HND财政预算OUTCOME34报告你不过我从此消失Word格式.docx

《HND财政预算OUTCOME34报告你不过我从此消失Word格式.docx》由会员分享,可在线阅读,更多相关《HND财政预算OUTCOME34报告你不过我从此消失Word格式.docx(6页珍藏版)》请在冰豆网上搜索。

Findings

PartA

(ⅰ)Flexbudgetinlinewithactualactivity

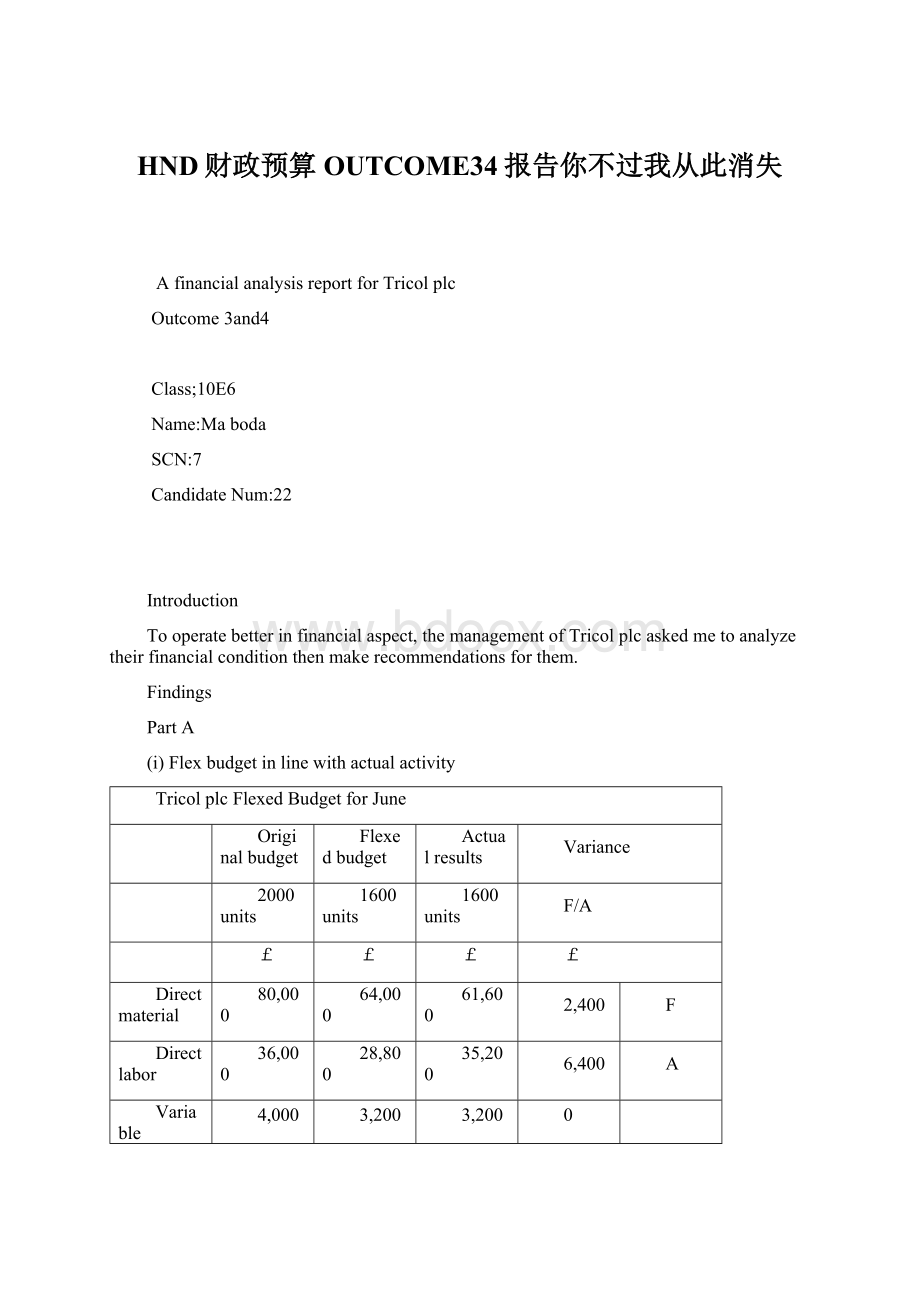

TricolplcFlexedBudgetforJune

Originalbudget

Flexedbudget

Actualresults

Variance

2000units

1600units

F/A

£

Directmaterial

80,000

64,000

61,600

2,400

F

Directlabor

36,000

28,800

35,200

6,400

A

Variableproductionoverhead

4,000

3,200

Fixedcost

Depreciation

1,500

Rentandrates

2,500

Administrationoverhead

2,000

2,200

200

Insurancecosts

Total

128,200

104,200

108,600

4,400

(ⅱ)Variancescalculation

Directmaterialtotalvariance

(Standardunitsofactualproduction*standardprice)-(actualquantity*actualprice)

