会计英语课后习题参考标准答案Word文档格式.docx

《会计英语课后习题参考标准答案Word文档格式.docx》由会员分享,可在线阅读,更多相关《会计英语课后习题参考标准答案Word文档格式.docx(22页珍藏版)》请在冰豆网上搜索。

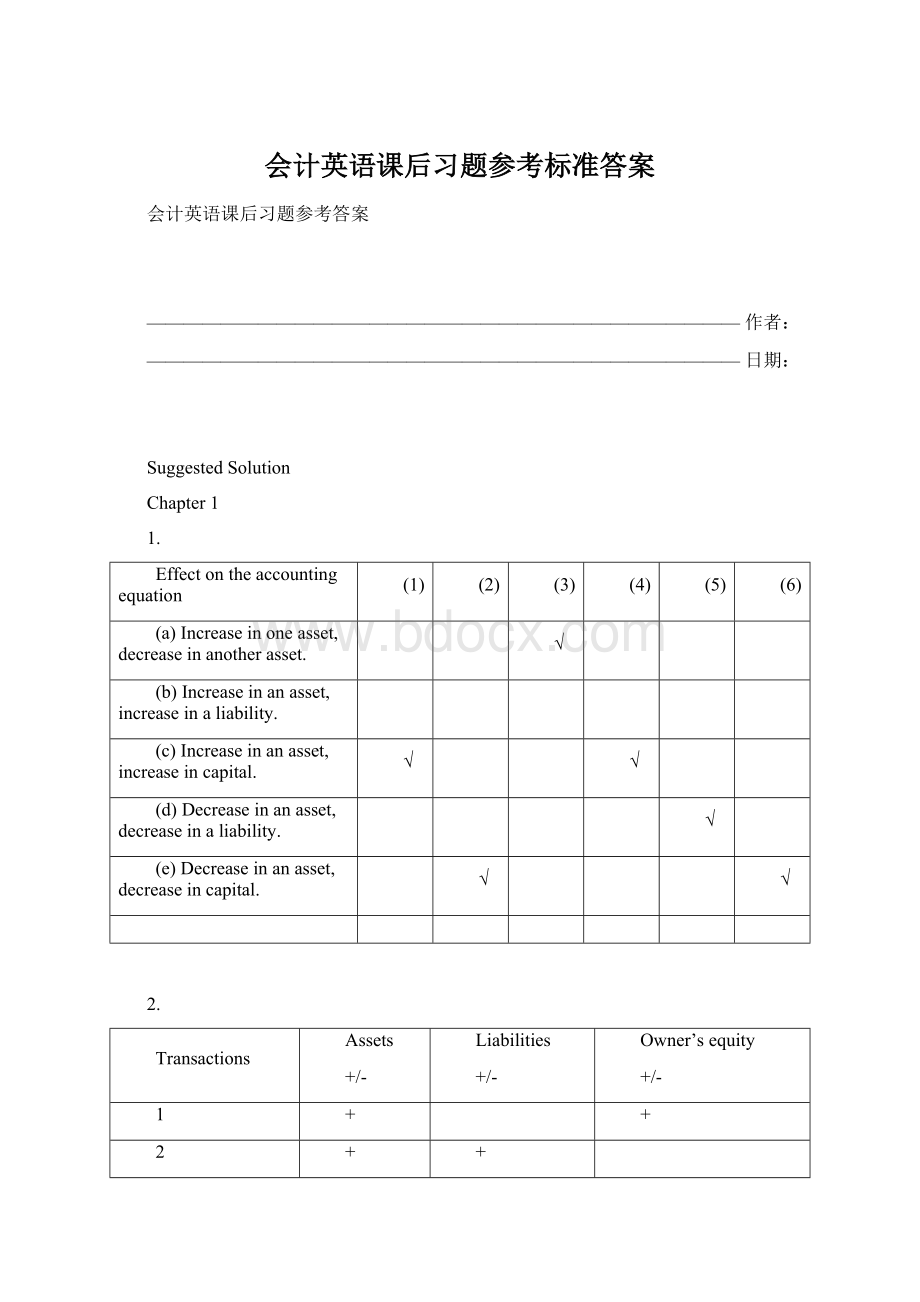

(d)Decreaseinanasset,decreaseinaliability.

(e)Decreaseinanasset,decreaseincapital.

2.

Transactions

Assets

+/-

Liabilities

Owner’sequity

1

+

2

3

-

4

5

6

7

8

9

10

3.

Describeeachtransactionbasedonthesummaryabove.

Purchasedlandforcash,$6,000.

