财务会计课件 from Professor CarterChapter08Word文档格式.docx

《财务会计课件 from Professor CarterChapter08Word文档格式.docx》由会员分享,可在线阅读,更多相关《财务会计课件 from Professor CarterChapter08Word文档格式.docx(47页珍藏版)》请在冰豆网上搜索。

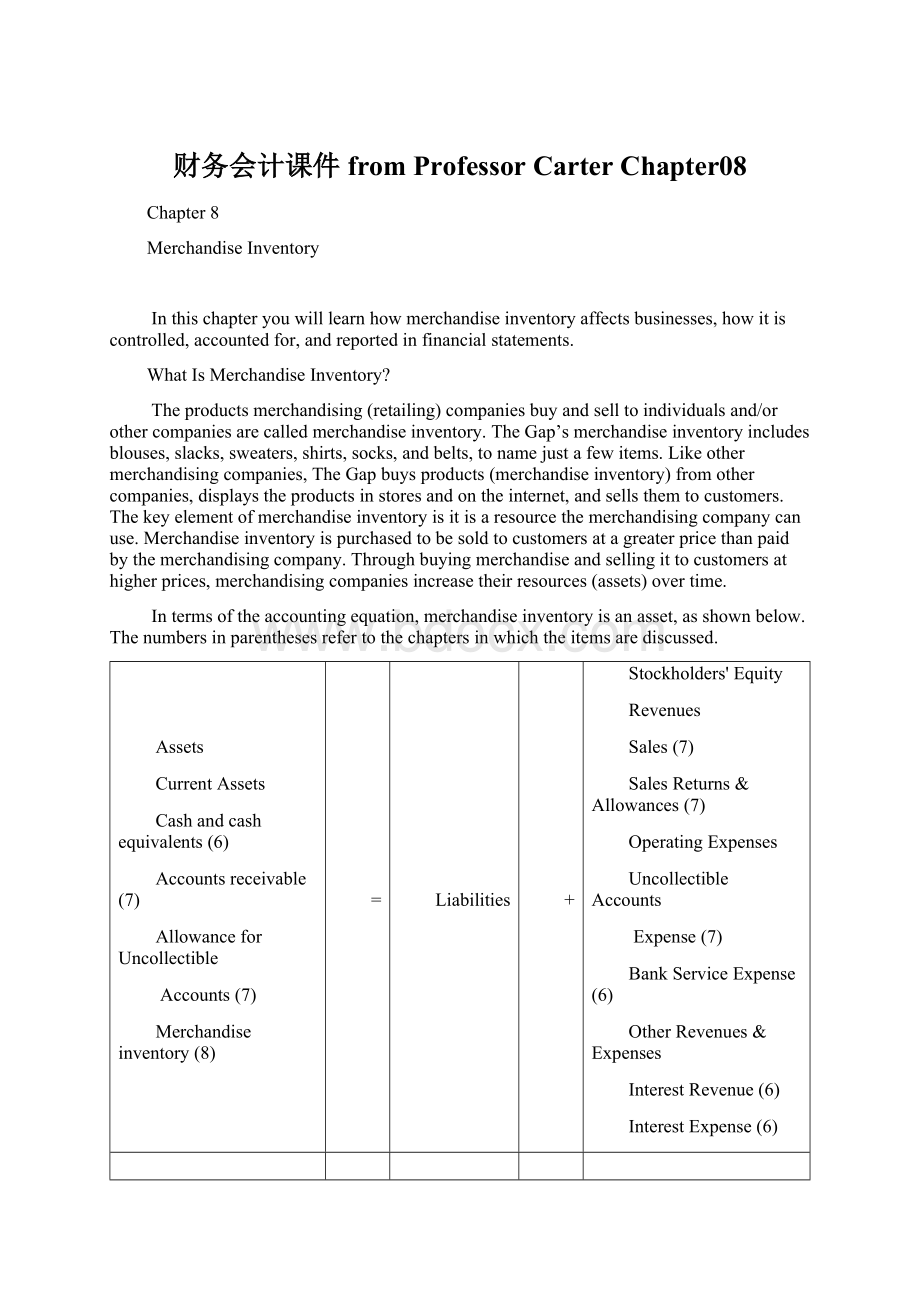

Intermsoftheaccountingequation,merchandiseinventoryisanasset,asshownbelow.Thenumbersinparenthesesrefertothechaptersinwhichtheitemsarediscussed.

