《今后25年政府债务的全球经济全景对经济政策及公共政策的启示》.docx

《《今后25年政府债务的全球经济全景对经济政策及公共政策的启示》.docx》由会员分享,可在线阅读,更多相关《《今后25年政府债务的全球经济全景对经济政策及公共政策的启示》.docx(36页珍藏版)》请在冰豆网上搜索。

《今后25年政府债务的全球经济全景对经济政策及公共政策的启示》

TheBurdenofDebtandFiscalLimits

Howmuchdebtis“sustainable”?

Ultimately,thelevelofsustainabledebtdependsnotonsomeabstractformula,butonthewillingnessofsocietyandgovernmenttopaytheinterestonthedebtandtoacceptthereductioninGDPcausedbythehigherinterestratesandhighertaxratesassociatedwithsuchaburden.Thereisnoautomaticwaytocalculatethateffectbutsomeobviouseconomicandfinancialnormsdoapply.Thefollowinganalysisseekstoapplythelessonsofhistoryforunderstandinglikelyfuturedevelopments.Wenotethatouranalysisdoesnotmakeanystrongassumptionsaboutrationalityorforesightofeitherthepublicortheprivatesector.However,thereisnoguaranteethatmarketsorgovernmentswillbehavethesameinthefutureastheydidinthepast.

债务负担和财政限制

多少债务是“合适”的?

可持续的债务水平,最终不是取决于一些抽象的公式,而是取决于社会和政府支付债务利率的意愿,及承受因高利率、高税率而导致GDP减少的意愿。

没有固定的方法能计算这些影响,但一些著名的经济金融原理可以适用。

接下来的的分析旨在吸取历史教训,更好地预测未来。

我们认识到,我们的分析没有对公有、私营行业进行任何理性或前瞻性的断定。

然而,市场或政府不能保证今后会采取以前的方法。

EffectofDebtonInterestRatesandInterestPayments

Table3andfigures7–11displayeffectiveinterestratesongovernmentdebt,bothpastandprojected.Since2006,interestrateshavefallenintheUnitedStatesandtheeuroarea,inpartbecauseoftheeconomicdownturn,whichledinvestorstobuygovernmentsecuritiesindollarsandeurosasasafehaven,andinpartbecauseofthetrendincreaseinreserveaccumulationbymanygovernmentsindevelopingeconomies.Atthesametime,rateshaveriseninJapanbecauseoftheendofthequantitativeeasingpolicy.Inthebaselinescenario,interestratesareprojectedtoequalthetrendgrowthrateofnominalGDPinalleconomiesin2015,roughlyconsistentwithhistoricalaveragebehaviorandtheassumptionthatoutputwillbenearitslong-runpotential.Thisprojectionimplicitlyassumesthatdevelopingeconomieswillslowtheirrapidpurchasesofbondsintheadvancedeconomies.

债务对利率及利息支付的影响

表3和图7---图11显示出政府债务的实际利率和预测利率。

自2006年以来,利率在美国和欧元区下跌,部分是因为经济不景气,导致投资者用美元和欧元购买政府债券作为“避风港”;还有部分原因是许多发展中国家政府外储增加。

与此同时,随着量化宽松政策的结束,日本利率上升。

基准情形下,假设GDP产量与历史平均水平一致,且达到其长期潜能,到2015年,我们预计利率将与名义GDP增长率趋于一致。

该预测无疑假定了发展中国家将放缓购买发达国家债券。

Whatissignificantisthatbeyond2015,interestratesgraduallyriseinlinewithnetdebtratios.ThecumulativeincreaseismostnotableintheUnitedStatesandJapan,whereratesareatverylowlevelsatpresent,butitisalsosignificantinEurope.Theprojectedlevelsofinterestratesin2035mayseemrathermodestgiventhelargeincreasesingovernmentdebtinsomeregions.Threefactorsexplainthismutedriseininterestrates.

2015年以后,利率上调幅度和净负债比率的密切关系将更为显著。

虽然在美国和日本,利率目前处于低水平,但利率的累积增长却最为明显,同时对欧洲也适用。

到2035年,政府债务大幅度增长的国家利率水平较为适度。

三个因素可以解释利率缓慢上升趋势。

First,andperhapsmostimportant,ourestimatesoftheeffectofgovernmentdebtoninterestratesessentiallyassumethatthereisnoriskofdefault.Thisassumptionisappropriateforgovernmentsthatborrowincurrenciestheycontrolbecausetheycanprintmoneytopaytheirdebtsinextremity.TheUnitedStates,theeuroareaasawhole,Japan,mostotheradvancedeconomies,andsomeemergingeconomiesborrowincurrenciestheycontrol.Butindividualeuro-areacountriesandmanyemergingeconomiesborrowincurrenciestheydonotcontrol;insuchcases,defaultbecomesaseriousriskwhendebtlevelsrise.Anumberofstudieshavefoundlargeeffectsofdebtoninterestratesforgovernmentsthatborrowincurrenciestheydonotcontrol.

