FRMExam完整版真题试题.docx

《FRMExam完整版真题试题.docx》由会员分享,可在线阅读,更多相关《FRMExam完整版真题试题.docx(69页珍藏版)》请在冰豆网上搜索。

FRMExam完整版真题试题

Question1

Whichtypeofoptionproducesdiscontinuouspayoffprofiles.meaningthatthepayoffdoesnotincreaseordecreasecontinuouslywiththeunderlyingassetvalue?

a.Chooseroptions

b.Barrieroptions

c.Binaryoptions

d.Lookbackoptions

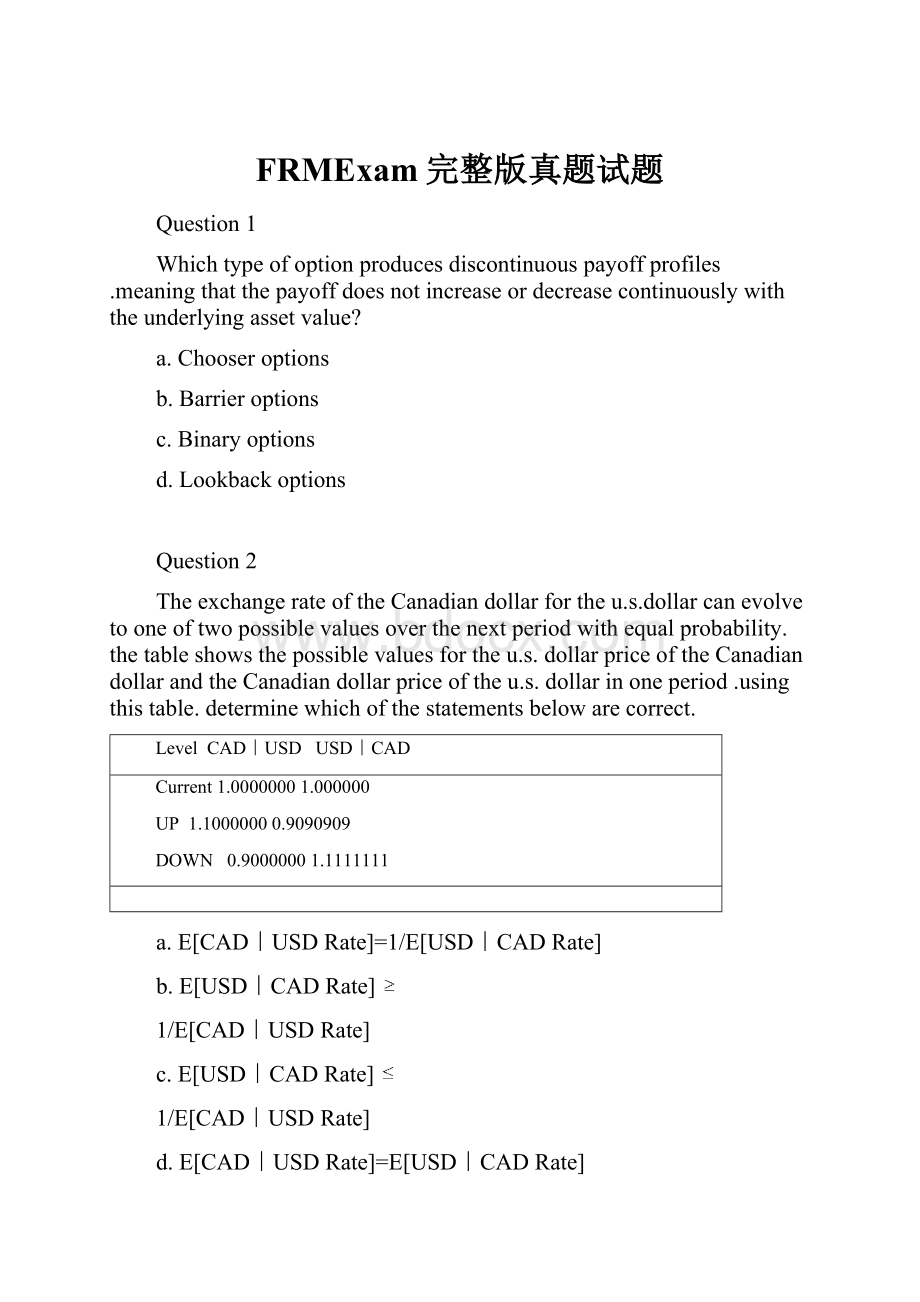

Question2

TheexchangerateoftheCanadiandollarfortheu.s.dollarcanevolvetooneoftwopossiblevaluesoverthenextperiodwithequalprobability.thetableshowsthepossiblevaluesfortheu.s.dollarpriceoftheCanadiandollarandtheCanadiandollarpriceoftheu.s.dollarinoneperiod.usingthistable.determinewhichofthestatementsbelowarecorrect.

