AEB14SMCH24v1+GE.docx

《AEB14SMCH24v1+GE.docx》由会员分享,可在线阅读,更多相关《AEB14SMCH24v1+GE.docx(21页珍藏版)》请在冰豆网上搜索。

AEB14SMCH24v1+GE

Chapter24

AuditCompletion

ReviewQuestions

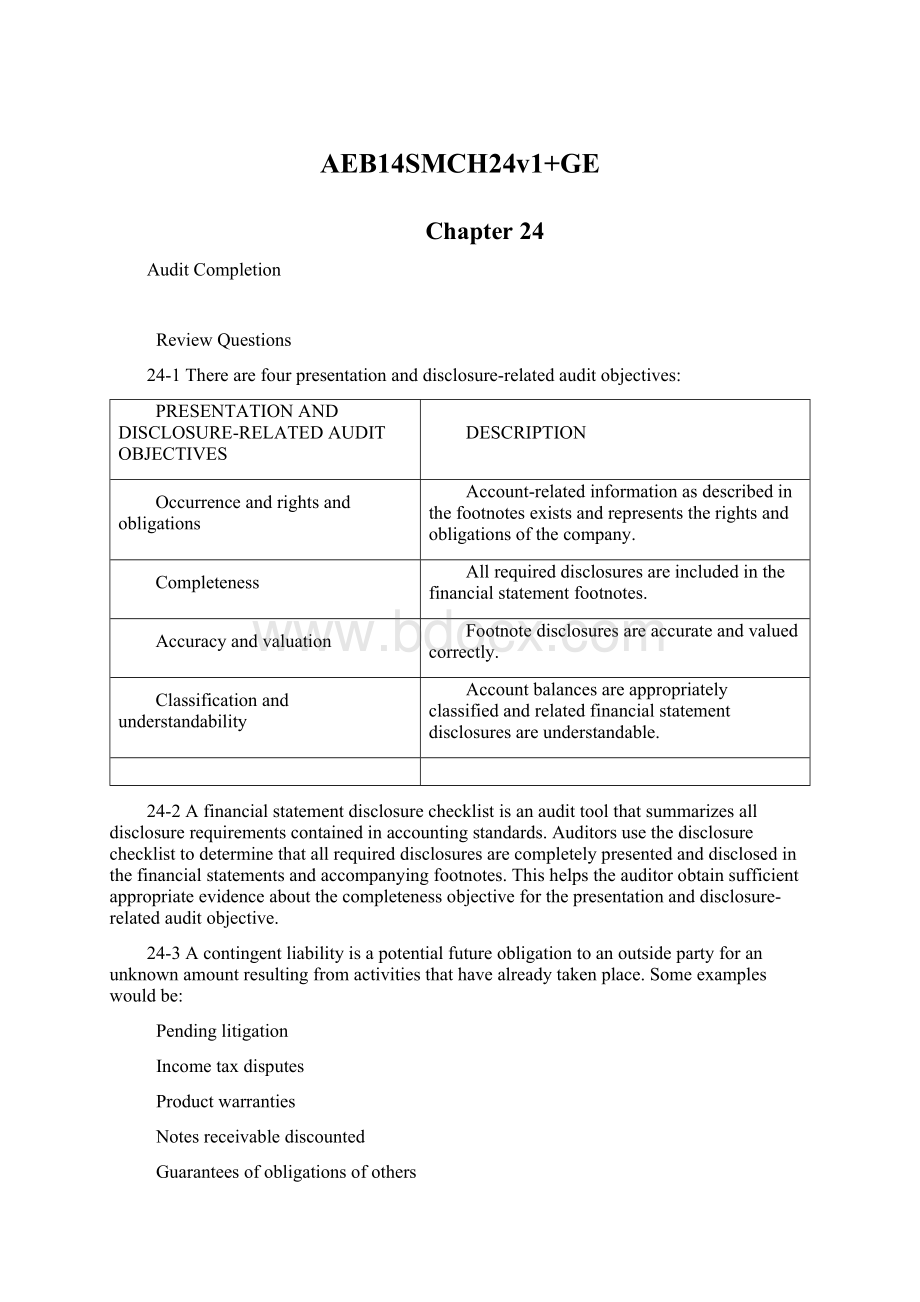

24-1Therearefourpresentationanddisclosure-relatedauditobjectives:

PRESENTATIONANDDISCLOSURE-RELATEDAUDITOBJECTIVES

DESCRIPTION

Occurrenceandrightsandobligations

Account-relatedinformationasdescribedinthefootnotesexistsandrepresentstherightsandobligationsofthecompany.

Completeness

Allrequireddisclosuresareincludedinthefinancialstatementfootnotes.