(4kg*1,600*£10)-£61,600=£2,400(F)

Rateofsignificance:

%)

Directmaterialusagevariance

Standardprice*(standardunitsofactualproduction-actualquantity)

£10*[(4kgⅹ1,600)-5,600kg]=£8,000(F)

Rateofsignificance%)

Directmaterialpricevariance

Actualquantity*(standardprice-actualprice)

5,600kg*[£10-(£61,600/5,600kg)]=£(5,600)(A)

Directlabourtotalvariance

(Standardhoursofactualproduction*standardrateph)-(actualhours*actualrateph)

[(2hrs*1,600)*£9]-£35,200=£(6,400)(A)

Directlabourefficiencyvariance

Standardrateph*(standardhoursofactualproduction-actualhours)

£9*(2hrs*1,600-3,520hrs)=(2,880)(A)

(10%)

Directlabourratevariance

Actualhours*(standardrateph–actualrateph)

3,520hrs*(£9*-£35,200/3,520hrs)=£(3,520)(A)

Totaloverheadvariance

Totalstandardoverheadforactualproduction-totalactualoverheads

(£18,000/12+£2,500+£2,200+£2,000)-(£1,500+£2,500+£2,200+£2,400)=£(400)(A)

(ⅲ)Reportaboutvariances

Directmaterialvariance

Thedirectmaterialtotalvariancecanbeanalyzedintwoaspectswhicharedirectmaterialvolumeanddirectmaterialprice.

Forvolumeside,ascalculatedabove,thebudgetvolumeis6400kg;

theactualvolumeis5600kg.Sothereis800kgvariancewhichisfavorableandeachunitvarianceis.Thelikelyreasoncausingthevariancecomesfromthreeaspects.Firstofall,thecompanyupgradedtheproductionmachineryrecently,andnewmachinemayusematerialsefficiently,soitreducedthewasteofmaterials.Secondly,thecompanyswitchedsuppliersandusinghigher-gradematerialscandecreasewasteofmaterialstoo.Finally,thecompanyhasconcludedahigher-than-expectedwagesettlementforproductionoperatives,whichwillmaintainemployeeswithhigherskillsaswellasdecreaseturnoverofemployees,anditalsocanincreaseefficiencyinusingmaterials.

Forpriceaspect,thebudgetpriceis£10perkg,andtheactualpriceis£11perkg,itisadversethatonepoundoverthebudgetprice.Thecompanyswitchingsuppliersmaycausetheincreaseofnegotiationcost.Theremaybealong-termrelationshipbetweenTricolplcanditsoldsuppliers,sothesuppliersmaytakelotsofdiscountstothefirm.Afterchangingsuppliers,thediscountmaydisappear.Furthermore,highergradematerialsincreasedunitprice.

Overall,thetotalmaterialvarianceisfavorable.£8,000-£5,600=£2,400.

Directlabourvariance

Thedirectlabourtotalvarianceiscomposedofdirectlabourefficiencyvarianceanddirectlabourratevariance.

Thebudgetdirectlabourhoursare3,200hrsandtheactuallabourhoursare3,520hrs.Therearemore320hrsneededthanthebudget,andeachunitis,whichitisobviouslyadverse.Thecompanyupgradingtheproductionmachinerymayneedtimeforemployeestoadoptit.Also,employeesneedtrainingtime.Therebuildprocessofmachineryconsumedtimetoo.Inaword,thechargeablehourshaveincreased.

Thebudgetdirectlaourhoursrateis£9perhour,theactualhoursrateis£10perhour.Itisadversethatonepoundhigherthanbudgeted.Itispossiblecausedbybothinternalandexternalfactors.Higher-than-expectedwagesettlementmaybeinternalreasonforthevariance,andnewmachinerymaybeneededtorecruitnewemployeestooperatethemachinery,whichalsocanincreasetheexpense.Forexternalfactors,thechangingoflabourmarketmayincreaselabourcost;

thegovernmentlegislationalsocanincreasethelabourcost,forexampleminimumpay.