LevelCAD|USDUSD|CAD

Current1.00000001.000000

UP1.10000000.9090909

DOWN0.90000001.1111111

a.E[CAD|USDRate]=1/E[USD|CADRate]

b.E[USD|CADRate]

1/E[CAD|USDRate]

c.E[USD|CADRate]

1/E[CAD|USDRate]

d.E[CAD|USDRate]=E[USD|CADRate]

Answerquestions3and4basedonthefollowinginformation

AriskmanagerforABCbankhascompiledthefollowingdateregardingabondtraderandanequitytrader.Assumethatthereturnsarenormallydistributedandthatthereare52tradingweeksperyear.ABCbankcomputesitscapitalusinga99%VaR.theafter-taxprofitsareall-inclusive.

ABCBankDate—USDmillions

After-taxnetbookweeklytax

Profitmarketvaluevolatilityrate

Bondtrader

Equitytrader

USD8USD1201.1%40%

USD18USD1801.94%40%

Question3

UsingtheABCbankdate.calculatetheannualrisk-adjustedreturnoncapital(RAROC)forthebondtrader?

a.25.24%

b.36.08%

c.60.15%

d.84.92%

Question4

UsingtheABCbankdate.whichofthefollowingstatementsarecorrectinrelationtotheequitytrader?

Theequitytraderhasanannual.after-taxVaRata99%confidoncelevelofUSD33.2million.

IncomparingtheRAROCforbothtraders.theequitytraderisperformingbetterthanthebondtrader.

a.Ⅰonly

b.Ⅱonly

c.Both

d.Neither

Question5

Thestand-aloneeconomiccapitalrequirementsforinsurancecompaniescanbebrokendownintothreemajorrisk;creditrisk,market/ALMriskandoperatingandotherrisks.analyzingtherisk.profilesofalifeinsurer;aP&Cinsurer.Adiversifiedinsurer,andapropertyinsurerthehighestmarket/ALMriskwouldbefora:

a.Lifeinsurer

b.P&Cinsurer

c.Diversifiedinsurer

d.Propertyinsurer

Question6

companyXYZ’spensionfundhasliabilitiesofUSD100millionandassetsofUSD120million.Theannualgrowthoftheliabilitieshasanexpectedvalueof5%with3%volatility.thereturnoftheassetshasanexpectedvalueof8%with12%volatility.Thecorrelationbetweenassetreturnandliabilitygrowthis0.3.whatisthe95%surplus-at-risk?

a.USD27.6million

b.USD22.7million

c.USD13.8million

d.USD18.1million

Question7

consideranall-equityfirmwithequitycapitalizationofUSD2billion.Thefirm’sCFOconsidersthefollowingthreefinancingstrategies

1.issuezero-couponseniordebtwithprincipalamountofUSD1billionpayablein10yearsandpurchaseinsuranceforUSD100millionthatwillpaylossesontheseniordebttoinvestorsinexcessofUSD500million

2.issuezero-couponjuniordebtwithprincipalamountofUSD500millionpayables10yearsandissuezero-couponseniordebtwithprincipalamountofUSD500millionpayables10years

3.issuezero-couponseniordebtwithprincipalamountofUSD1billionpayable10yearswithaputoptionattachedthatgivesinvestorstherighttoputdebttothefirmatmaturityfortheprincipalamount

whichofthesesstrategieswouldhavethemostriskyseniordebt?

a.Strategy1

b.Strategy2

c.Strategy3

d.Seniordebtsareequallyriskyinallthreestrategies

Question8

gammaindustriesincissuesaninversefloaterwithafacevalueofUSD50.000.000thatpaysasemiannualcouponof1150%minusLIBROgammaindustriesintendstoexecuteanarbitragestrategyandearnaprofitbysellingthenotes.Usingtheproceedstopurchaseabondwithafixedsemiannualcouponrateof6.75%ayearandthenhedgetheriskbyenteringintoanappropriateswap.Gammaindustriesreceivesaquotefromaswapdealerwithafixedrateof5.75%andafloatingrateofLIBOR.WhatwouldbethemostappropriatetypeofswapofGammaindustries,Inc.,toenterintotohedgeitsrisk?

a.Pay-fixed,receive-fixedswap

b.Pay-floating,receive-fixedswap

c.Pay-fixed,receive-floatingswap

d.Theriskcannotbehedgedwithaswap

Question9

aportfoliomanagerentersintoatotalofreturnswapasthetotalreturnreceiver.Underwhichofthefollowingsituationswouldtheportfoliomangerberequiredtomakeanetoutlaytothecounterparty?

a.Ifthetransactionwasinitiatedasahedge.Thennooutlaywasrequired

b.Iftherewereacapitalgainonthereferenceasset

c.Ifthemarketvalueofthereferenceassetdecreasedsignificantly

d.Ifthespreadbetweenthereferenceassetandthebenchmarkassetchanged

Question10

whichofthefollowingstatementsaboutcombatingmodelriskareincorrect?