Assets

CurrentAssets

Cashandcashequivalents(6)

Accountsreceivable(7)

AllowanceforUncollectible

Accounts(7)

Merchandiseinventory(8)

=

Liabilities

+

Stockholders'

Equity

Revenues

Sales(7)

SalesReturns&

Allowances(7)

OperatingExpenses

UncollectibleAccounts

Expense(7)

BankServiceExpense(6)

OtherRevenues&

Expenses

InterestRevenue(6)

InterestExpense(6)

Theamountofmerchandiseinventorydiffersfromcompanytocompanyandfromyeartoyearwithinagivencompany.Forexample,Wal-Mart,thelargestretailcompanyintheUnitedStates,reportedmerchandiseinventoryof$33.2billiononJanuary31,2010.This$33.2billionwasapproximately19%ofWal-Mart’sJanuary31,2010totalassets.Aeon,thelargestretailcompanyoutsideoftheUnitedStates,reportedmerchandiseinventoryof334billionyenonFebruary28,2010.The334billionyenwasapproximately9%ofAeon’sFebruary28,2010totalassets.Oneyearearlier,onJanuary31,2009,Wal-Mart’smerchandiseinventorywas$34.5billionorapproximately21%ofWal-Mart’stotalassets.

Merchandising:

AnOverview

ThefollowingparagraphsbrieflydescribehowmerchandiseinventoryaffectsmerchandisingcompaniesbydiscussingonepartoftheoperationsoftheMatthewSportingGoodsCompany.AsyoumayrememberfromChapter7,theMatthewSportingGoodsCompanysellssportingequipmentandsuppliestoyouthorganizations.Thefollowingparagraphsarerestrictedtoonlythatpartofthecompany'

soperationsrelatingtothesaleofcustomizedbaseballshirts.Eachshirtisimprintedwithateam'

snameandlogo.AsshowninExhibit8-1,therearefourstepsinvolvedwiththecompany’smerchandiseinventory(baseballshirts):

(1)thepurchaseofmerchandisefromsuppliers,

(2)thesaleofmerchandisetocustomers,(3)thecollectionofcashfromcustomers,and(4)thepaymentofcashtosuppliers.Aswillbeshown,theMatthewSportingGoodsCompanyattemptstoincreaseitsresourcesthroughthesefoursteps.

Exhibit8-1

MatthewSportingGoodsCompany

MerchandisingOperations

2A

Step1:

purchasemerchandiseoncreditfromsuppliersInordertosellbaseballshirtstocustomers,theMatthewSportingGoodsCompanymustpurchasetheshirtsfromothercompanies.Theseothercompaniescouldalsobemerchandisingcompaniesortheycouldbecompaniesthatmaketheshirts,calledmanufacturers.AlthoughtheMatthewSportingGoodsCompanydoespurchasesomeproductsbypayingcash,thevastmajorityofitspurchasesareoncredit.Thatis,thecompanybuysmerchandisebypromisingtopayforitinthenearfuture,oftenwithin30days.Asaresultofbuyingmerchandiseoncredit,thecompany'

sresources(assets)increase,asshowninExhibit8-1bythearrowindicatingresourcescomingintothecompany(Step1).Sincethesourceoftheseresourceswascreditors,thecompany'

sliabilities,calledaccountspayable,alsoincrease.Ifthecompanybuys100shirtsatacostof$24pershirt,theeffectsofstep1,thepurchaseofmerchandisefromsuppliers,canbesummarizedasfollows.

TotalResources

SourcesofBorrowedResources

Sourcesof

OwnerInvestedResources

SourcesofManagement

Generated

Resources

purchase

ofmerchandiseoncredit

+$2,400

Step2:

sellmerchandiseoncredittocustomersWhentheMatthewSportingGoodsCompanysellssomeofitsshirtstocustomers,twothingshappensimultaneously:

thecompany’sresourcesdecreasewhentheshirtsgotothecustomersandthecompany’sresourcesincreasewhenthecustomerseitherpayfortheshirtsorpromisetopayfortheshirtsinthenearfuture.Remember,thecompany’sbusinessistosellproducts,notgivethemaway!

