

70752.98

2760

90.8

10

1998

1506.84

105987

31827

19937

125989.84

2651

86.3

16

1999

1105.79

46230

35393

24787

99468.48

2105

125.3

10.5

2000

933.03

37165

38832

25112

82478.3

3030

107.4

10.5

2001

1008.54

48787

46079

24414

54936.3

2810

106.6

8.5

2002

1567.56

75808

47871

22970

87135.51

2649

115.7

6

2003

1960.06

123128

54372

24403

129884.03

3031

110.1

6.5

2004

2884.88

371406

65602

30531

163044.2

3644

105.8

5

2005

2556.72

198569

74917

37861

215033.62

3690

101.6

5.25

三、多重共线性分析

可用逐步回归法进行变量选择

DependentVariable:

Y

Method:

LeastSquares

Date:

12/20/09Time:

22:

07

Sample:

19741988

Includedobservations:

15

Variable

Coefficient

Std.Error

t-Statistic

Prob.

C

493.6722

158.5363

3.113937

0.0082

X1

0.007337

0.001244

5.895809

0.0001

R-squared

0.727809

Meandependentvar

1136.720

AdjustedR-squared

0.706871

S.D.dependentvar

823.0463

S.E.ofregression

445.6086

Akaikeinfocriterion

15.16032

Sumsquaredresid

2581372.

Schwarzcriterion

15.25473

Loglikelihood

-111.7024

F-statistic

34.76056

Durbin-Watsonstat

1.327326

Prob(F-statistic)

0.000053

DependentVariable:

Y

Method:

LeastSquares

Date:

12/20/09Time:

22:

09

Sample:

19741988

Includedobservations:

15

Variable

Coefficient

Std.Error

t-Statistic

Prob.

C

-147.2516

151.9300

-0.969207

0.3501

X2

0.037776

0.003865

9.773950

0.0000

R-squared

0.880218

Meandependentvar

1136.720

AdjustedR-squared

0.871004

S.D.dependentvar

823.0463

S.E.ofregression

295.6060

Akaikeinfocriterion

14.33950

Sumsquaredresid

1135978.

Schwarzcriterion

14.43390

Loglikelihood

-105.5462

F-statistic

95.53011

Durbin-Watsonstat

1.389152

Prob(F-statistic)

0.000000

DependentVariable:

Y

Method:

LeastSquares

Date:

12/20/09Time:

22:

09

Sample:

19741988

Includedobservations:

15

Variable

Coefficient

Std.Error

t-Statistic

Prob.

C

-80.15322

211.5083

-0.378960

0.7108

X3

0.068291

0.010294

6.634063

0.0000

R-squared

0.771973

Meandependentvar

1136.720

AdjustedR-squared

0.754432

S.D.dependentvar

823.0463

S.E.ofregression

407.8587

Akaikeinfocriterion

14.98328

Sumsquaredresid

2162534.

Schwarzcriterion

15.07769

Loglikelihood

-110.3746

F-statistic

44.01080

Durbin-Watsonstat

1.022370

Prob(F-statistic)

0.000016

DependentVariable:

Y

Method:

LeastSquares

Date:

12/20/09Time:

22:

10

Sample:

19741988

Includedobservations:

15

Variable

Coefficient

Std.Error

t-Statistic

Prob.

C

133.3664

117.5810

1.134251

0.2772

X4

0.012904

0.001209

10.67062

0.0000

R-squared

0.897526

Meandependentvar

1136.720

AdjustedR-squared

0.889644

S.D.dependentvar

823.0463

S.E.ofregression

273.4151

Akaikeinfocriterion

14.18342

Sumsquaredresid

971825.5

Schwarzcriterion

14.27783

Loglikelihood

-104.3757

F-statistic

113.8620

Durbin-Watsonstat

1.716793

Prob(F-statistic)

0.000000

DependentVariable:

Y

Method:

LeastSquares

Date:

12/20/09Time:

22:

10

Sample:

19741988

Includedobservations:

15

Variable

Coefficient

Std.Error

t-Statistic

Prob.

C

-194.0396

220.6236

-0.879505

0.3951

X5

0.637642

0.093473

6.821702

0.0000

R-squared

0.781643

Meandependentvar

1136.720

AdjustedR-squared

0.764847

S.D.dependentvar

823.0463

S.E.ofregression

399.1167

Akaikeinfocriterion

14.93995

Sumsquaredresid

2070823.

Schwarzcriterion

15.03436

Loglikelihood

-110.0496

F-statistic

46.53562

Durbin-Watsonstat

0.974820

Prob(F-statistic)

0.000012

DependentVariable:

Y

Method:

LeastSquares

Date:

12/20/09Time:

22:

11

Sample:

19741988

Includedobservations:

15

Variable

Coefficient

Std.Error

t-Statistic

Prob.

C

1482.477

2347.499

0.631514

0.5387

X6

-3.285416

22.20766

-0.147941

0.8847

R-squared

0.001681

Meandependentvar

1136.720

AdjustedR-squared

-0.075113

S.D.dependentvar

823.0463

S.E.ofregression

853.3975

Akaikeinfocriterion

16.45989

Sumsquaredresid

9467734.

Schwarzcriterion

16.55430

Loglikelihood

-121.4492

F-statistic

0.021886

Durbin-Watsonstat

0.215522

Prob(F-statistic)

0.884660

DependentVariable:

Y

Method:

LeastSquares

Date:

12/20/09Time:

22:

12

Sample:

19741988

Includedobservations:

15

Variable

Coefficient

Std.Error

t-Statistic

Prob.

