管理会计作业答案.docx

《管理会计作业答案.docx》由会员分享,可在线阅读,更多相关《管理会计作业答案.docx(42页珍藏版)》请在冰豆网上搜索。

管理会计作业答案

MA

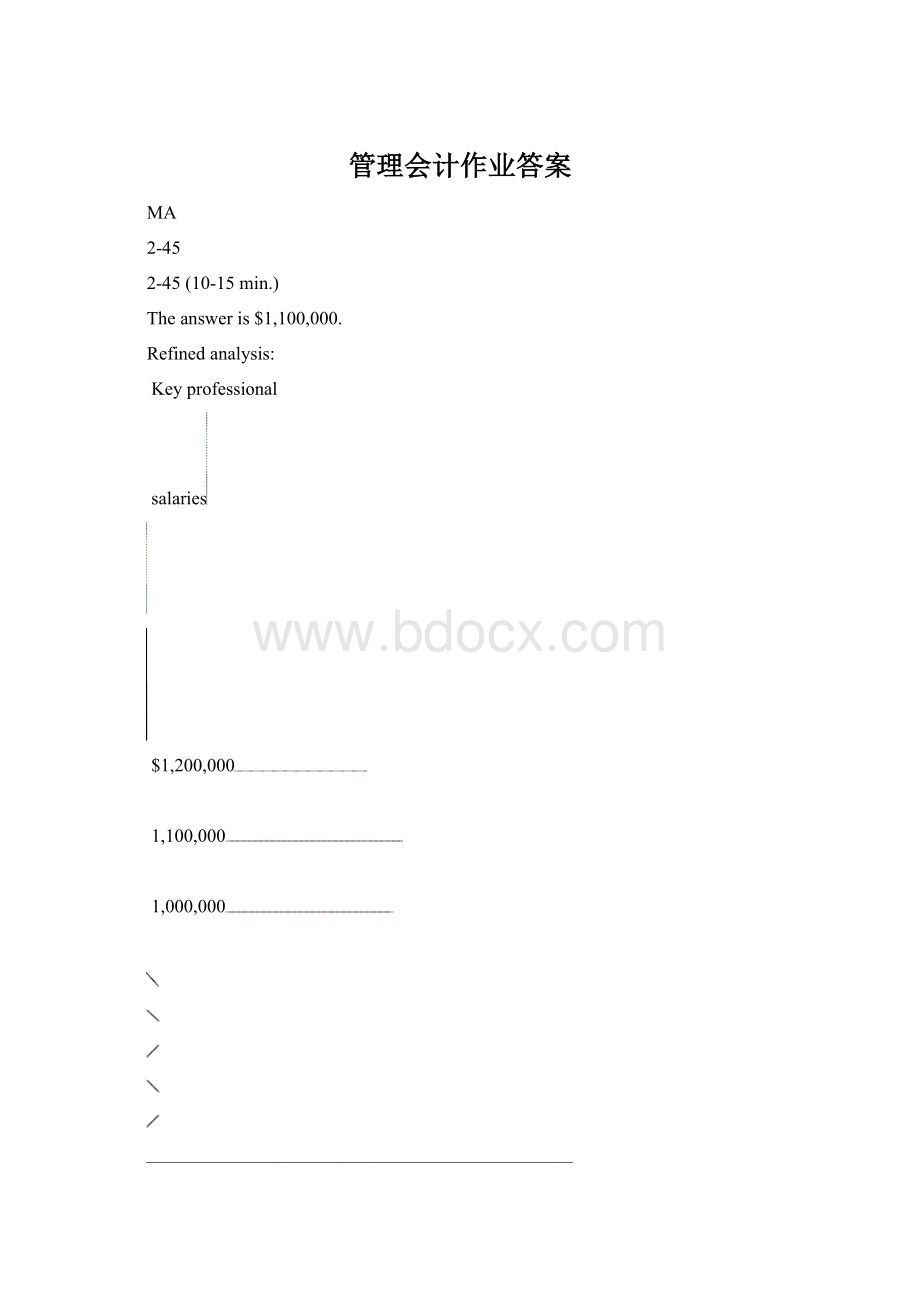

2-45

2-45(10-15min.)

Theansweris$1,100,000.

Refinedanalysis:

Keyprofessional

salaries

$1,200,000

1,100,000

1,000,000

$2,000,000$2,400,000Billings

Practicalanalysis:

Keyprofessional

salaries

$1,200,000

1,100,000

1,000,000

$2,000,000$2,400,000Billings

RelevantRange

2-64

2-64(25-35min.)

1.