Bothdirectlabourefficiencyanddirectlabourratevariancesareadverse,sothedirectlabourtotalvarianceisadverse.

Overheadvariance

Ascalculatedabove,totaloverheadvarianceiscausedbyadministrationandinsurance.Eachfactorhas£200variance,sothetotaloverheadvarianceis£400anditisadverse.Duringtheprocessofchangingsupplier,thecompanyneededmoreexpenseonpublicrelationshipornegotiation,inaddition,inordertomaintainthenewmachinery,administrationcostwillbeincreasedtoo.Forinsuranceaside,theimprovementofmachinerywillneedmoreinsurancefeestocover,whichalsocontributestotheincreaseofinsurancefeeofnewemployees.

PartB

Selectionandapplicationoftwoinvestmentappraisaltechniques

Asthecompanyiskeentorecoupthecostoftheinvestmentwithinfiveyears,IwillchoosePaybackperiodandNetPresentValuetohelpmecompletetheappraisal.

Inordertofulfilltheappraisaleasily,therearesomeassumptionslistedbelowshouldbeconsideredbeforetheappraisal.

⑴Allrevenueandinflowareassumedcashflow

⑵Allinvestmentcostincurredinyear0

⑶Nouncertaintyisconsidered

⑷Donotconsiderinflationandtaxation

⑸Marketrateofreturnisexpectedrateofreturn

⑹Rateofreturnisvaryingalongwithtime

TricolplcPaybackperiodforprojectdistributionarm

YearNetcashflow

CumulativeCashFlow

CashFlow

Year0

(1,000,000)

CashInflow

Year1

160,000

(840,000)

Year2

(680,000)

Year3

320,000

(360,000)

Year4

(40,000)

Year5

280,000

NetCashBenefit

Note:

require40,000/320,000inyear5=1/8*year=moths

Payback=4yearsmoths

TricolplcNetPresentValueforprojectdistributionarm

Annualcashflow

Presentvaluefactorsat10%

Present

Value

145,440

132,160

240,320

218,560

198,720

935,200

NPV

(64,800)

Recommendationaboutinvestment

AccordingtoPaybackPeriodanalysis,theinvestmentcostcanberecoupedinyear4andmoths.Inotherwords,theperiodisundercompany’sexpectation.Theprojectcanbeexecuted.However,accordingtoNetPresentValueanalysis,intermsofpresentvalue,withinfiveyears,whattheNPVwillbringnetresultisnetcashlossbutnotnetcashsurplus.Ingeneral,thecompanyshouldconsidertimevalueandotherfactors,sotheprojectshouldnotbeexecuted.

Factorsimpactontheinvestmentshouldbeconsidered

Variousfactorswillimpactonresultofinvestment.Iwilloutlinefactorsshouldbeconsideredwhenthemanagementreviewingmyrecommendationinfinancialandnon-financialfactors.

Financialfactor

Asdistributionarmisfinanciallong-termbeneficialproject,itcanbeusedin

long-termperiodandbringbenefitscontinuous.Theinvestmentcostis£1,000,000,whichcanbeconsideredalargeinvestment.Soitmorelikelyneedslongperiodpaybackperiod.Themanagementshouldfocusonlongercashflowsforlongerperiodoffuture.Ontheotherhand,NetPresentValueinyearfiveis(28,000)onlytake%percentsoftheinvestmentcost,itismorelikelysurplusinyearsix.Anotherfinancialfactorissourceofmillionpounds.Ifitisinternalsource,themanagementmainlyconcentrateonopportunitiescost.Ifitiscostofcapitalorcostofcapitaltakingmuchweightofthesource,themanagementmustpaycostofthesourcefirstly,themarketingrateofreturnlikelylowforthecompany,inaddition,themanagementshouldusehigherdiscountedcashflow.

Non-financialfactor

Theinvestmentmustbeconsistencewithcompany’sstrategicplan.AsTricolisaplc,itmusttakesocialresponsibilitysuchasobeyinggovernmentpolicy,minimizingimpactonenvironmentandminimizingimpactonnatives.

Conclusion

Forrealcompetitionismorecomplexandfierce,inordertomakeaccuratedecisions,managementshouldconsidermorefactorsduringthedecision-making;

furthermore,themanagementshouldusemoretoolstohelpthemsuchasIRR,DCF.

升级会员

升级会员