Chapter 5 Limiting Factors and Throughput Accounting5章限制因素和产出会计.docx

《Chapter 5 Limiting Factors and Throughput Accounting5章限制因素和产出会计.docx》由会员分享,可在线阅读,更多相关《Chapter 5 Limiting Factors and Throughput Accounting5章限制因素和产出会计.docx(15页珍藏版)》请在冰豆网上搜索。

Chapter5LimitingFactorsandThroughputAccounting5章限制因素和产出会计

Chapter5LimitingFactorsandThroughputAccounting

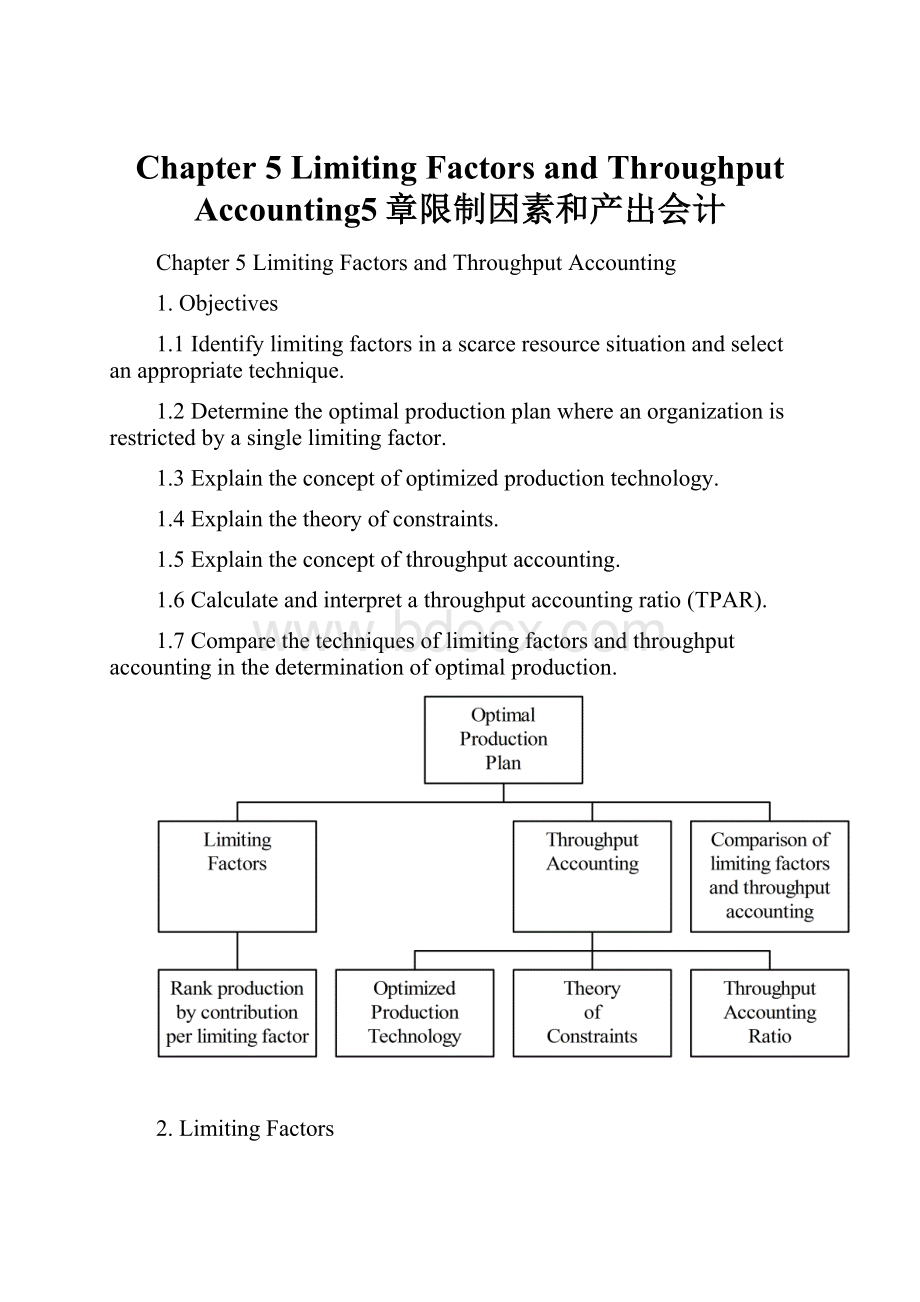

1.Objectives

1.1Identifylimitingfactorsinascarceresourcesituationandselectanappropriatetechnique.

1.2Determinetheoptimalproductionplanwhereanorganizationisrestrictedbyasinglelimitingfactor.

1.3Explaintheconceptofoptimizedproductiontechnology.

1.4Explainthetheoryofconstraints.

1.5Explaintheconceptofthroughputaccounting.

1.6Calculateandinterpretathroughputaccountingratio(TPAR).

1.7Comparethetechniquesoflimitingfactorsandthroughputaccountinginthedeterminationofoptimalproduction.