Becauseknowledgeofeachofthesetwoeffectsisimportanttomanagers,thesaleofproductstocustomersisseparatedintoitstwoparts:

thedecreaseinresourceswhentheshirtsgotocustomersandtheincreaseinresourceswhenthecustomerspayorpromisetopayfortheshirts.

TheflowofmerchandisetocustomersWhentheMatthewSportingGoodsCompany’sshirtsgotoitscustomers,theobviouseffectisadecreaseinthecompany’sresources,asshowninExhibit8-1bythearrowindicatingresourcesgoingoutofthecompany(Step2,part2A).Consistentwithourtreatmentofresourcesinpreviouschapters,thisdecreasemaybeviewedasaresultofmanagementusingupsomeresources.Theresources(shirts)werenotsenttocreditors,norweretheydistributedtoowners.Theresources(shirts)wereusedupbymanagementintheperformanceofmanagement’sresponsibilityforoperatingthecompany.Whenmanagementusesupresourcesintheoperationofthecompany,suchusesarereportedasexpenses.Withmerchandiseinventory,the“usingup”ofshirtsbythemgoingtocustomersisreportedasadecreaseinmerchandiseinventoryandanincreaseinanexpensecalledthecostofgoodssold.Sinceexpensesdecreasestockholders’equity,theultimateresultofshirtsgoingtocustomersisadecreaseinresources(assets)andanequaldecreaseinstockholders’equity(throughtheincreaseinthecostofgoodssold“expense”).Ifall100oftheMatthewSportingGoodsCompany’sshirtsgotoitscustomers,theeffectscanbesummarizedaspresentedasstep2Abelow.Sinceeachoftheshirtscostthecompany$24,theresourcesdecreaseandstockholders’equitydecreaseare$2,400(100x$24).

SourcesofManagementGenerated

Step2A:

flowofmerchandisetocustomers(expense)

-$2,400

Totals

$0

Theflowofpromises(accountsreceivable)fromcustomersAtthesametimetheMatthewSportingGoodsCompany’scustomersreceivetheshirts,theymustgivesomethinginreturntothecompany.Usuallycustomersgiveeithercashorpromisesofcash.Thus,thecompanyreceiveseithercashoraccountsreceivable.Ineithercase,theobviouseffectisanincreaseinthecompany’sresources,asshowninExhibit8-1bythearrowindicatingresourcescomingintothecompany(Step2,part2B).Consistentwithourtreatmentofresourcesinpreviouschapters,thisincreasemaybeviewedasaresultofmanagementgeneratingresources.Theresources(cashoraccountsreceivable)werenotborrowedfromcreditorsnorinvestedbyowners.Theresourcesweregeneratedbymanagementintheperformanceofmanagement’sresponsibilityforoperatingthecompany.Whenmanagementgeneratesresourcesintheoperationofthecompany,suchgenerationsarereportedasrevenues.Withthesaleofproductstocustomers,thereceiptofcashoraccountsreceivablefromcustomersisreportedasanincreaseincashoraccountsreceivableandanincreaseinarevenuecalledsales.Sincerevenuesincreasestockholders’equity,theultimateresultofthereceiptofcashoraccountsreceivablefromcustomersisanincreaseinresources(assets)andanequalincreaseinstockholders’equity(throughtheincreaseinsales“revenue”).Ifthe100shirtsoftheMatthewSportingGoodsCompanyweresoldtoitscustomersoncredit,atapriceof$37each,theeffectscanbesummarizedaspresentedasstep2Bbelow.Theresourceincreaseandthestockholders’equityincreaseare$3,700(100x$37).

Step2B:

flowofaccountsreceivablefromcustomers(revenue)

+$3,700

+$1,300

Step3:

collectcashfromcustomersWithinaveryshorttime,often30daysorless,theMatthewSportingGoodsCompanycollectscashfromcustomerstowhomitsoldshirtsoncredit.Asaresult,ascashincreasesandaccountsreceivabledecrease,thecompany’sresourcesincreaseanddecreasebythesamedollaramount,asshowninExhibit8-1bythearrowsatStep3.IftheMatthewSportingGoodsCompanycollectsallofitsaccountsreceivablefromitsc

升级会员

升级会员