亨格瑞管理会计英文第15版练习答案06.docx

《亨格瑞管理会计英文第15版练习答案06.docx》由会员分享,可在线阅读,更多相关《亨格瑞管理会计英文第15版练习答案06.docx(43页珍藏版)》请在冰豆网上搜索。

亨格瑞管理会计英文第15版练习答案06

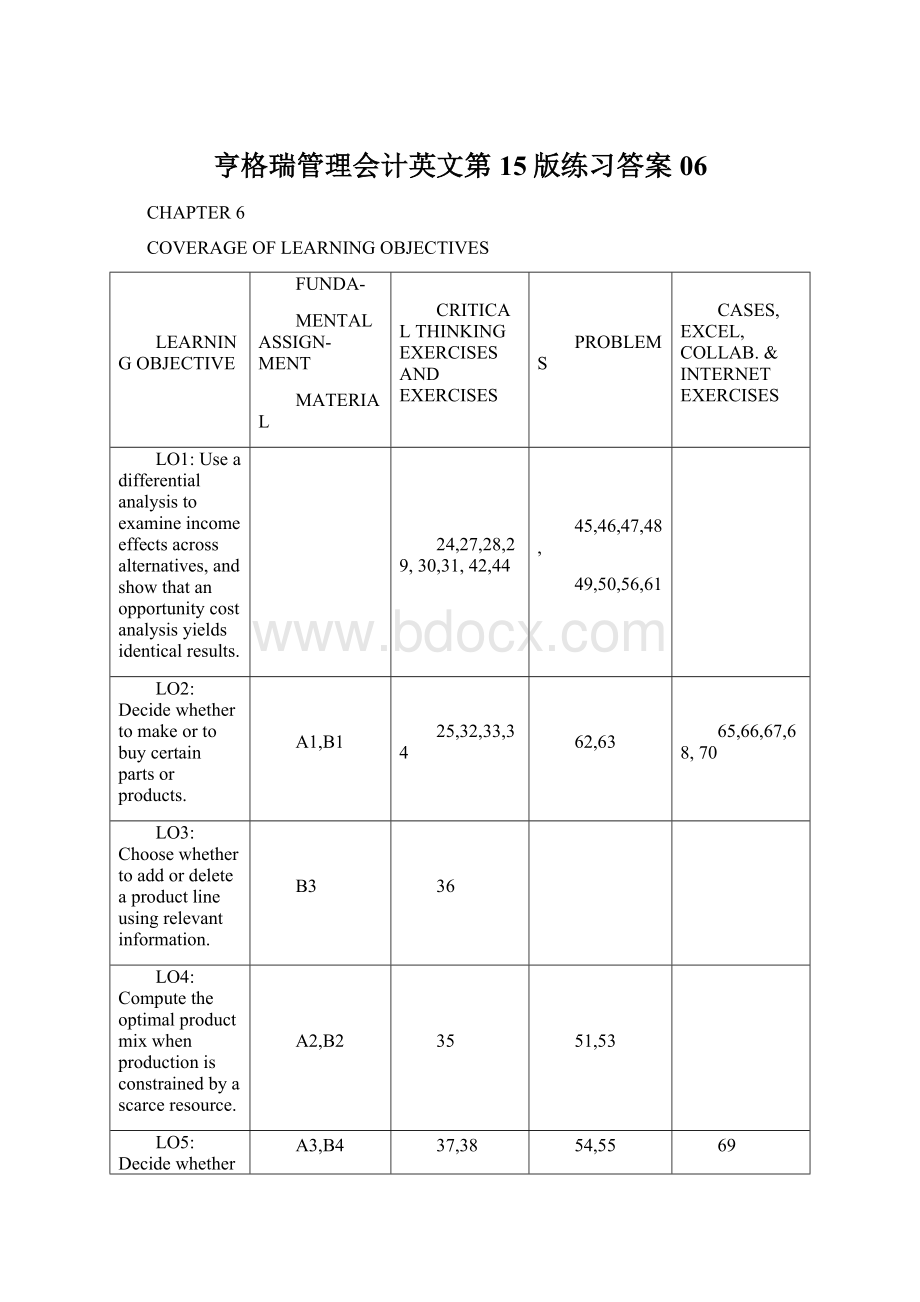

CHAPTER6

COVERAGEOFLEARNINGOBJECTIVES

LEARNINGOBJECTIVE

FUNDA-

MENTALASSIGN-MENT

MATERIAL

CRITICALTHINKINGEXERCISESANDEXERCISES

PROBLEMS

CASES,EXCEL,COLLAB.&INTERNETEXERCISES

LO1:

Useadifferentialanalysistoexamineincomeeffectsacrossalternatives,andshowthatanopportunitycostanalysisyieldsidenticalresults.

24,27,28,29,30,31,42,44

45,46,47,48,

49,50,56,61

LO2:

Decidewhethertomakeortobuycertainpartsorproducts.

A1,B1

25,32,33,34

62,63

65,66,67,68,70

LO3:

Choosewhethertoaddordeleteaproductlineusingrelevantinformation.

B3

36

LO4:

Computetheoptimalproductmixwhenproductionisconstrainedbyascarceresource.

A2,B2

35

51,53

LO5:

Decidewhetherajointproductshouldbeprocessedbeyondthesplit-offpoint.

A3,B4

37,38

54,55

69

LO6:

Decidewhethertokeeporreplaceequipment.

A4,B5

40

57,59

LO7:

Identifyirrelevantandmisspecifiedcosts.

26,39,41

52,58,64

71

LO8:

Discusshowperformancemeasurescanaffectdecisionmaking.

B6

43

60

CHAPTER6

RelevantInformationandDecisionMakingWithaFocusonOperationalDecisions

6-A1(20min)

1.Thekeytothisquestioniswhatwillhappentothefixedoverheadcostsifproductionoftheboxesisdiscontinued.Assumethatall$60,000offixedcostswillcontinue.Then,SunshineStatewilllose$20,000bypurchasingtheboxesfromWeyerhaeuser:

PaymenttoWeyerhaeuser,80,000×$2.10$168,000

Costssaved,variablecosts148,000

Additionalcosts$20,000

2.Somesubjectivefactorsare:

MightWeyerhaeuserraisepricesifSunshineStatecloseddownitsbox-makingfacility?

Willsub-contractingtheboxproductionaffectthequalityoftheboxes?

Isatimelysupplyofboxesassured,evenifthenumberneededchanges?

DoesSunshineStatesacrificeproprietaryinformationwhendisclosingtheboxspecificationstoWeyerhaeuser?

3.Inthiscasethefixedcostsarerelevant.However,itisnotthedepreciationontheoldequipmentthatisrelevant.Itisthecostofthenewequipment.Annualcostsavingsbynotproducingtheboxesnowwillbe:

Variablecosts$148,000

Investmentavoided(annualized)80,000

Totalsaved$228,000

ThepaymenttoWeyerhaeuseris$228,000-$168,000=$60,000lessthanthesavings,soSunshineStatewouldbe$60,000betteroffsubcontractingtheproductionoftheboxes.

6-A2(10min.)

1.Contributionmargins:

Plain=$70-$55=$15

Professional=$100-$75=$25

Contributionmarginratios:

Plain=$15÷$70=21.4%

Professional=$25÷$100=25%

2.PlainProfessional

a.Unitsperhour21

b.Contributionmarginperunit$15$25

Contributionmarginperhour$30$25

Totalcontributionfor20,000hours$600,000$500,000

3.Theplaincircularsawsarethebestuseofthescarcemachinehours.Foragivencapacity,thecriterionformaximizingprofitsistoobtainthegreatestpossiblecontributiontoprofitforeachunitofthelimitingorscarcefactor.Moreover,fixedcostsareirrelevantunlesstheirtotalisaffectedbythechoiceofproducts.

