国际金融答案.docx

《国际金融答案.docx》由会员分享,可在线阅读,更多相关《国际金融答案.docx(55页珍藏版)》请在冰豆网上搜索。

国际金融答案

1、V.AnswerstoEndofChapterQuestions

1.Debitsarereportedasnegativevalueswhilecreditsarereportedaspositivevalues.

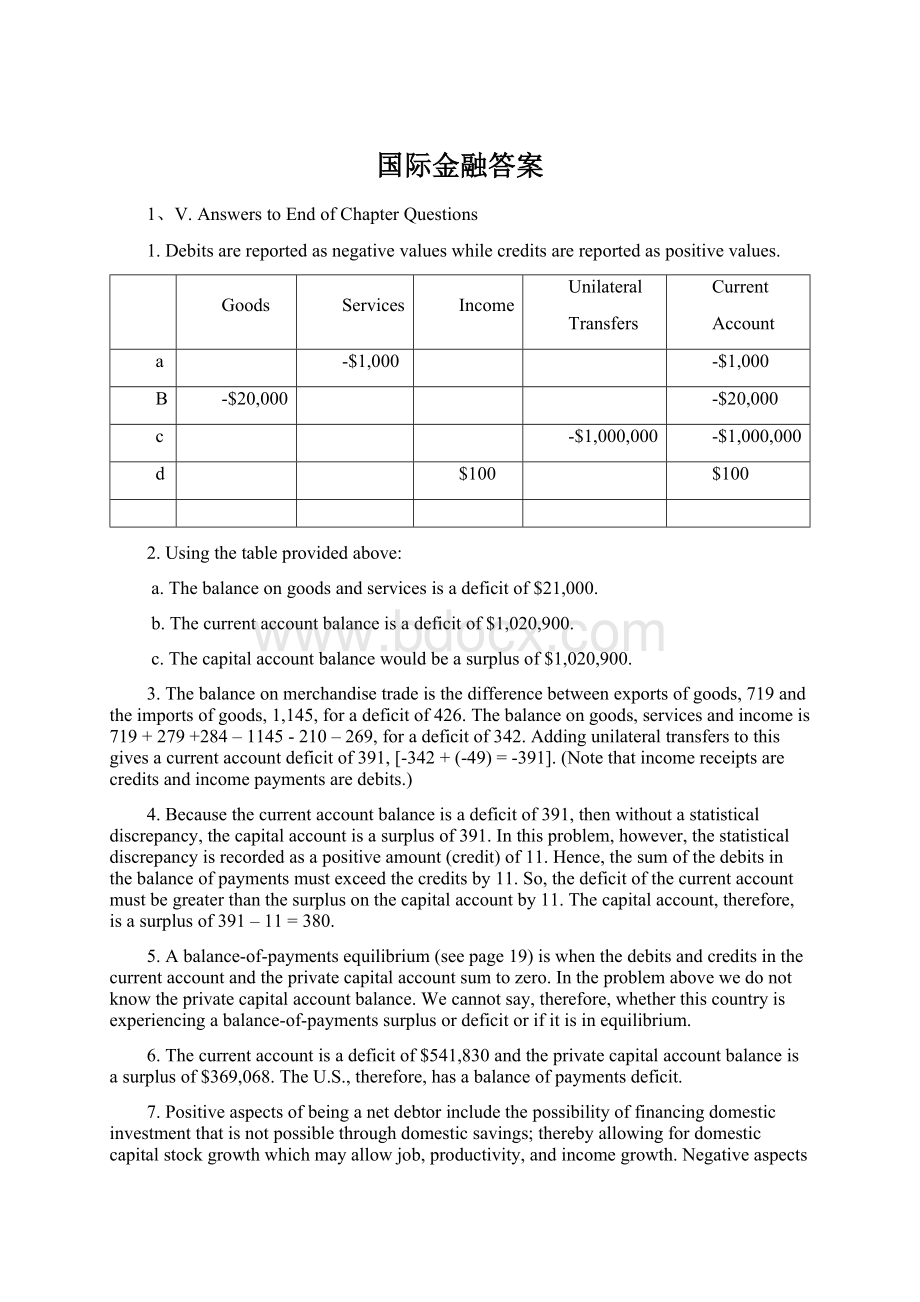

Goods

Services

Income

Unilateral

Transfers

Current

Account

a

-$1,000

-$1,000

B

-$20,000

-$20,000

c

-$1,000,000

-$1,000,000

d

$100

$100

2.Usingthetableprovidedabove:

a.Thebalanceongoodsandservicesisadeficitof$21,000.

b.Thecurrentaccountbalanceisadeficitof$1,020,900.

c.Thecapitalaccountbalancewouldbeasurplusof$1,020,900.

3.Thebalanceonmerchandisetradeisthedifferencebetweenexportsofgoods,719andtheimportsofgoods,1,145,foradeficitof426.Thebalanceongoods,servicesandincomeis719+279+284–1145-210–269,foradeficitof342.Addingunilateraltransferstothisgivesacurrentaccountdeficitof391,[-342+(-49)=-391].(Notethatincomereceiptsarecreditsandincomepaymentsaredebits.)

