IAsgns5.docx

《IAsgns5.docx》由会员分享,可在线阅读,更多相关《IAsgns5.docx(10页珍藏版)》请在冰豆网上搜索。

IAsgns5

LESSON5

Suggestedsolutions

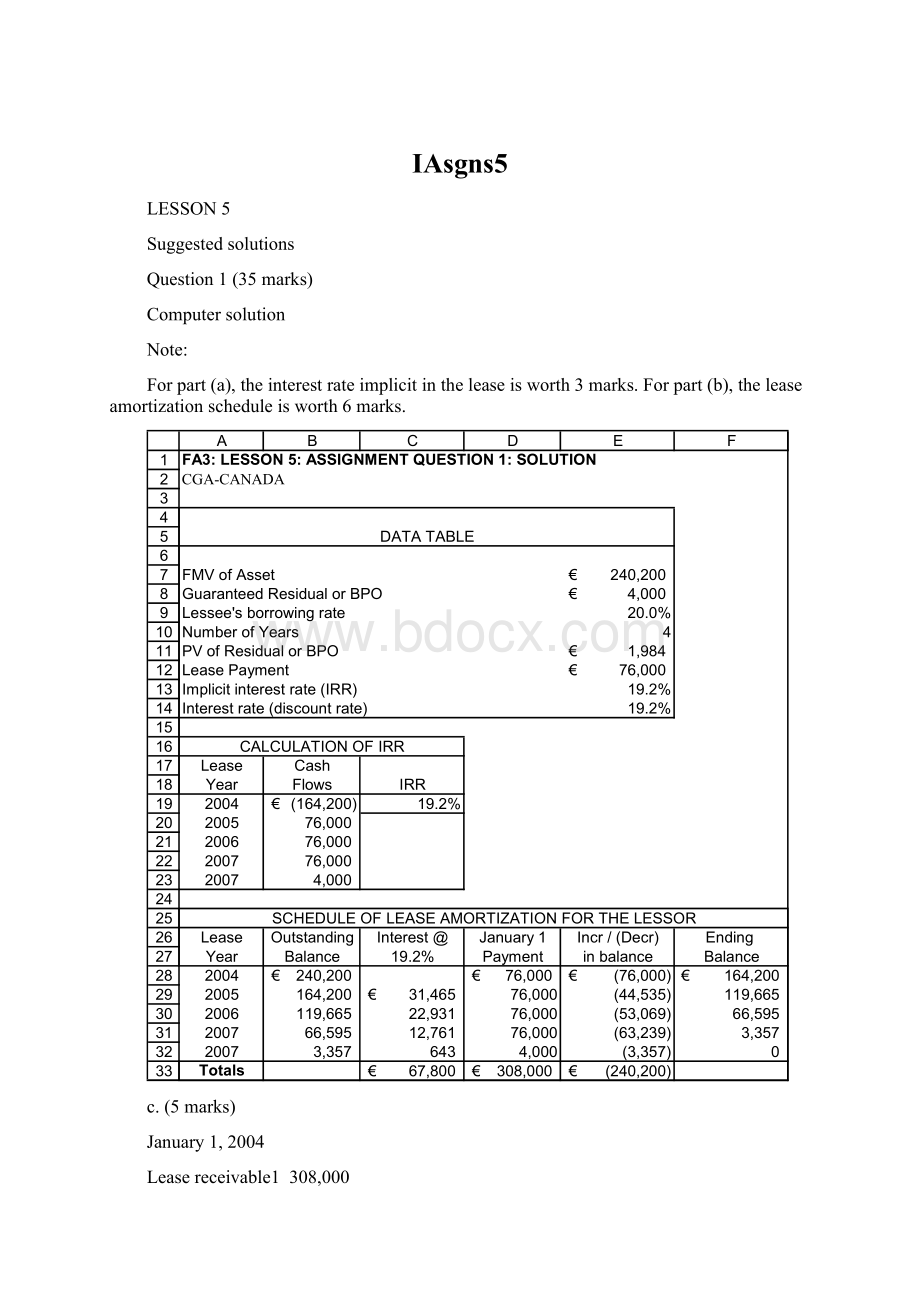

Question1(35marks)

Computersolution

Note:

Forpart(a),theinterestrateimplicitintheleaseisworth3marks.Forpart(b),theleaseamortizationscheduleisworth6marks.

c.(5marks)

January1,2004

Leasereceivable1308,000

Cash(orInventoryorMachine)240,200

Unearnedfinanceincome67,800

1(€76,0004)+€4,000

Cash76,000

Leasereceivable76,000

December21,2004

Unearnedfinanceincome31,465

Financeincome31,465

January1,2005

Cash76,000

Leasereceivable76,000

December31,2005

Unearnedfinanceincome22,931

Financeincome22,931

d.(7marks)

