Cashflowstatement现金流量表的编制方法.docx

《Cashflowstatement现金流量表的编制方法.docx》由会员分享,可在线阅读,更多相关《Cashflowstatement现金流量表的编制方法.docx(8页珍藏版)》请在冰豆网上搜索。

Cashflowstatement现金流量表的编制方法

Issue1Disclosure:

cashflowstatements

1.Generalformatofcashflowstatement:

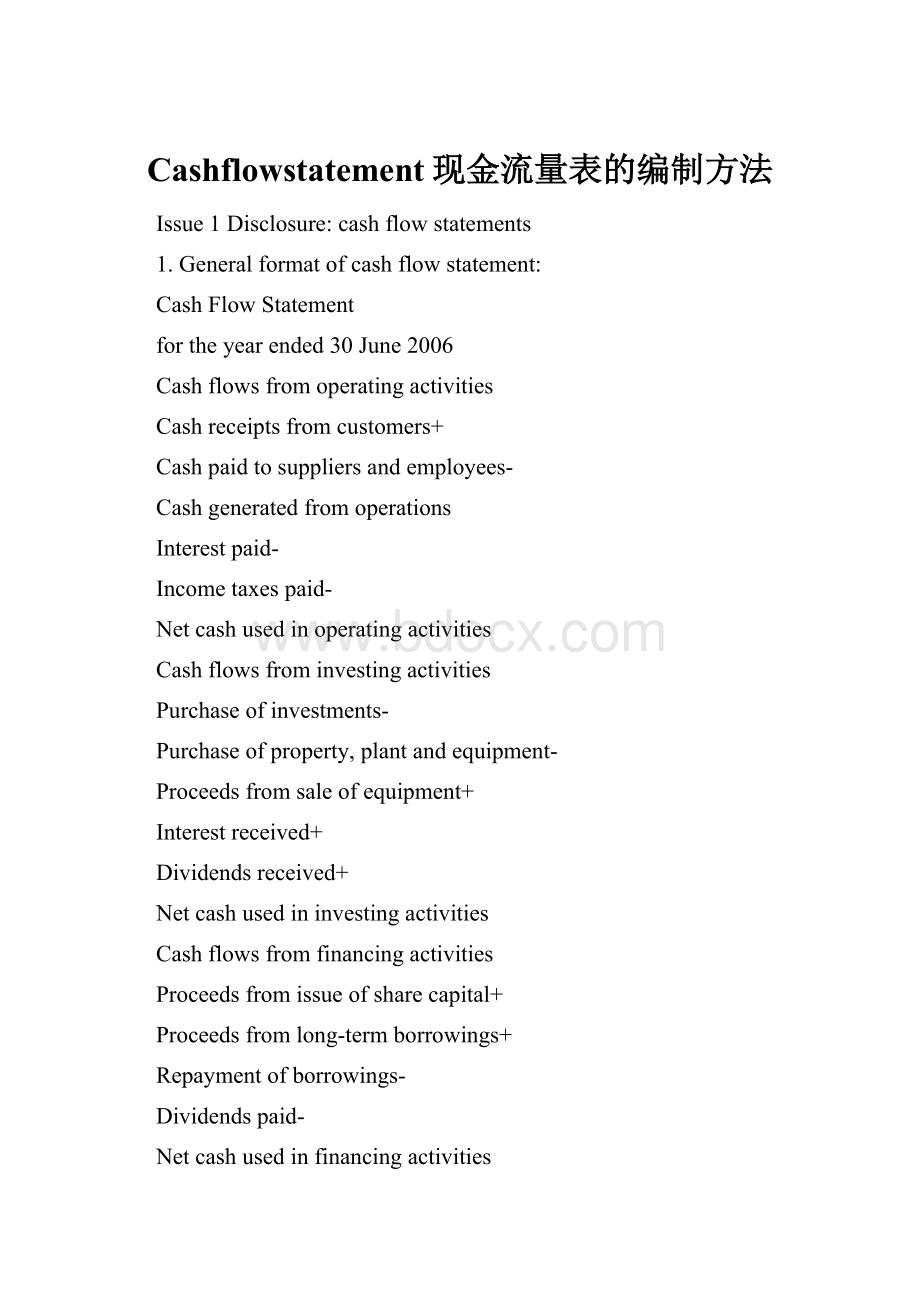

CashFlowStatement

fortheyearended30June2006

Cashflowsfromoperatingactivities

Cashreceiptsfromcustomers+

Cashpaidtosuppliersandemployees-

Cashgeneratedfromoperations

Interestpaid-

Incometaxespaid-

Netcashusedinoperatingactivities

Cashflowsfrominvestingactivities

Purchaseofinvestments-

Purchaseofproperty,plantandequipment-

Proceedsfromsaleofequipment+

Interestreceived+

Dividendsreceived+

Netcashusedininvestingactivities

Cashflowsfromfinancingactivities

Proceedsfromissueofsharecapital+

Proceedsfromlong-termborrowings+

Repaymentofborrowings-

Dividendspaid-

Netcashusedinfinancingactivities

Netincrease(decrease)incashandcashequivalents+/-

Cashandcashequivalentsatbeginningofperiod+

Cashandcashequivalentsatendofperiod+

2.Ascashflowstatementisintroduced,whatismeantbytheterm‘cash’?