Accuracyandvaluation

Footnotedisclosuresareaccurateandvaluedcorrectly.

Classificationandunderstandability

Accountbalancesareappropriatelyclassifiedandrelatedfinancialstatementdisclosuresareunderstandable.

24-2Afinancialstatementdisclosurechecklistisanaudittoolthatsummarizesalldisclosurerequirementscontainedinaccountingstandards.Auditorsusethedisclosurechecklisttodeterminethatallrequireddisclosuresarecompletelypresentedanddisclosedinthefinancialstatementsandaccompanyingfootnotes.Thishelpstheauditorobtainsufficientappropriateevidenceaboutthecompletenessobjectiveforthepresentationanddisclosure-relatedauditobjective.

24-3Acontingentliabilityisapotentialfutureobligationtoanoutsidepartyforanunknownamountresultingfromactivitiesthathavealreadytakenplace.Someexampleswouldbe:

Pendinglitigation

Incometaxdisputes

Productwarranties

Notesreceivablediscounted

Guaranteesofobligationsofothers

Unusedbalancesofoutstandinglettersofcredit

24-3(continued)

Anactualliabilityisarealfutureobligationtoanoutsidepartyforaknownamountfromactivitiesthathavealreadytakenplace.Someexampleswouldbe:

Notespayable

Accountspayable

Accruedinterestpayable

Incometaxespayable

Payrollwithholdingliabilities

Accruedsalariesandwages

24-4Ifyouareconcernedaboutthepossibilityofcontingentliabilitiesforincometaxdisputes,therearevariousproceduresyoucoulduseforanintensiveinvestigationinthatarea.Oneapproachwouldbeananalysisofincometaxexpense.Unusualornonrecurringamountsshouldbeinvestigatedtodetermineiftheyrepresentsituationsofpotentialtaxliability.AnotherhelpfulprocedureforuncoveringpotentialtaxliabilitiesistoreviewthegeneralcorrespondencefileforcommunicationwithattorneysorIRSagents.Thismightgiveanindicationthatthepotentialforaliabilityexistseventhoughnoactuallitigationhasbegun.Finally,anexaminationofinternalrevenueagentreportsfromprioryearsmayprovidethemostobviousindicationofdisputedtaxmatters.

24-5Theauditorwouldbeinterestedinaclient'sfuturecommitmentstopurchaserawmaterialsatafixedpricesothatthisinformationcouldbedisclosedinthefinancialstatements.Thecommitmentmaybeofinteresttoaninvestorasitiscomparedtothefuturepricemovementsofthematerial.Afuturecommitmenttopurchaserawmaterialsatafixedpricemayresultintheclientpayingmoreorlessthanthemarketpriceatafuturetime.

24-6Theanalysisoflegalexpenseisanessentialpartofeveryauditengagementbecauseitmaygiveanindicationofcontingentliabilitieswhichmaybecomeactualliabilitiesinthefutureandrequiredisclosureinthecurrentfinancialstatements.Sinceanysinglecontingencycouldbematerial,itisimportanttoverifyalllegaltransactions,eveniftheamountsaresmall.Aftertheanalysisoflegalexpenseiscompleted,theattorneystowhompaymentwasmadeshouldbeconsideredforlettersofconfirmationforcontingencies(attorneyletters).

24-7PysonshoulddeterminethematerialityofthelawsuitsbyrequestingfromMerrill'sattorneysanassessmentofthelegalsituationsandtheprobableliabilitiesinvolved.Inaddition,Pysonmayhavehisownattorneyassessthesituations.Properdisclosureinthefinancialstatementswilldependontheattorneys'evaluationsoftheprobableliabilitiesinvolved.Iftheevaluationsindicatehighlyprobable,materialamounts,disclosurewillbenecessaryintheformofafootnote,assumingtheamountoftheprobablemateriallosscannotbereasonablyestimated.Iftheclientrefusestomakeadequatedisclosureofthecontingencies,aqualifiedoradverseopinionmaybenecessary.

24-8Anassertedclaimisanexistinglegalactionthathasbeentakenagainsttheclient,whereasanunassertedclaimrepresentsapotentiallegalaction.Theclient'sattorneymaynotrevealanunassertedclaimforfearthatthedisclosureofthisinformationmayprecipitatealawsuitthatwouldbedamagingtotheclient,andthatwouldotherwisenotbefiled.

24-9Ifanattorneyrefusestoprovidetheauditorwithinformationaboutmaterialexistinglawsuitsorlikelymaterialunassertedclaims,theauditopinionwouldhavetobemodifiedtoreflectthelackofavailableevidence.Thisisrequiredbyauditingstandard

升级会员

升级会员