January1,2004

Assetunderfinancelease240,200

Leaseliability240,200

Leaseliability76,000

Cash76,000

December31,2004

Interestexpense31,465

Leaseliability31,465

Depreciationexpense(€240,200/6)40,033

Accumulateddepreciation40,033

January1,2005

Leaseliability76,000

Cash76,000

December31,2005

Interestexpense22,931

Leaseliability22,931

Depreciationexpense40,033

Accumulateddepreciation40,033

e.(8marks)

LessorLessee

Incomestatement

Interestincome22,931

Interestexpense22,931

Depreciationexpense40,033

Balancesheet

Leasereceivable(net)142,596

Leaseliability,currentportion76,000*

Leaseliability,longterm66,596*

Leasedasset240,200

Accumulateddepreciation(80,066)

*TotalliabilityatDecember31,€142,596,ofwhich€76,000isdueJanuary1,2006.

f.(2marks)

Cashflowdisclosure

Operatingactivities

Addbackdepreciation40,033

Financingactivities

Repaidleaseliability(53,069)*

*2004balance,€195,665less€142,596

g.(4marks)

Cashflowdisclosurenote

Thecompanyhasthefollowingcashcommitmentsunderfinanceleases:

Question2(14marks)

(2markseach)

a.3)

Thegainonasaleandleasebackresultinginafinanceleaseisrecognizedoverthetermofthelease,perIAS17,Paragraph50.

b.4)

The€50,000securitydepositisprepaidrentuntilthefinalyear.

c.3)

Thelesseeusestherateimplicitinthelease,unlessitisnotpracticabletodetermine.

d.3)

Theleaseisforthemajorityoftheasset’susefullife,thereforeitisafinancelease.

€100,000(PVA,10yrs,10%);€614,457rounded.

e.1)

Balanceattheendof20X4,€518,400(€608,400–€90,000)

Interestaccrualendof20X5,€51,840

Balanceattheendof20X5,€480,240(€518,400+€51,840–€90,000)

Thisisareductionof€38,160(€518,400–€480,240)

f.2)

€126,000/15;theentireusefullifeisthedepreciationperiod,sincetitlepasses.

g.4)

Inthecalculationofpresentvalueoftheminimumleasepayments,thePVofabargainpurchaseoptionisadded,so(4)iscorrect.Answer

(1)isincorrectsincethepaymentdoeshavetobecapitalized.ThePVisnotsubtracted,so

(2)isincorrect.Thepresentvalueisused,nottheexerciseamount,so(3)isincorrect.

Question3(16marks)

Requirement1(8marks)

#1#2#3

a.Leaseterm1year7years

(1)5years

b.Bargainpurchaseoptionn/a€1n/a

c.Unguaranteedresidual?

n/an/a

d.Guaranteedresidualn/an/a€75,000

e.Bargainrenewaltermsn/an/an/a

f.Minimumnetleasepayments€9,200€150,001

(2)€596,500(3)

g.Contingentleasepayments€7.40/hourn/an/a

h.Interestratetobeusedtodiscount10%8%10%

(1)RenewaltermpreceedsBPO

(2)[(€28,600–€2,600)5]+[(€11,500–€1,500)2]+€1

(3)(€104,3005)+€75,000.Thefullamountoftheguaranteedresidualisincluded.

Requirement2(4marks)

Classification

#1Operatinglease.Noneofthecriteriaforafinanceleasearemet.Thisisastraightforwardrental.

#2Financelease.Titlepasses(BPO).ThePVoftheMLPalsorepresentssubstantiallyallofthefairvalueoftheassetattheinceptionofthelease:

a)(€28,600–€2,600)(PVA,8%,5)(3.99271)€103,810

b)(€11,500–€1,500)(PVA,8%,2)(PV,8%,5)

(1.78326)(.68058)12,137

€115,947

(TheBPOhasanegligiblePV.)

#3Financelease.Theleasetermcoversthemajorpart(5/6)oftheasset’susefullife.ThisisafinanceleaseeventhoughthePVoftheMLPrepresentsonly88%ofthefairvalueoftheassetattheinceptionofthelease:

a)(€104,300)(PVAD,10%,5)(4.16987)€434,917

b)(€75,000)(PV,10%,5)(.62092)46,569

€481,486

Marker:

award1markforleases#1and#3,and2marksforlease#2.

Requirement3(4marks)

#1Maintenanceandinsuranceexpense1,400

Rentalexpense,machinery9,200

Cash10,600

Theexpensecouldallberecordedinrentalexpense

#2Assetundercapitallease115,947

Leaseliability115,947

#3Assetundercapitallease481,486

Leaseliability481,486

Leaseliability104,300

Cash104,300

Marker:

award1markforleases#1and#2,and2marksforlease#3.

Question4(15marks)

Requirement1(4marks)

Note:

MoststudentswillsolvetheIRRusingaspreadsheetprogramandmayalsocompletetheamortizationtablethisway,althoughthisisnotrequired.Ifstudentssolvetheproblemusingextrapolation,someroundingerrorsmaybepresent.Studentsshouldnotbepenalizedforthis.