Definitionofcashisimportantbecausecashcannotgeneratecashflowinthecontextofpreparingacashflowstatementandcashshouldberecordedin‘Cashandcashequivalentsatbeginningofperiod’.

Cashcomprisescashonhandanddemanddeposits.

Cashequivalentsareshort-termhighlyliquidinvestmentsthatarereadilyconvertibleintoknownamountsofcash,andwhicharesubjecttoaninsignificantriskofchangesinvalue.

Examples:

bankandnon-bankbills,moneymarketdepositsclosetomaturity,investmentwithinatermof3monthsorless.

Bankoverdraftistreatedasafinancialactivity.

Accountreceivable(subjecttoadjustmentbybaddebts)andequitysecurities(highriskinchangesinvalue)areexcludedfromthedefinitionofcash.

3.Classificationofcashflowactivities

Operatingactivities

Associatedwithrevenuesandexpenses

E.g.tolendersforinterestandborrowingcosts

Investingactivities

Associatedwithmovementinnon-currentassetsandinvestment

E.g.tosaleandpurchaseofsharesanddebentureofotherentities

Financingactivities

Associatedwithmovementinnon-currentliabilitiesandequity

E.g.toissueshares,debenture,borrowings,sharebuy-backs,dividendpaidforthecompany

(Note:

youneedtomakeclearwhetherthepaymentorreceiptisforourowncompanyorthirdparties)

4.Preparingthecashflowstatement

Step1:

Cashflowsfromoperatingactivities

Thereare2methodswhichcanbeused–directmethodandindirectmethod

Directmethodisbasedonindividualiteminincomestatement.Majorclassesofrevenuesareshownasgrosscashinflowsfromoperations,andexpensesareshownasgrosscashoutflowsfromoperations.Theinformationnecessarytodeterminetheoperatingcashflowsisobtainedbyadjustingsales,costofsalesandotheritemsintheaccrual-basisISfornon-cashitemsanditemsnotrelatedtooperatingactivities.

Underdirectmethod,eachitemisadjustedfromaccrualbasistocashbasis.Certainitems,suchasdepreciationandamortisationofnon-currentassetsandgains/lossesonnon-currentassetsdisposedof,areexcluded,becausetheyhavenoeffectoncashflow.

Indirectmethodisbasedonafter-taxprofitinincomestatement.Theaccrual-basisprofitisadjustedtoacash-basisprofitbymakingadjustmentsfornon-cashitemsusedinthedeterminationofprofit.Addedbacktoprofitaretheeffectsofalldeferralsofcashinflows(deferredincome)andoutflows(prepayment),anddeductedareallaccrualsofexpectedfuturecashinflows(accruedincome)andoutflows(accruedexpense).Thedeferralsandaccrualsoffuturecashflowsarereflectedinthechangesinthebalanceofassetsandliabilitiesrelatingtooperatingactivities.(Thismethodissimilartowhatisdoneinpreparingtax).

BothmethodsarepermittedunderIAS7.

A.Cashreceiptsfromcustomers

BeginningAccountsReceivable

+Creditsales

-Baddebtswrittenoff

-Discountallowed

=TotalAccountsReceivable

-EndingAccountsReceivable

=Cashreceiptsfromcustomers

BaddebtswrittenoffisactuallyA/RwrittenoffinUK(DrProvisionfordoubtfuldebts/CrAR)

Thepointisthebalanceoftheallowancefordoubtfuldebtsaccountmustnotbenettedoffagainsttheaccountsreceivablebalance.Wemustusebaddebtswrittenoff.

BeginningAllowance+Baddebts–Baddebtswrittenoff=EndingAllowance

Baddebtswrittenoff=BeginningAllowance+Baddebts–EndingAllowance

B.Cashpaidtosuppliersandemployees(andotherexpenses)

Forcashpaidtosuppliers:

Beginningaccountspayable

+Creditpurchases

-Discountreceived

=Totalaccountspayable

-Endingaccountspayable

=Cashpaidtosuppliers

ButcreditpurchaseisnotshowninIS.OnlycostofsalescanbeobtaineddirectlyfromIS.

COS=Beginninginventory+Creditpurchases–Endinginventory

Creditpurchases=COS–Beginninginventory+Endinginventory

Forcashpaidtoemployeesandotherservices:

Settleaccruals:

Beginningaccruals

+Accruedexpense

=Totalaccruals

-Endingaccruals

=Cashpaidforservices

Prepayment:

Beginningprepayment–Expense+Prepaidexpense(Cash)=Endingprepayment

Cashpayment=Expense+Endingprepayment–Beginningprepayment

Step2:

Cashflowsfrominvestingactivities

A.Acquisitionanddisposalofnon-currentassets

Thisstepinvolvesanexaminationofanychangesintheselong-termassetsinthelightofrelevanttransactiondatatodeterminetheeffectsoncashflows.Hence,youmustsearchthedatatocheckwhetherthecompanypurchaselong-termassetsoncashoroncreditandselllong-termassetsoncashoroncredit.