=15,000patient-days

2.Variablecosts=

=$220perpatient-day

Contributionmargin=$810-$220=$590perpatient-day

Torecoupthespecifiedfixedexpenses:

$5,900,000÷$590=10,000patient-days

3.Thefixedcostlevelsdifferastherelevantrangechanges:

Non-NursingNursingTotal

Patient-DaysFixedExpensesFixedExpensesFixedExpenses

10,000-12,000$5,900,000$1,350,000(a)$7,250,000

12,001-16,0005,900,0001,575,000(b)7,475,000

(a)$45,000×30=$1,350,000

(b)$45,000×35=$1,575,000

Tobreakevenonalowerleveloffixedcosts:

$7,250,000÷$590=12,288patient-days

Thisanswerexceedsthelower-levelmaximum;therefore,thisanswerisinfeasible.Thedepartmentmustoperateata$7,475,000leveloffixedcoststobreakeven:

$7,475,000÷$590=12,669patient-days.

3-50

(1)

3-50(10-15min.)

1.Variablecost/unit=($1,131-$649)(136-71)=$48265=$7.4154

Fixedcost=$1,131-(136×7.4154)=$1,131-$1,008.49=$122.51

Predictedcostfor510units=($122.51×4)+(510×$7.4154)=$4,271.89

Noticethatthedataarequarterlyobservations.Thus,theannualfixedcostis4timesthecomputed(quarterly)fixedcost.

2.Predictedcostfor510units=($355×4)+(510×$5.77)=$4,362.70

3.Theregressionanalysisgivesbettercostestimatesbecauseitusesallthedatatoformacostfunction.Thetwopointsusedbythehigh-lowmethodmaynotberepresentativeofthegeneralrelationbetweencostsandvolume.

3A1

3-A1(20-25min.)Someoftheseanswersarecontroversial,andreasonablecasescanbebuiltforalternativeclassifications.Classdiscussionoftheseanswersshouldleadtoworthwhiledisagreementsaboutanticipatedcostbehaviorwithregardtoalternativecostdrivers.

1.(b)Discretionaryfixedcost.

2.(e)Stepcost.

3.(a)Purelyvariablecostwithrespecttorevenue.

4.(a)Purelyvariablecostwithrespecttomilesflown.

5.(d)Mixedcostwithrespecttomilesdriven.

6.(c)Committedfixedcost.

7.(b)Discretionaryfixedcost.

8.(c)Committedfixedcost.

9.(a)Purelyvariablecostwithrespecttocasesof7-Up.

10.(b)Discretionaryfixedcost.

11.(b)Discretionaryfixedcost.

4-45

4-45(20-30min.)

Thisproblemprovidesanoverviewofcostaccumulationandallocationwithoutgettingboggeddownintheintricaciesofbookkeeping.SomeinstructorsmayprefertoassigntheprobleminconjunctionwithChapter13.Inparticular,notethatthecomplicationofunder-andover-appliedoverheadisavoidedinChapter4.Forafullerdiscussion,seeChapter13.

1.Amountsareindollars.

MachiningFinishingTotal

Directmaterial140,000*60,000200,000

Directlabor25,000**50,00075,000

Indirectproduction38,00042,00080,000

Total203,000152,000355,000

*70%×$200,000

**33.333%×$75,000

2.Amountsareindollars.Sigma

DirectDirectIndirect

MaterialLaborProduction

Machining56,000*7,500*11,400*

Finishing20,000**20,000**16,800**

Totals76,00027,50028,200

*40%×$140,000;30%×$25,000;30%×$38,000

**1/3×$60,000;40%×$50,000;40%×$42,000

Chi

DirectDirectIndirect

MaterialLaborProduction

Machining42,000*7,500*11,400*

Finishing20,000**20,000**16,800**

Totals62,00027,50028,200

*30%×$140,000;30%×$25,000;30%×$38,000

**1/3×$60,000;40%×$50,000;40%×$42,000

Delta

DirectDirectIndirect

MaterialLaborProduction

Machining42,000*10,000*15,200*

Finishing20,000**10,000**8,400**

Totals62,00020,00023,600

*30%×$140,000;40%×$25,000;40%×$38,000

**1/3×$60,000;20%×$50,000;20%×$42,000

TotalCosts:

Sigma(76,000+27,500+28,200)=$131,700

Chi(62,000+27,500+28,200)=117,700

Delta(62,000+20,000+23,600)=105,600

Accountedfor$355,000

5-42

5-42(15min.)

1.Assumingthattotalfixedcostsarethesameatproductionlevelsof6,000and10,000units,theanalysiscanfocusoncontributionmargins:

CM@$12.50:

6,000units×($12.50-$6)=$39,000

CM@$10:

10,000units×($10-$6)=$40,000

Profitswillbe$40,000-$39,000=$1,000higheratthe$10price.

2.Subjectivefactorsincludeimageinthemarketplace(higherpricemaygiveanimageofquality),marketpenetration(satisfiedcustomersmaybecomerepeatcustomers),andeffectsonthesalesforce.

5-48

5-48(25-35min.)