首先,也是最重要的,在假定没有违约风险的基础上,我们就利率对政府债务的影响进行估计。

这种假设是基于,政府能借用他们所控制的货币,最终可以通过印发钞票来支付债务。

在美国、欧元区、日本、许多其他经济发达国家,还有一些新兴经济体都借用其所掌控的货币。

但是,欧元区的个别国家和许多新兴经济体借用的不是其所控制的货币;在这种情况下,当债务水平上升时,违约将成为一个严重的风险。

研究表明,当政府借用不能控制的货币时,利息对债务产生很大的影响。

23

Second,allofourscenariosassumeconstantlowinflationandstableinflationexpectations.Thereisnowayofpredictinghowfuturefiscaldevelopmentswouldaffectinflationandprices,butthebehaviorofcentralbanksoverthepast20yearssuggeststhatthereisareasonablechancethatinflationmayremainlowevenwithlargeincreasesindebt.Atsomepoint,however,increasesinthecostofservicingdebtareboundtoforcegovernmentstoresorttoinflationarymoneycreation.Ifinflationweretoincreasesignificantly,interestrateswouldsurelybeevenhigherthanprojectedhere.Buttherealrateofinterest(i.e.,thenominalinterestrateminustheexpectedinflationrate)mightmovebyanamountconsistentwiththeempiricalresultsintable3.Higherrealratesofinterestaretheprimarychannelthroughwhichgovernmentbudgetdeficitscrowdoutproductiveinvestmentandultimatelyreducethegrowthrateoftheeconomy.

其次,我们假设持续的低通货膨胀和稳定的通胀预期。

目前,无法预测财政前景会如何影响通货膨胀和价格,但央行过去20年的经验表明,即使大幅增加债务,保持低通货膨胀也是有可能的。

然而,某些时候,偿债成本的增加势必迫使政府诉诸超发货币。

如果通货膨胀大幅增长,利率会比预计高。

但是,实际利率(即名义利率减预计通货膨胀率)会有一些变化,这与表3的研究结果一致。

更高的实际利率通过政府预算赤字挤出有效投资,从而最终影响经济的增长。

图3政府债务的的有效利率(百分比)

美国

乐观增长

基线

悲观增长

悲观的健康代价

高利率

欧洲地区

同上

日本

同上

经济发达国家

同上

经济新兴国家

同上

来源:

作者的计算、2005年14期国际货币基金组织的财政数据和预测

图7美国综合政府债券的有效利率

基线

悲观增长

悲观健康

高利率

低利率

乐观增长

来源:

作者的计算、2005年14期国际货币基金组织的财政数据和预测

Thethird,andprobablyleastimportant,factoristhatinourscenariostheincreaseingovernmentdebtrestrainsthegrowthofGDP,whichholdsdowninterestrates.Thisfactorbecomessignificantonlyinthefinalfewyearsofthemoreextremescenarios.

第三,在我们的方案中,或许最不重要的因素是不断增长的政府债务抑制了GDP的增长,同时也阻止了利率的增长。

这一因素只有在出现极端情况的最后几年才会变得重要。

Table4andfigures12-16displaynetdebtInterestpaymentsasapercentofGDPineacheconomy.Exceptfortheoptimisticgrowthscenariointheeuroareaandtheemergingmarkets,interestpaymentsarerisinginalleconomiesunderallscenarios.NetdebtinterestpaymentsrisemostdramaticallyinJapan,reflectingthelargergrowthofdebtprojectedforJapan.