Investmentforcash,$3,200.

Paidexpense$1,200.

Purchasedsuppliesonaccount,$800.

Paidowner’spersonaluse,$750.

Paidcreditor,$1,500

Suppliesusedduringtheperiod,$630.

4.

Equity

Beginning

275,000

80,000

195,000

Add.investment

48,000

Add.Netincome

27,000

Lesswithdrawals

-35,000

Ending

320,000

85,000

235,000

5.

(a)

March31,20XX

April30,20XX

Cash

4,500

5,400

Accountsreceivable

2,560

4,100

Supplies

840

450

Totalassets

7,900

9,950

Liabilities

Accountspayable

430

690

TinaPierce,Capital

7,470

9,260

(b)netincome=9,260-7,470=1,790

(c)netincome=1,790+2,500=4,290

Chapter2

1.

a.ToincreaseNotesPayable-CR

b.TodecreaseAccountsReceivable-CR

c.ToincreaseOwner,Capital-CR

d.TodecreaseUnearnedFees-DR

e.TodecreasePrepaidInsurance-CR

f.TodecreaseCash-CR

g.ToincreaseUtilitiesExpense-DR

h.ToincreaseFeesEarned-CR

i.ToincreaseStoreEquipment-DR

j.ToincreaseOwner,Withdrawal-DR

2.

a.

Cash

1,800

Accountspayable

b.

Revenue

Accountsreceivable

c.

Owner’swithdrawals

1,500

SalariesExpense

d.

AccountsReceivable

750

Revenue

PrepareadjustingjournalentriesatDecember31,theendoftheyear.

Advertisingexpense

600

Prepaidadvertising

Insuranceexpense(2160/12*2)

360

Prepaidinsurance

Unearnedrevenue

2,100

Servicerevenue

Consultantexpense

900

Prepaidconsultant

3,000

4.

1.$388,400

2.$22,520

3.$366,600

4.$21,800

5.

1.netlossfortheyearendedJune30,2002:

$60,000

2.DRJonNissen,Capital60,000

CRincomesummary60,000

3.post-closingbalanceinJonNissen,CapitalatJune30,2002:

$54,000

Chapter3

1.DundeeRealtybankreconciliation

October31,2009

Reconciledbalance$6,220Reconciledbalance$6,220

2.April7Dr:

Notesreceivable—Acompany5400

Cr:

Accountsreceivable—Acompany5400

12Dr:

Cash5394.5

Interestexpense5.5

Notesreceivable5400

June6Dr:

Accountsreceivable—Acompany5533

Cash5533

18Dr:

Cash5560.7

Cr:

Accountsreceivable—Acompany5533

Interestrevenue27.7

3.(a)Asawhole:

theendinginventory=685

(b)appliedseparatelytoeachproduct:

theendinginventory=625

4.Thecostofgoodsavailableforsale=endinginventory+thecostofgoods=80,000+200,000*500%=80,000+1,000,000=1,080,000

5.

(1)24,000+60,000-90,000*0.8=12000

(2)(60,000+24,000)/(85,000+31,000)*(85,000+31,000-90,000)=18828

Chapter4

1.(a)second-yeardepreciation=(114,000–5,700)/5=21,660;

(b)second-yeardepreciation=8,600*(114,000–5,700)/36,100=25,800;

(c)first-yeardepreciation=114,000*40%=45,600

second-yeardepreciation=(114,000–45,600)*40%=27,360;

(d)second-yeardepreciation=(114,000–5,700)*4/15=28,880.

2.(a)weighted-averageaccumulatedexpenditures(2008)=75,000*12/12+84,000*9/12+180,000*8/12+300,000*7/12+100,000*6/12=483,000

(b)interestcapitalizedduring2008=60,000*12%+(483,000–60,000)*10%=49,500

3.

(1)depreciationexpense=30,000

(2)bookvalue=600,000–30,000*2=540,000

(3)depreciationexpense=(600,000–30,000*8)/16=22,500

(4)bookvalue=600,000–30,000*8–22,500=337,500

4.Situation1:

Jan1st,2008InvestmentinM260,000

Cash260,000

June30Cash6000

Dividendrevenue6000

Situation2:

January1,2008InvestmentinS81,000

Cash81,000

June15Cash10,800

InvestmentinS10,800

December31InvestmentinS25,500

InvestmentRevenue25,500

5.a.December31,2008InvestmentinK1,200,000

Cash1,200,000

June30,2009DividendReceivable42,500

DividendRevenue42,500

December31,2009Cash42,500

DividendReceivable42,500

b.Decembe

升级会员

升级会员