1Ifapositionisknowtohaveconsiderablemodelrisk.Afirmcanlimititsexposurebyimposingatighterpositionlimit

2Ifwealwayschoosethemodelthattakesintoaccountthelargestnumberofreal-worldfactorsthataffectprices.Thefirm’sexposuretomodelriskwillbereduced

3Runningregularstresstestsorscenarioanalysestotestthevolatility.Correlationandliquidityassumptionsinmodelhelpsreducemodelrisk

4Riskmanagersshouldcheckthetrader’spricingmodeltoensurethatmodelcalibrationisup-to-dateandthatmodelsareupgradedinlinewithmarketbestpracticeandtoensurethatobsoletemodelsareidentifiedandtakenoutofuse

a.Nonearetrue

b.Ⅱonly

c.Ⅰ,ⅢandⅣ

d.Ⅰ,ⅡandⅢ

Question11

Whichtypeofdistributionproducesthelowestprobabilityforavariabletoexceedaspecifiedextremevalue“X”Whichisgreaterthanthemean,assumingthedistributionallhavethesamemeanandvariance?

a.Aleptokurticdistributionwithakurtosisof4.

b.Aleptokurticdistributionwithakurtosisof8.

c.Anormaldistribution.

d.Aplatykurticdistribution.

Question12

AnAmericaninvestorholdsaportfolioofFrenchstocks.Themarketvalueofportfoliois€10million,withabetaof1.35relativetoCACindex.InNovember,thespotvalueoftheCACindexis4750.TheexchangerateisUSD1.25/€.Thedividendyield.aurointerestratesanddollarinterestratesareallequalto4%.Whichofthefollowingoptionstrategieswouldbethemostappropriatetoprotecttheportfolioagainstadeclineoftheeuro?

MarchEurooptions(allpricesinUSdollarper€)

StrikeCalleuroPuteuro

1.250.0180.022

a.BuycallswithapremiumofUSD160,000.

b.BuyputswithapremiumofUSD220,000.

c.SellcallswithapremiumofUSD180,000.

d.SellputswithapremiumofUSD220,000.

Question13

Inanattempttoprovideguidanceonanadditionalstepstobetakenbytheprivatesectortopromotetheefficiency,effectivenessandstabilityoftheglobalfinancialsystem.ThecounterpartyriskmanagementpolicyGroupII(GRMPGII)publishedareportinJuly2005containingrecommendationsandguidingprinciples.AccordingtotheGRMPGIIreport,whichofthefollowingstatementsrelatingtoEmergingIssueisincorrect?

a.GRMPGIIrecommendsthatfiduciariestakingonrisksassociatedwithcomplexproductsshouldhavetheabilitytoaggregateriskacrosstheirentirepoolofassetsinordertounderstandportfolio-levelimplications.

b.GRMPGIIrecommendsthathedgefunds.onavoluntarybasis,adopttherelevantrecommendationsandguidingprinciplescontainedintheir(GRMPGII)report.

c.Asaguidingprincipleinsellingstructuredproductstoretailinvestors,financialintermediariesshouldconsiderwhetherdisclosureappropriatelyconveysthefactthatsecondarymarketvalue,atmaturity,willbelessthantheissueprice.

d.Asaguidingprinciple,seniormanagementshouldconductperiodicreviewsofthefinancialintermediary’sinternalcontrolsforthesaleofcomplexproductsretailinvestors.

Question14

Whichstatementbestdescribescorrelationsanvariancesintimesoffinancialcrisis?

a.Thereareonlymarginalchangesincorrelationsandvariancesintimesofcrisis,andthereforetheydonotneedtobefactoredintoriskmanagement.

b.Thediversificationbenefitsdecreasebecausecorrelationsincrease,andthereforeyourrisklevelincreases.

c.Thediversificationbenefitsincreasebecausecorrelationsdecrease,andthereforeyourriskleveldecreases.

d.VaRestimatesusingtheRiskmetricsapproachprovidefortheeffectsofincreasedcorrelationsduringperiodscrisis,andthereforetheeffectsarefactoredintocurrentpositions.

Question15

Assumethemarginalmonthlydefaultrates(conditionalonnopreviousdefault)forafirmare2%eachmonthduringthefirstyearand3%eachmonthduringthesecondyear.Whatisthemarginalprobabilityofdefaultingoverthethesecondyear,conditionalonnothavingdefaultedthefirstyear?

a.Insufficientinformationtoanswerthequestion

b.30.6%

c.36.0%

d.47.4%

Question16

GiventworandomvariablesXandY,WhatisthevarianceofX,GivenVariance[Y]=100.

Variance[4X-3Y]=2,700andthecorrelationbetweenXandYis0.5?

a.56.3

b.113.3

c.159.9

d.225.0

Question17

Aportfoliohasanaveragereturnoverthelastyearof13.2%.Itsbenchmarkhasprovidedanaveragereturnoverthesameperiodof12.3%.Theportfolio’sstandarddeviationis15.3%,itsbetais1.15,itstrackingerrorvolatilityis6.5%anditssemi-standarddeviationis94%.Lastly,therisk-freerateis4.5%.Calculatetheportfolio’sinformationRatio(IR).

a.0.569

b.0.076

c.0.138

d.

升级会员

升级会员