1.LAGRANDECORPORATION

ContributionIncomeStatement

For2009

(InmillionsofEuros)

Sales€900

Lessvariableexpenses:

Manufacturingcostofgoodssold€300

Sellingandadministrativeexpenses140440

Contributionmargin460

Lessfixedexpenses:

Manufacturingcosts280

Sellingandadministrativeexpenses60340

Operatingincome€120

2.(a)Sales:

€900×90%×130%€1,053

Variableexpenses:

€440×130%572

Contributionmargin481*

Fixedexpenses340

Operatingincome€141

*Alternativecomputationofcontributionmargin:

Salesaftera10%reductioninprices:

€900×90%€810

Variableexpenses440

Contributionmarginbeforevolumechange370

Add30%of€370111

Estimatednewcontributionmargin€481

(b)Contributionmargin:

€460×110%€506

Fixedexpenses:

€340+30370

Operatingincome€136

(c)Sales€900

Variableexpenses:

Manufacturing:

€300×85%€255

Sellingandadministrative140395

Contributionmargin505

Fixedexpenses:

€340+€80420

Operatingincome€85

(d)Sales:

€900×120%×105%€1,134

Variableexpenses:

Manufacturing:

€300×120%€360

Sellingandadministrative:

€140×120%×125%210570

Contributionmargin564**

Fixedexpenses:

Manufacturing€280

Sellingandadministrative:

€60×2120400

Operatingincome€164

**Alternatecomputationofcontributionmargin:

Salesaftera5%increaseinprices:

€900×105%€945

Variableexpenses:

Manufacturing€300

Sellingandadmin.aftera25%

increaseinunitcosts:

€140×125%175475

Contributionmarginbefore

volumechange470

Add20%of€47094

Estimatednewcontributionmargin€564

(e)Thesecomputationsaregoodexamplesof"sensitivityanalysis"--testingvariousinputstoamodeltomeasuretheeffectsonestimatedoutputs.Thisisaplanningprocedure.Animportantpointtomakewithstudentsisthatthecontributionformofincomestatementismuchmoreappropriateforthesepurposesthantheabsorptionform.

Theanalysisisreadilycalculatedbyusingdatafromthecontributionincomestatement.Incontrast,thedataintheabsorptionincomestatementmustbeanalyzedandsplitintovariableandfixedcategoriesbeforetheeffectonoperatingincomecanbeestimated.

3.Alternative(c)isclearlyundesirablebecauseitproduceslessoperatingincomethanthestatusquo.Alternatives(a),(b)or(d)wouldbebetterthanthestatusquo.However,ifthesealternativescannotbeundertakensimultaneously,andifthereisnosubjectivereasontofavoralternatives(a)or(b),alternative(d)seemsbest.Itproduces€164–€141=€23(or23millionEuros)moreoperatingincomethanthenextbestalternative(a).

5-63

5-63(10–15min.)

1.Capacityisnotsufficienttoacceptbothorders,butthereisenoughcapacitytoaccepteithertheNordstromortheMacy’sorder.Thereisexcesscapacityfor150,000shoes,butthetwoorderstogetherwouldrequireproductionof90,000+75,000=165,000shoes.

NordstromMacy’s

OrderOrder

Revenue$136.00$130.00

VariableCosts:

DirectMaterials49.0049.00

DirectLabor22.0022.00

Var.FactoryOH14.0014.00

Packaging3.502.00

Contributionmargin$47.50$43.00

Unitsales×75,000×90,000

Totalcontributionmargin$3,562,500$3,870,000

Basedontheanalysisabove,acceptingtheMacy’sorderistheoptimaldecision,generatinganadditionalcontributionmarginof$3,870,000overnotacceptingaspecialorder,andanadditional$307,500incontributionmarginrelativetotheNordstromorder.

2.Someconsiderationswouldinvolvecannibalizationofexistingsalesbylowerprices,andwhethervariableandfixedcostdistinctionsremainvalidwithintherelevantrange(especiallyasmaximumcapacityisapproached).

6B3

6-B3(15-20min.)

AllamountsareinthousandsofBritishpounds.

Themajorlessonisthataproductthatshowsanoperatinglossbasedonfullyallocatedcostsmayneverthelessbeworthkeeping.Why?

Becauseitmayproduceasufficientlyhighcontributiontoprofitsothatthefirmwouldbebetteroffwithitthananyotheralternative.

Theemphasisshouldbeontotals:

ReplaceMagicDepartmentWith

ExistingGeneral

OperationsMerchandiseElectronicProducts

Sales6,000-600+250=5,650-600+200=5,600

Variableexpenses4,090-390+175a=3,875-390+100b=3,800

Contributionmargin1,910-210+75=1,775-210+100=1,800

Fixedexpenses1,100-120+0=980-120+30=1,010

Operatingincome810-90+75=795-90+70=790

a(100%-30%)×250

b(100%-50%)×200

Thefactsasstatedindicatethatthemagicdepartmentshouldnotbeclosed.First,thetotaloperatingincomewoulddrop.Second,fewercustomerswouldcometothestore,sosalesinotherdepartmentsmaybeaffectedadversely.

6-37

6-37(10min.)

ProductMshouldnothavebeenprocessedfurther.Theonlyvalidapproachistoconcentrateontheseparablecostsandrevenu

升级会员

升级会员