6-A3(15min.)Tableisinthousandsofdollars.

1,2.(a)(b)(a)-(b)(c)(a)-(b)-(c)

Separable

SalesSalesCostsIncremental

BeyondatIncrementalBeyondGainor

Split-OffSplit-OffSalesSplit-Off(Loss)

A23054176190(14)

B33032298300

(2)

C1755412110021

IncreaseinoveralloperatingincomefromfurtherprocessingofA,B,andC5

TheincrementalanalysisindicatesthatProductCshouldbeprocessedfurther,butProductsAandBshouldbesoldatsplit-off.Theoveralloperatingincomewouldbe$44,000,asfollows:

Sales:

$54,000+$32,000+$175,000$261,000

Jointcostofgoodssold$117,000

Separablecostofgoodssold100,000217,000

Operatingincome$44,000

Comparethiswiththepresentoperatingincomeof$28,000.Thatis,$230,000+$330,000+$175,000-($190,000+$300,000+$100,000+$117,000)=$28,000.Theextra$16,000ofoperatingincomecomesfromeliminatingthe$16,000lossresultingfromprocessingProductsAandBbeyondthesplit-offpoint.

6-A4(30-40min.)

Problem6-60isanextensionofthisproblem.Thetwoproblemsmakeagoodcombination.

1.Operatinginflowsforeachyear,oldmachine:

$910,000-($810,000+$60,000)$40,000

Operatinginflowsforeachyear,newmachine:

$910,000-($810,000+$22,000*)$78,000

*$60,000-$38,000

Cashflowstatements(inthousandsofdollars):

KeepReplace

ThreeThree

YearYearsYearsYearYearsYears

12&3Together12&3Together

Receipts,inflowsfromoperations40401207878234

Disbursements:

Purchaseof"old"equipment(90)*--(90)(90)--(90)

Purchaseof"new"equipment:

Totalcostslessproceeds

fromdisposalof"old"

equipment($99,000-$15,000)------(84)--(84)

Netcashinflow(outflow)(50)4030(96)7860

*Assumesthattheoutlayof$90,000tookplaceonJanuary2,2010,orsometimeduring2010.Somestudentswillignorethisitem,assumingcorrectlythatitisirrelevanttothedecision.However,notethatastatementfortheentireyearwasrequested.

Thedifferenceforthreeyearstakentogetheris$60,000-$30,000=$30,000.Noteparticularlythatthe$90,000bookvaluecanbeomittedfromthecomparison.Merelycrossouttheentireline。

althoughthecolumntotalswillbeaffected,thenetdifferencewillstillbe$30,000.

2.Incomestatements(inthousandsofdollars):

KeepReplace

ThreeThree

YearsYearsYearYearsYears

1,2&3Together12&3Together

Sales9102,7309109102,730

Expenses:

Otherexpenses8102,4308108102,430

Operatingofmachine60180222266

Depreciation3090*333399

Totalexpenses9002,7008658652,595

Lossondisposal:

Proceeds("revenue")----(15)--(15)

Bookvalue("expense")----90--90*

Loss----75--75

Totalcharges9002,7009408652,670

Netincome1030(30)4560

*Asinpart

(1),the$90,000bookvaluecanbeomittedfromthecomparisonwithoutchangingthe$30,000difference.Thiswouldmeandroppingthedepreciationitemof$30,000peryear(acumulativeeffectof$90,000)underthe"keep"alternative,anddroppingthebookvalueitemof$90,000inthelossondisposalcomputationunderthe"buy"alternative.

Differenceforthreeyearstogether,$60,000-$30,000=$30,000.

Notethemotivationalfactorshere.AmanagermaybereluctanttoreplacesimplybecausethelargelossondisposalwillseverelyharmtheprofitperformanceinYear1.