表4和图12-16反映了各经济体的净债务利息支出占GDP比例。

除欧元区和新兴市场乐观的增长情况外,其他各经济体利息支出是全方位不断上升的。

日本净债务利息支出上升最为明显,表明将会出现更大的债务增长。

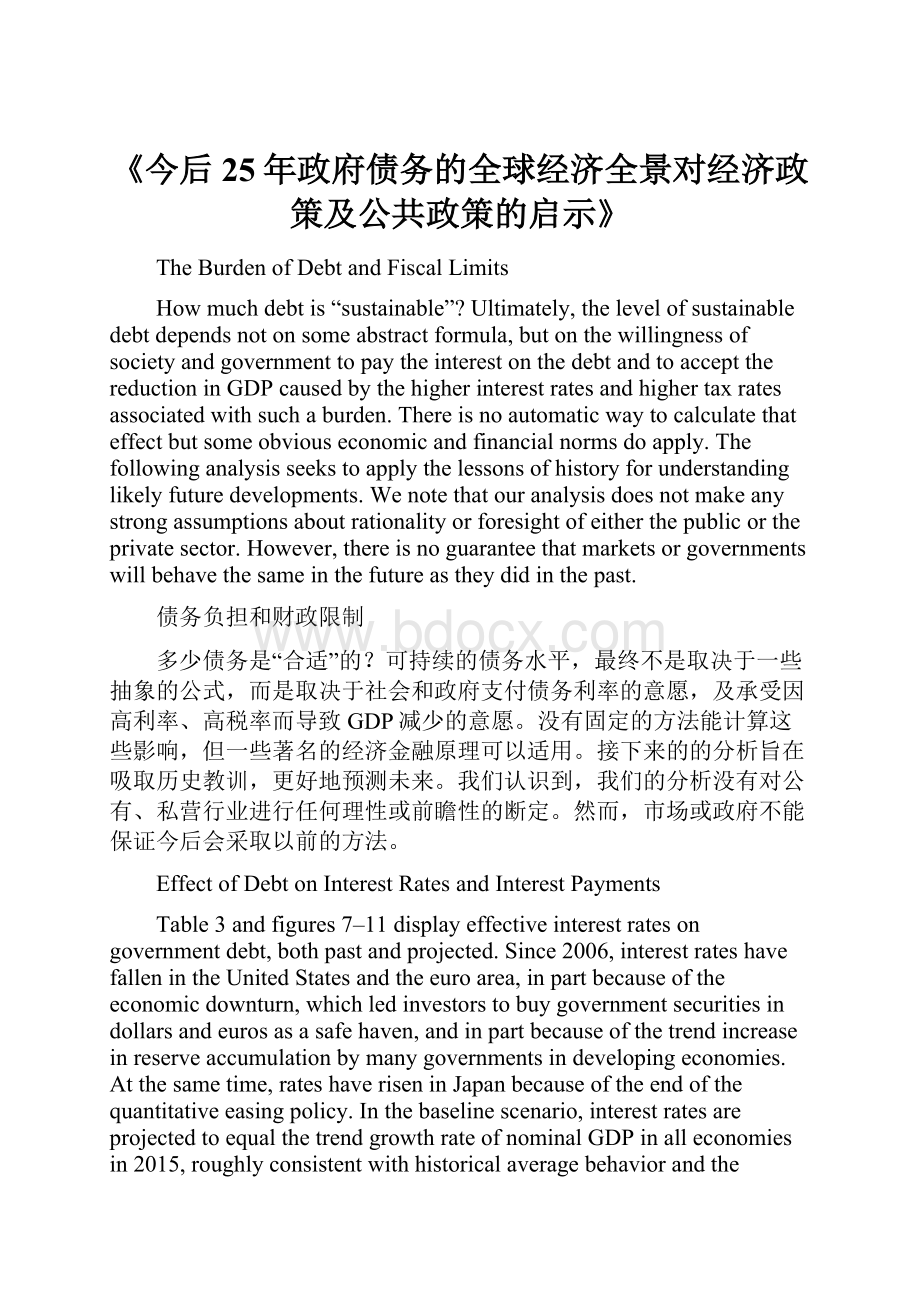

图8一般政府债务的实际利率---日本

基准线

悲观增长

悲观正常

高利率

低利率

积极增长

来源:

作者的计算和IMF(国际货币基金组织)官方预测数据2005-14。

TheLimitsofDebt

AsovereigndefaultbytheUnitedStatesoramajorcountryinEuropeisobviouslyunthinkableforpolicymakers.Nevertheless,marketscanreacttothepossibilityofsuchanoccurrenceinthelong-termfuture.Itisextremelydifficulttolaydownahardandfastruleonthelimitsofborrowing,andtheprospectfordefault,foreconomiesinthemodernera.Reinhart,Rogoff,andSavastano(2003)—intheirstudyofthehistoryofborrowinganddefaultaroundtheworld,withaparticularfocusonemergingeconomies—haveshownthateconomiesdiffersharplyinthelevelsofdebtthatgovernmentshavetoleratedwithoutdefault.Thequestionforthefutureiswhethermarketswillcontinuetobemoreworriedaboutagivenlevelofdebtinemergingeconomiesthanthesamelevelofdebtinadvancedeconomies.Inmanyemergingeconomies,thedebtratiosatwhichdefaultshaveoccurredaremuchlowerthanthedebtratiosthatmanyadvancedeconomieshavesustainedfordecades.