Interestrateimplicitinthelease

€200,730=(€43,329–€5,200)(PVAD,x%,6)

x=5.55%(solvedbyspreadsheet)

Lessor’sAmortizationSchedule

BeginningInterestatDecreaseEnding

YearBalance5.55%PaymentinBalanceBalance

20x7€200,730€0€38,129€38,129€162,601

20x8162,6019,02438,12929,105133,496

20x9133,4967,40838,12930,721102,775

20x10102,7755,70338,12932,42670,349

20x1170,3493,90438,12934,22536,124

20x1236,1242,00538,12936,1240

€28,044

Requirement2(3marks)

Changesinprofitduetolease

Fiscal

YearProfitfromsaleFinanceIncomeTotal

20x7€50,7301€9,024€59,754

20x807,4087,408

20x905,7035,703

20x1003,9043,904

20x1102,0052,005

20x12000

Total€50,730€28,044€78,774

1Or,€200,730salesincome–€150,000costofasset.

Requirement3(8marks)

January2,20x7

Leasepaymentsreceivable((€43,329–€5,200)6)228,774

Unearnedfinanceincome28,044

Sales200,730

COGS150,000

Inventory150,000

Cash43,329

Maintenanceandinsuranceexpense5,200

Leasepaymentsreceivable38,129

Maintenanceandinsuranceexpense5,200

Cash5,200

December31,20x7

Unearnedfinanceincome9,024

Financeincome9,024

January2,20x8

Cash43,329

Maintenanceandinsuranceexpense5,200

Leasepaymentsreceivable38,129

Maintenanceandinsuranceexpense5,200

Cash5,200

December31,20x8

Unearnedfinanceincome7,408

Financeincome7,408

Question5(20marks)

Caseanalysissolution

Overview

TheleasemustbeaccountedforandreportedinaccordancewithIAS17asafinancelease.Wrightwouldbeconsideredamanufacturerordealerlessor.Sinceoutsideshareholderswillrelyonthefinancialstatements,thereisahighethicalstandardoffairpresentation.

Issues

a)Leaseclassification—financeoroperating

b)Leasepresentation—cantheleasereceivablebenettedwiththebankloanpayable?

Analysis

1.Leaseclassification

Theleaseismostlikelyafinancelease

a)Attheendoftheleaseterm,whichisnomorethan50%oftheexpectedlifeoftheairplane,thelesseecanrenewperpetuallyfor€1,000.Thiscertainlywillbeabargainrenewaloption,since

(1)theoptionisthelessee’s,whichimpliesthatWACwillhavereceivedfullcompensationfortheplanewithintheinitialleaseterm,and

(2)thenormalrentalratesforarelativelyyoungairplanewouldcertainlybemorethan€1,000peryear.Thus,itisreasonablycertainthatthelesseewouldcontinueleasingtheassetsuchthattheleasetermcoversthemajorportionoftheusefullifeoftheairplane.

b)AlthoughWACistechnicallythelessor,WACactuallyreceivesallofthemoneyupfront:

10%fromthelesseeand90%(discounted)fromthebank.Aftertheinitialtransaction,WACdoesnotparticipateintheleaseexceptasanintermediaryforthepaymentsbetweentheflyingclubandthebank.Thisisaclassicleveragedlease.Sincethelessorreceivesallthesalesvalueupfront,thisrepresentsthepresentvalueoftheminimumleasepaymentsandissubstantiallyalloffairmarketvalue.

c)Otherclassificationcriteria,titlepassing,aBPO,orspecializednatureoftheasset,arenotmet.

TheleasemustbereportedinaccordancewithIAS17asafinanceleasebyamanufacturer.Wrightwillrecordsalesrevenueintheamountofthefairvalueoftheplaneor,iflower,thenetpresentvalueoftheleasepayments,discountedattheinterestrateimplicitinthelease(assumingthisratereflectsthecommercialrate).Wrightwillalsorecognizealeasereceivableaccount.

2.Leasepresentation

Itispossibletoarguetwoapproachestopresentingthereceivableandpayable:

a)Reportthenetleasereceivableasanassetandreportthebankloanasaliability.

b)Nettheliabilityagainstthereceivable,showingonlyanynetdifferenceintheaccounts(astheresultofusingdifferentdiscountrates)asdeferredfinancingcostorincome.

Nettingthetwoamountswouldhavetheeffectofreducingthereporteddebtandassets,withthefollowingresults:

∙improvingdebt:

equityratios

∙increasingreturnonassets

∙reducinginterestchargestoincome,andtherebyimprovingthetimes-interest-earnedratio

ThismaybeadesirableresultforWrightifthecompanyhasdebtcovenants.However,itisonlyethicaltochoosethispresentationifitcorrespondstoreality:

whatisthenatureoftherelationshipbetweenWrightandthebankifacustomerdefaults?

Thesecondalternativemaybevalidinthecaseofnon-recourseleveragedleasesituations,butitisnotstatedinthecasethatthebankhasnorecoursetoWright.Thes

升级会员

升级会员