4.Becausethecurrentaccountbalanceisadeficitof391,thenwithoutastatisticaldiscrepancy,thecapitalaccountisasurplusof391.Inthisproblem,however,thestatisticaldiscrepancyisrecordedasapositiveamount(credit)of11.Hence,thesumofthedebitsinthebalanceofpaymentsmustexceedthecreditsby11.So,thedeficitofthecurrentaccountmustbegreaterthanthesurplusonthecapitalaccountby11.Thecapitalaccount,therefore,isasurplusof391–11=380.

5.Abalance-of-paymentsequilibrium(seepage19)iswhenthedebitsandcreditsinthecurrentaccountandtheprivatecapitalaccountsumtozero.Intheproblemabovewedonotknowtheprivatecapitalaccountbalance.Wecannotsay,therefore,whetherthiscountryisexperiencingabalance-of-paymentssurplusordeficitorifitisinequilibrium.

6.Thecurrentaccountisadeficitof$541,830andtheprivatecapitalaccountbalanceisasurplusof$369,068.TheU.S.,therefore,hasabalanceofpaymentsdeficit.

7.Positiveaspectsofbeinganetdebtorincludethepossibilityoffinancingdomesticinvestmentthatisnotpossiblethroughdomesticsavings;therebyallowingfordomesticcapitalstockgrowthwhichmayallowjob,productivity,andincomegrowth.Negativeaspectsincludethefactthatforeignsavingsmaybeusedtofinancedomesticconsumptionratherthandomesticsavings;whichwillcompromisethegrowthsuggestedabove.

Positiveaspectsofbeinganetcreditorincludetheownershipofforeignassetswhichcanrepresentanincomeflowstothecreditingcountry.Further,thenetcreditorpositionalsoimpliesanetexportingposition.Anegativeaspectofbeinganetcreditorincludesthefactthatforeigninvestmentmaysubstitutefordomesticinvestment.

8.Anationmaydesiretoreceivebothportfolioanddirectinvestmentduetothetypeofinvestmenteachrepresents.Portfolioinvestmentisafinancialinvestmentwhiledirectinvestmentisdominatedbythepurchaseofactual,real,productiveassets.Totheextentthatacountrycanbenefitbyeachtypeofinvestment,itwilldesirebothtypesofinvestment.Further,portfolioinvestmenttendstobeshort-runinnature,whileFDItendstobelong-runinnature.ThisisalsoaddressedinmuchgreaterdetailinChapter7.

9.DomesticSavings-DomesticInvestment=CurrentAccountBalance

DomesticSavings-DomesticInvestment=NetCapitalFlows

Therefore,CurrentAccountBalance=NetCapitalFlows

10.Usingtheequationsabove,privatesavingsof5percentofincome,governmentsavingsof-1percent,andinvestmentexpendituresof10percentwouldresultsinacurrentaccountdeficitof6percentofincomeandacapitalaccountsurplus(netcapitalinflows)of6percentofincome.Thiscouldbecorrectedwithareductioninthegovernmentdeficit(toasurplus)and/oranincreaseinprivatesavings.

11.ThetransnationalityindexforWorldFilmsis:

(533/1233+227/615+322/1256)/3=(0.432+0.369+0.256)/3=1.057/3=0.352.

ThetransationalityindexforMusicPublishersWorldwideis:

(455/2456+246/809+900/2467)/3=(0.185+0.304+0.365)/3=0.854/3=0.285.

Basedonthisindex,Worldfilmsisthemostglobalizedfirm.

2、V.AnswerstoEndofChapterQuestions

1.Becauseitcostsfewerdollarstopurchaseaeuroaftertheexchangeratechange,theeurodepreciatedrelativetothedollar.Therateofdepreciation(inabsolutevalue)was[(1.2168–1.2201)/1.2201]100=0.27percent.

2.Ifwetaketheinverseofeachrate,theformulaprovidedinthequestionsbecomes:

Returningtothetableonpage37,thepoundappreciationis:

[(0.5511–0.5501)/0.5501]*100=0.18,whichisthesamevaluederivedonpage39.

3.NotethattheratesprovidedaretheforeigncurrencypricesoftheU.S.dollar.Everyvaluehasbeenroundedtotwodecimalplaceswhichmaycausesomedifferencesinanswers.

A$

£

C$

Sfr

$

Australia

-

2.35

1.06

1.12

1.53

Britain

0.42

-

0.45

0.47

0.65

Canada

0.95

2.23

-

1.06

1.45

Switzerland

0.90

2.11

0.94

-

1.37

UnitedStates

0.65

1.54

0.69

0.73

-

4.Thecrossrateis1.702/1.234=1.379(€/£),whichissmallerinvaluethanthatobservedintheLondonmarket.Thearbitrageurwouldpurchase£587,544($1,000,000/1.702)withthe$1millionintheNewYorkmarket.Nexttheywouldusethe£587,544inLondontopurchase€837,250(£587,544*1.425).Finally,theywouldsellthe€837,250intheNewYorkmarketfor$1,033,167(€837,250*1.234).Theprofitis#33,167.