B.Interestanddividendsreceived

Beginningaccruedincome

+Interest/dividendincome

=Totalaccruedincome(Asset)

-Closingaccruedincome

=Interestanddividendsreceived

Step3:

Cashflowsfromfinancingactivities

Theinitialstepistoanalysethebalancesheetandstatementofchangesinequityforchangesinnon-currentliabilitiesandequityitems.Thesechangesarethenassessedinlightofadditionalrelevanttransactiondatatodeterminechangeswhichresultedincashflows.

Step4:

Ascertainnetcashandcashequivalentincrease/decrease

Step5:

Reconcilecashandcashequivalentatendwiththatatthebeginning

Step6:

Notetodisclosethecomponentsofcashandcashequivalents

Step7:

NotetoreconcilethenetcashusedinoperatingactivitieswithprofitintheISbyusingindirectmethod.

Thereconciliationprocesscommenceswiththeaccrual-basisprofitandadjustingforanynon-operatingitems(e.g.gains/lossesonsaleofPPE)andallnon-cashexpensesandrevenues.

Profitfortheperiod

Subtract:

Gainsonsaleofnon-currentassets(Profitfrominvestingactivities/gainsdonotaffectcash,onlysalesproceedsaffectcash)

Subtract:

Investmentincome(Interestanddividendsreceivedfrominvestingactivities)

Add:

Depreciationandotherwrite-downs(Noreductionofcash)

Add/subtract:

ChangesincurrentassetsandliabilitiesinBS(Non-currentassetsandliabilitiesrelatetoinvestmentorfinancing)

CurrentitemsinBS

+profit/cash

-profit/cash

CurrentAsset(A/R,Inventories,Prepayment)

Assetsdecrease

Assetsincrease

CurrentLiabilities(A/P,Accruals,Deferredincome)

Liabilitiesincrease

Liabilitiesdecrease

Step8:

Notestodiscussnon-cashfinancingandinvestingactivities,includingacquisitionorsaleofasubsidiaryandofproperty,plantandequipment

Why?

Sincethecashflowstatementreportsonlytheeffectsoftransactionsoncashandcashequivalents,somematerialfinancingandinvestingactivitiesmaybeomittedfromthestatementifsuchtransactionsdonotaffectcashflows.Examplesincludeconversionoflong-termdebttoequity,theacquisitionofotherentitiesbymeansofashareissue,theacquisitionofnon-currentassetsbymeansofmortgage,andtheacquisitionofassetsbyenteringintoafinancelease.

Myownthought:

Theessenceofcashflowstatementistoturntheaccrual-accountingprofittocash-accountingprofit(whichisalsonetcash).Inordertoachievethisgoal,thereare2wayswecanchoose.Thefirstwayistoadjusttheaccrual-accountingprofit,whichiscalledindirectmethod.Underindirectmethod,accrual-accountingprofitisadjustedbyreducingnon-cashexpensessuchasdepreciationexpense(whichmeansaddingittoprofit),andgain/losswhichdoesnotaffectthecashlevel.Then,weneedtoadjustthechangeofcurrentassetsandliabilities,whicharerelatedtooperatingactivities.Actually,wecansubdividetheprofit,andthiswillleadtoanothermethod–directmethod.Underthedirectmethod,theamountofcashinflowandoutflowwillbecalculated.Wecanusesales,purchasesandotherexpensetogetherwiththechangeofassetsandliabilitiestogetthecash.Cashgeneratedfromoperatingactivitiesiscloselyrelatedtocurrentassetsandcurrentliabilities;cashgeneratedfrominvestingactivitiesiscloselyrelatedtonon-currentassets;cashgeneratedfromfinancingactivitiesiscloselyrelatedtonon-currentliabilitiesandequity.

Example:

Directmethod:

Cashoutflow=BeginningA/CPayable+Purchases–ClosingA/CPayable

Indirectmethod:

Netcash=Profit+IncreaseofA/CPayable

=(Revenue–OS–Purchases+CS…)+EndingA/CPayable–OpeningA/CPayable

=…-(Purchases+OpeningA/CPayable–EndingA/CPayable

=…-theamountofcashoutflowforpurchases

Directmethod:

Cashinflow=BeginningA/CReceivable+CreditSales–EndingA/CReceivable

Indirectmethod:

Netcash=Profit–IncreaseA/CReceivable

=(Revenue-…)–(EndingA/CReceivable–BeginningA/CReceivable)

=Revenue…+BeginningA/CReceivable–EndingA/CReceivable

=Theamountofcashinflowforsal

升级会员

升级会员