2.LimitingFactors

2.1

LimitingFactors

Alimitingfactorisanyfactorthatisinscarcesupplyandthatstopstheorganisationfromexpandingitsactivitiesfurther,thatis,itlimitstheorganisationsactivities.

2.2Anorganisationmightbefacedwithjustonelimitingfactor(otherthanmaximumsalesdemand)buttheremightalsobeseveralscarceresources,withtwoormoreofthemputtinganeffectivelimitonthelevelofactivitythatcanbeachieved.

2.3Examplesoflimitingfactorsincludesalesdemandandproductionconstraints.

(a)Labour.Thelimitmaybeeitherintermsoftotalquantityorofparticularskills.

(b)Materials.Theremaybeinsufficientavailablematerialstoproduceenoughunitstosatisfysalesdemand.

(c)Manufacturingcapacity.Theremaynotbesufficientmachinecapacityfortheproductionrequiredtomeetsalesdemand.

2.4Itisassumedinlimitingfactoranalysisthatmanagementwouldmakeaproductmixdecisionorservicemixdecisionbasedontheoptionthatwouldmaximiseprofitandthatprofitismaximizedwhencontributionismaximised(givennochangeinfixedcostexpenditureincurred).Inotherwords,marginalcostingideasareapplied.

(a)Contributionwillbemaximisedbyearningthebiggestpossiblecontributionperunitoflimitingfactor.ForexampleifgradeAlabouristhelimitingfactor,contributionwillbemaximisedbyearningthebiggestcontributionperhourofgradeAlabourworked.

(b)Thelimitingfactordecisionthereforeinvolvesthedeterminationofthecontributionearnedperunitoflimitingfactorbyeachdifferentproduct.

(c)Ifthesalesdemandislimited,theprofit-maximisingdecisionwillbetoproducethetoprankedproduct(s)uptothesalesdemandlimit.

2.5Inlimitingfactordecisions,wegenerallyassumethatfixedcostsarethesamewhateverproductorservicemixisselected,sothattheonlyrelevantcostsarevariablecosts.

2.6Whenthereisjustonelimitingfactor,thetechniqueforestablishingthecontribution-maximisingproductmixorservicemixistoranktheproductsorservicesinorderofcontribution-earningabilityperunitoflimitingfactor.

2.7

Example1

Sausagemakestwoproducts,theMashandtheSauce.Unitvariablecostsareasfollows.

Mash

Sauce

$

$

Directmaterials

1

3

Directlabour($3perhour)

6

3

Variableoverhead

1

1

8

7

Thesalespriceperunitis$14perMashand$11perSauce.DuringJulytheavailabledirectlabourislimitedto8,000hours.SalesdemandinJulyisexpectedtobeasfollows.

Mash

3,000units

Sauce

5,000units

Required:

Determinetheproductionbudgetthatwillmaximizeprofit,assumingthatfixedcostspermonthare$20,000andthatthereisnoopeninginventoryoffinishedgoodsorworkinprogress.

Solution:

1.Determinethelimitingfactor

Mash

Sauces

Total

Labourhoursperunit

2hrs

1hr

Salesdemand

3,000units

5,000units

Labourhoursneeded

6,000hrs

5,000hrs

11,000hrs

Labourhoursavailable

8,000hrs

Shortfall

3,000hrs

Labouristhelimitingfactoronproduction.

2.Identifythecontributionearnedbyeachproductperunitofscarceresource,thatis,perlabourhourworked.

Mash

Sauce

$

$

Salesprice

14

11

Variablecost

8

7

Unitcontribution

6

4

Labourhourperunit

2hrs

1hr

Contributionperlabourhour(=perunitoflimitingfactor)

$3

$4

Ranking

2

1

3.Determinethebudgetedproductionandsales.

Product

Units

Hoursneeded

Contributionperunit

Total

$

$

Sauces

5,000

5,000

4

20,000

Mashes(Bal.)

1,500

3,000

6

9,000

8,000

29,000

Less:

fixedcosts

20,000

Profit

9,000

Conclusion:

(1)Unitcontributionisnotthecorrectwaytodecidepriorities.

(2)Labourhoursarethescarceresource,thereforecontributionperlabourhouristhecorrectwaytodecidepriorities.

(3)TheSauceearns$4contributionperlabourhour,andtheMashearns$3contributionperlabourhour.Saucesthereforemakemoreprofitableuseofthescarceresource,andshouldbemanufacturedfirst.

Question1

TriproductLimitedmakesandsellsthreetypesofelectronicsecuritysystemsforwhichthefollowinginformationisavailable.

Standardcostandsellingpricesperunit

Product

Dayscan

Nightscan

Omniscan

$

$

$

Materials

70

110

155

Manufacturinglabour

40

55

70

Installationlabour

24

32

44

Variableoverheads

16

20

28

Sellingprice

250

320

460

Fixedcostsfortheperiodare$450000andtheinstallationlabour,whichishighlyskilled,isavailablefor25000hoursonlyinaperiodandispaid£8perhour.