5.Totaltradeis(163,681+160,829+261,180+210,590)=796,280.TradewiththeEuroareais(163,681+261,180)=424,861.TradewithCanadais(160,829+210,590)=371,419.Theweightassignedtotheeurois424,861/796/280=0.53andtheweightassignedtotheCanadiandollaris0.47.(Recalltheweightsmustsumtounity.)

Becausethebaseyearis2003,the2003EERis100.Thevalueofthe2004EERis:

[(0.82/0.88)•0.53+(1.56/1.59)•0.47]•100=(0.4939+0.4611)•100=95.4964,or95.5.Thisrepresentsa4.5percentdepreciationoftheU.S.dollar.

6.Therealeffectiveexchangerate(REER)for2003isstill100.Therealratesofexchangeare,for2003,0.88•(116.2/111.3)=.9187,1.59•(116.2/111.7)=1.6541,andfor2004,0.82•(119.0/114.4)=0.8530,1.56•(119.0/115.6)=1.6059.Thevalueofthe2004REERis:

[(0.8530/0.9187)•0.53+(1.6059/1.6541)•0.47]•100=(0.4921+0.4563)•100=94.84,or94.8.Thisrepresentsa5.2percentdepreciationoftheU.S.dollarinrealterms

7.ThisisanominalappreciationoftheeurorelativetotheU.S.dollar.Thepercentchangeis[(1.19–1.05)/1.05]•100=13.3percent.

8.TheJanuary200realexchangerateis1.05•(107.5/112.7)=1.0016.TheMay2004realrateis1.19•(116.4/122.2)=1.1335.

9.InrealtermstheeuroappreciatedrelativetotheU.S.dollar.Therateofappreciationis[(1.1335–1.0016)/1.0016]*100=13.17percent.

10.AbsolutePPPsuggeststheMay2004exchangerateshouldbe122.2/116.4=1.0498.Theactualexchangerateis1.19.Hence,theeuroisovervaluedrelativetotheU.S.dollarby(1.19–1.0498)/1.0498]•100=13.35percent.

11.RelativePPPcanbeusedtocalculateapredictedvalueoftheexchangerateas:

SPPP=1.05•[(122.2/112.7)/(116.4/107.5)]=1.0014.

12.Theactualexchangerateis1.19.Hence,theeuroisovervaluedrelativetotheU.S.dollarby(1.19–1.0014)/1.0014]•100=18.83percent.

3、V.AnswerstoEndofChapterQuestions

1.Rankingthevariousexchangeratearrangementsbyflexibilityisnotsoclearcut.Nonethelessthearrangementsdescribedinthischapterare(fromfixedtoflexible):

dollarization,currencyboard,commodity(standard)peg,dollar(standard)peg,currencybasketpeg,crawlingpeg,managedfloat,flexible.

2.ThetwoprimaryfunctionsoftheInternationalMonetaryFundare:

surveillanceofmembernations'macroeconomicpolicies,andtoprovideliquiditytomembernationsexperiencingpaymentsimbalances.

3.ThevalueoftheCanadiandollarrelativetogoldisCAN$69(1.38•$50)andthevalueoftheBritishpoundrelativetogoldis£33.33($50/1.50).

4.TheexchangeratebetweentheCanadiandollarandtheBritishpoundisC$/£2.07(1.38•1.50).

5.Thecurrencyvalueofthepesocanbeexpressedas$0.50+€.50=P1.Theexchangeratebetweenthedollarandtheeurocanbeusedtoconverttheeuroamounttoitsdollarequivalentof$0.55.Hence,$1.05=P1,orandexchangevalueof0.952P/$.Usingtheexchangeratebetweenthedollarandtheeuroagain,theexchangeratebetweenthepesoandtheeurois0.1.048P/€(0.952P/$•1.10$/€).

6.Because$1.05isthecurrencycontentofthebasket,asshownabove,and$0.50ofthatcontentisattributabletothedollar,theweightassignedtothedollaris0.50/1.05=0.476,or47.6percent.Becausetheweightsmustsumtounity,theweightassignedtotheeurois52.4percent.

7.Themaindifferencebetweenthetwosystemswasthat,intheSmithsoniansystem,thedollarwasnotpeggedtothevalueofgold.OnereasonthatthesystemwasshortwasbecausetherewaslittleconfidencethatU.S.economicpolicywouldbeconductedinamannerconducivetoasystemofpeggedexchangerates.

8.Theprincipleresponsibilitiesofacurrencyboardaretoissuedomesticcurrencynotesandpegthevalueofthedomesticcurrency.Acurrencyboardisnotallowedtopurchasedomesticdebt,actasalenderoflastresort,orsetreserverequirements.

9.TheLourveaccordestablishedunofficiallimitsoncurrencyvaluemovements.Inasense,itwaspegwithbandsforeachofthemaincurrencies(dollar,yenandmark).

10.Differencesinthefundamentaldeterminantsofcurrencyvaluesbetweenthepeggingcountryandtheothercountryshouldbeconsidered.Tothispointofthetext,therateofinflationisagoodexample.RelativePPPcanbeusedtodetermin

升级会员

升级会员