C

1337.975

621.3416

2.153364

0.0506

X7

-25.42163

73.42366

-0.346232

0.7347

R-squared

0.009137

Meandependentvar

1136.720

AdjustedR-squared

-0.067083

S.D.dependentvar

823.0463

S.E.ofregression

850.2046

Akaikeinfocriterion

16.45240

Sumsquaredresid

9397021.

Schwarzcriterion

16.54680

Loglikelihood

-121.3930

F-statistic

0.119877

Durbin-Watsonstat

0.246059

Prob(F-statistic)

0.734708

从上述7个表可以看出,以X4为解释变量时,R2最大,但常数项不显著,就把不含常数项含X4的一元线性回归模型作为基本模型(所有不含常数项的一元线性回归模型中,此模型R2最大)

在此基础上分别加入X1,X2,X3,X5,X6,X7

DependentVariable:

Y

Method:

LeastSquares

Date:

12/20/09Time:

22:

21

Sample:

19741988

Includedobservations:

15

Variable

Coefficient

Std.Error

t-Statistic

Prob.

X4

0.010598

0.001061

9.988042

0.0000

X1

0.003000

0.000810

3.704267

0.0026

R-squared

0.945213

Meandependentvar

1136.720

AdjustedR-squared

0.940999

S.D.dependentvar

823.0463

S.E.ofregression

199.9192

Akaikeinfocriterion

13.55727

Sumsquaredresid

519580.1

Schwarzcriterion

13.65168

Loglikelihood

-99.67952

F-statistic

224.2834

Durbin-Watsonstat

1.190080

Prob(F-statistic)

0.000000

DependentVariable:

Y

Method:

LeastSquares

Date:

12/20/09Time:

22:

22

Sample:

19741988

Includedobservations:

15

Variable

Coefficient

Std.Error

t-Statistic

Prob.

X4

0.007698

0.002448

3.145342

0.0077

X2

0.016101

0.006054

2.659477

0.0197

R-squared

0.927066

Meandependentvar

1136.720

AdjustedR-squared

0.921456

S.D.dependentvar

823.0463

S.E.ofregression

230.6650

Akaikeinfocriterion

13.84338

Sumsquaredresid

691682.2

Schwarzcriterion

13.93778

Loglikelihood

-101.8253

F-statistic

165.2434

Durbin-Watsonstat

1.886847

Prob(F-statistic)

0.000000

DependentVariable:

Y

Method:

LeastSquares

Date:

12/20/09Time:

22:

26

Sample:

19741988

Includedobservations:

15

Variable

Coefficient

Std.Error

t-Statistic

Prob.

X4

0.011413

0.002914

3.916365

0.0018

X3

0.012656

0.013791

0.917717

0.3755

R-squared

0.894237

Meandependentvar

1136.720

AdjustedR-squared

0.886102

S.D.dependentvar

823.0463

S.E.ofregression

277.7686

Akaikeinfocriterion

14.21502

Sumsquaredresid

1003020.

Schwarzcriterion

14.30943

Loglikelihood

-104.6126

F-statistic

109.9165

Durbin-Watsonstat

1.648368

Prob(F-statistic)

0.000000

DependentVariable:

Y

Method:

LeastSquares

Date:

12/20/09Time:

22:

27

Sample:

19741988

Includedobservations:

15

Variable

Coefficient

Std.Error

t-Statistic

Prob.

X4

0.010146

0.002249

4.511236

0.0006

X5

0.166624

0.092648

1.798469

0.0954

R-squared

0.909822

Meandependentvar

1136.720

AdjustedR-squared

0.902885

S.D.dependentvar

823.0463

S.E.ofregression

256.4876

Akaikeinfocriterion

14.05560

Sumsquaredresid

855216.8

Schwarzcriterion

14.15001

Loglikelihood

-103.4170

F-statistic

131.1597

Durbin-Watsonstat

1.546147

Prob(F-statistic)

0.000000

DependentVariable:

Y

Method:

LeastSquares

Date:

12/20/09Time:

22:

28

Sample:

19741988

Includedobservations:

15

Variable

Coefficient

Std.Error

t-Statistic

Prob.

X4

0.012874

0.001180

10.91316

0.0000

X6

1.310060

1.085108

1.207309

0.2488

R-squared

0.898739

Meandependentvar

1136.720

AdjustedR-squared

0.890950

S.D.dependentvar

823.0463

S.E.ofregression

271.7927

Akaikeinfocriterion

14.17152

Sumsquaredresid

960326.4

Schwarzcriterion

14.26593

Loglikelihood

-104.2864

F-statistic

115.3811

Durbin-Watsonstat

1.726650

Prob(F-statistic)

0.000000

DependentVariable:

Y

Method:

LeastSquares

Date:

12/20/09Time:

22:

28

Sample:

19741988

Includedobservations:

15

Variable

Coefficient

Std.Error

t-Statistic

Prob.

X4

0.013930

0.001168

11.92717

0.0000

X7

1.062945

13.41974

0.079208

0.9381

R-squared

0.887440

Meandependentvar

1136.720

AdjustedR-squared

0.878781

S.D.dependentvar

823.0463

S.E.ofregression

286.5559

Akaikeinfocriterion

14.27731

Sumsquaredresid

1067486.

Schwarzcriterion

14.37172

Loglikelihood

-105.0798

F-statistic

102.4936

Durbin-Watsonstat

1.705970

Prob(F-statistic)

0.000000

以X4、X1为解释变量的模型为基本回归模型,在此基础上分别加入x2、x3、x5、x6、x7得

DependentVariable:

Y

Method:

LeastSquares

Date:

12/20/09Time:

22:

33

Sample:

197

升级会员

升级会员