Bothmanufacturingandinstallationlabourarevariablecosts.

Themaximumdemandfortheproductis:

Dayscan

Nightscan

Omniscan

2,000units

3,000units

1,800units

Required:

(a)Calculatetheshortfall(ifany)inhoursofinstallationlabour.(2marks)

(b)Determinethebestproductionplan,assumingthatTriproductLimitedwishestomaximiseprofit.(5marks)

(c)Calculatethemaximumprofitthatcouldbeachievedfromtheplaninpart(b)above.

(3marks)

(d)Havingcarriedoutaninvestigationoftheavailabilityofinstallationlabour,thefirmthinksthatbyoffering$12perhour,additionallabourwouldbecomeavailableandthusovercomethelabourshortage.

Required:

Basedontheresultsobtainedabove,advisethefirmwhetherornottoimplementthe

proposal.(5marks)

(Total15marks)

3.ThroughputAccounting(產量會計)

3.1Optimizedproductiontechnology(OPT)

3.1.1Duringthe1980sGoldrattandCox(1984)advocatedanewapproachtoproductionmanagementcalledOPT.OPTisbasedontheprinciplethatprofitsareexpandedbyincreasingthethroughputoftheplant.TheOPTapproachdetermineswhatpreventsthroughputbeinghigherbydistinguishingbottleneckandnon-bottleneckresources.

3.1.2Abottleneckmightbeamachinewhosecapacitylimitsthethroughputofthewholeproductionprocess.Theaimistoidentifybottlenecksandremovethemor,ifthisisnotpossible,ensurethattheyarefullyutilizedatalltimes.

3.1.3Non-bottleneckresourcesshouldbescheduledandoperatedbasedonconstraintswithinthesystem,andshouldnotbeusedtoproducemorethanthebottleneckscanabsorb.TheOPTphilosophythereforeadvocatesthatnon-bottleneckresourcesshouldnotbeutilizedto100%oftheircapacity,sincethiswouldmerelyresultinanincreaseininventory.

3.2Theoryofconstraints

3.2.1GoldrattandCox(1992)describetheprocessofmaximizingoperatingprofitwhenfacedwithbottleneckandnon-bottleneckoperationsasthetheoryofconstraints(TOC).

3.2.2TheTOCaimstoincreasethroughputcontributionwhilesimultaneouslyreducinginventoryandoperationalexpenses.However,thescopeforreducingthelatterislimitedsincetheymustbemaintainedatsomeminimumlevelforproductiontotakeplaceatall.Inotherwords,operationalexpensesareassumedtobefixedcosts.

3.2.3TheTOCadoptsashort-runtimehorizonandtreatsalloperatingexpenses(includingdirectlabourbutexcludingdirectmaterials)asfixed,thusimplyingthatvariablecostingshouldbeusedfordecision-making,profitmeasurementandinventoryvaluation.

3.2.4Itemphasizesthemanagementofbottleneckactivitiesasthekeytoimprovingperformancebyfocusingontheshort-runmaximizationofthroughputcontribution.

3.2.5

Example1–IllustrationoftheTOC

MachineXcanprocess1,000kgofrawmaterialperhour,machineY800kg.Ofaninputof900kg,100kgofprocessedmaterialmustwaitonthebottleneckmachine(machineY)attheendofanhourofprocessing.

Thetraditionalviewisthatmachinesshouldbeworking,notsittingidle.Soifthedesiredoutputfromtheaboveprocesswere8,100kgs,machineXwouldbekeptincontinualuseandall8,100kgswouldbeprocessedthroughthemachineinninehours.Therewouldbeabacklogof900kgs[8,100–(9hrs×800)]ofprocessedmaterialinfrontofmachineY,however.Allthismaterialwouldrequirehandlingandstoragespaceandcreatetheadditionalcostsrelatedtothesenon-valueaddedactivities.Itsprocessingwouldnotincreasethroughputcontribution.

3.3ThroughputAccounting(TA)

3.3.1GallowayandWaldron(1988)advocateanapproachcalledthroughputaccountingtoapplytheTOCphilosophy.

3.3.2

ThroughoutAccounting

Throughputaccountingisaproductmanagementsystemwhichaimstomaximisethroughput,andthereforecashgenerationfromsales,ratherthanprofit.Ajustintime(JIT)environmentisoperated,withbufferinventorykeptonlywhenthereisabottleneckresource.

3.3.3TAforJITissaidtobebasedonthreeconcepts.

(a)Concept1

Intheshortrun,mostcostsinthefactory(withtheexceptionofmaterialscosts)arefixed(theoppositeofABC,whichassumesthatallcostsarevariable).Thesefixedcostsincludedirectlabour.ItisusefultogroupallthesecoststogetherandcallthemTotalFactoryCosts(TFC).

(b)Concept2

InaJITenvironment,allinventoryisa'badthing'andtheidealinventorylevelisze

升级会员

升级会员