3.Thenetdifferenceforthethreeyearstakentogetherwouldbeunaffectedbecausetheitemisapastcost.Youcansubstituteanynumberfortheoriginal$90,000figurewithoutchangingthisanswer.

Forexample,examinehowtheresultswouldchangeinpart

(1)byinserting$1millionwherethe$90,000nowappears(inthousandsofdollars):

Keep:

Replace:

ThreeYearsThreeYears

TogetherTogetherDifference

Receipts,inflowsfromoperations120234114

Disbursements:

Purchaseofoldequipment(1,000)(1,000)0

Purchaseofnewequipment:

Grossprice(99)

Disposalproceedsof"old"15--(84)(84)

Netcashoutflow(880)(850)30

Insum,thismaybeahorriblesituation.Themanagerreallyblundered.Butkeepingtheoldequipmentwillcompoundtheblundertothecumulativetuneof$30,000overthenextthreeyears.

4.Diplomatically,Leeshouldtrytoconveythefollowing.Allofustendtoindulgeintheerroneousideathatwecansoothethewoundedprideofabadpurchasedecisionbyusingtheiteminsteadofreplacingit.Thefallacyisbelievingthatacurrentorfutureactioncaninfluencethelong-runimpactofapastoutlay.Allpastcostsaredownthedrain.Nothingcanchangewhathasalreadyhappened.The$90,000hasbeenspent.Subsequentaccountingfortheitemisirrelevant.Theschedulesinparts

(1)and

(2)clearlyshowthatwemaycompletelyignorethe$90,000originaloutlayandstillhaveacorrectanalysis.Theimportantpointisthatthe$90,000isnotanelementofdifferencebetweenalternativesand,therefore,maybesafelyignored.Theonlyrelevantitemsarethoseexpectedfutureitemsthatwilldifferbetweenalternatives.

5.The$90,000purchaseoftheoriginalequipment,thesales,andtheotherexpensesareirrelevantbecausetheyarecommontobothalternatives.Therelevantitemsarethefollowing(inthousandsofdollars):

ThreeYears

Together

KeepReplace

Operatingofmachine

(3×$60。

3×$22)$180$66

Incrementalcostofnewmachine:

Totalcost$99

Lessproceedsofoldmachine15

Incrementalcost--84

Totalrelevantcosts$180$150

Differenceinfavorofbuying$306-B1(15-20min.)

1.MakeBuy

TotalPerUnitTotalPerUnit

Purchasecost€10,000,000€50

Directmaterial€5,500,000€27.50

Directlabor1,900,0009.50

Factoryoverhead,variable1,100,0005.50

Factoryoverhead,fixed

avoided900,0004.50

Totalrelevantcosts€9,400,000€47.00€10,000,000€50

Differenceinfavorofmaking€600,000€3.00

Thenumericaldifferenceinfavorofmakingis€600,000or€3.00perunit.Therelevantfixedcostsare€900,000,not€3,000,000.

2.BuyandLeave

MakeCapacityIdleBuyandRent

Rentrevenue----€1,150,000

Obtainingofcomponents€(9,400,000)€(10,000,000)€(10,000,000)

Netrelevantcosts€(9,400,000)€(10,000,000)€(8,850,000)

Thefinalcolumnindicatesthatbuyingthecomponentsandrentingthevacatedcapacitywillyieldthebestresultsinthiscase.Thefavorabledifferenceis€9,400,000-€8,850,000=€550,000.

6-B2(15min.)

1.Iffixedmanufacturingcostisappliedtoproductsat$1.00permachinehour,ittakes$.75÷$1.00,or3/4ofanhourtoproduceoneunitofXY-7.Similarly,ittakes$.25÷$1.00or1/4ofanhourtoproduceBD-4.

2.Ifthereare100,000hoursofcapacity:

XY-7:

100,000hours÷3/4=133,333units.

BD-4:

100,000hou

升级会员

升级会员