债务阈值

美国或欧洲主要国家的主权违约对于政策决策者来说显然是不可想象的。

不过,市场将对未来可能的违约做出反应。

在现代经济体系中,制定对借贷限制和预期违约的硬性规定是非常困难的。

莱因哈特,罗格夫和塞瓦斯丹诺(2003年)在其对世界各地特别是新兴经济体的借贷和违约历史的研究表明,在没有违约的情况下,各国政府对债务水平的容忍各不相同。

未来的问题是,在一个给定的债务水平上,与发达经济体相比,市场是否仍需更多的担忧新兴经济体。

近几十年来,许多新兴经济体的债务违约发生率远低于发达经济体。

图9一般政府债务的实际利率---欧元区

基准线

悲观增长

悲观正常

高利率

低利率

积极增长

来源:

作者的计算和IMF(国际货币基金组织)官方预测数据2005-14

Thesedifferencesin“debtintolerance”reflectthequalityofinstitutionsandthepoliticaldynamicsineacheconomy.Reinhart,Rogoff,andSavastanoarguethatchangesindebtintolerancehappenonlyslowly;theypointtoBrazilandChileasexamplesofeconomieswithrisingabilitiestobeardebt.Ofparticularinterestinlightofthisyear’sfiscalstressesinEurope,theyfindthatGreecehasthelowestdebttoleranceoftheadvancedeconomiescoveredbytheirstudy.

在“债务不耐”上的这些差异反映了各经济体的机构质量和政治动态。

莱因哈特,罗格夫和塞瓦斯丹诺认为,“债务不耐”会发生缓慢变化,巴西和智利是经济体中债务承担能力不断增强的例子。

根据对今年欧洲财政压力的的关注,他们发现希腊是发达经济体中债务容忍程度最低的。

Ostryetal.(2010)seektofindthelimitstothe“tolerance”ofdebtinasampleofadvancedeconomies.Foreachcountry,theestimatedlimitisbasedontheresponsivenessofitsfiscalpolicytopastchangesinthelevelofdebt.Notsurprisingly,countrieswitharecordofaddressingtheirpastproblemsofdeficitsanddebtsareabletorunuplargeamountsofdebtwithoutafinancialcrisis.Theresultsdiffermoderatelyacrosseconomies,butOstryetal.findthatdebtratiosofaround200percentofGDPareattheextremelimitofwhatadvancedeconomiescanexperiencewithoutbecomingdestabilized.24Theirmodel,however,assumesthatfinancialmarketstoleratethisleveldebtprimarilybecausetheyexpectgovernmentstotakeactionstoreducetheburdeninthefuture.Thus,themaximumsustainablelevelofdebtisconsidablylowerthan200percentofGDP.

奥斯特伊(2010)试图在发达经济体中寻求债务“容忍”的限额。

每个国家的债务阈值是基于财政政策对以往债务水平变化的反应基础上的。

毫无疑问,每个国家都有解决赤字和债务问题的经验,能使其能持有大量的债务而不会发生金融危机。

这些结果不同程度地适用于各经济体,但奥斯特伊等发现债务占GDP的200%左右是发达经济体维持稳定可以承受的极限。

24然而,他们的模型是假设金融市场承受这个债务水平,主要是因为他们期望政府采取行动以减少在未来的负担。

因此,最大的可持续债务水平是低于GDP的200%。

图10一般政府债务的实际利率----发达经济体

基准线

悲观增长

悲观正常

高利率

低利率

积极增长

来源:

作者的计算和IMF(国际货币基金组织)官方预测数据2005-14

Asimpletestoftheplausibilityoftheseestimateddebtlimitsistocomparethemtothehistoricalintervalswhenmaximumtemporaryandsustaineddebtratioswereincurredbutwithouttheexpectationofdefaultorhighinflation25.Oneobviouscaseofsuchtoleranceisatimeofwar.Source:

AuthorcalculationsandIMFfiscaldataandprojectionsfor2005–14.AccordingtoCBO(2010b),USfederalnetdebtpeakedatjustover100percentofGDPin1945,atthecloseofWorldWarII,andthendeclinedsteeply.AccordingtoMares(2010),UKpublicsectornetdebtpeakedatroughly250percentofGDPattheendsoftheNapoleonicWarsandWorldWarIIanddeclinedsteeplyaftereachepisode.AccordingtoReinhart(2010)theN

升级会员

升级会员