美国会计准则与国际会计准则比较摘录Word文件下载.docx

《美国会计准则与国际会计准则比较摘录Word文件下载.docx》由会员分享,可在线阅读,更多相关《美国会计准则与国际会计准则比较摘录Word文件下载.docx(14页珍藏版)》请在冰豆网上搜索。

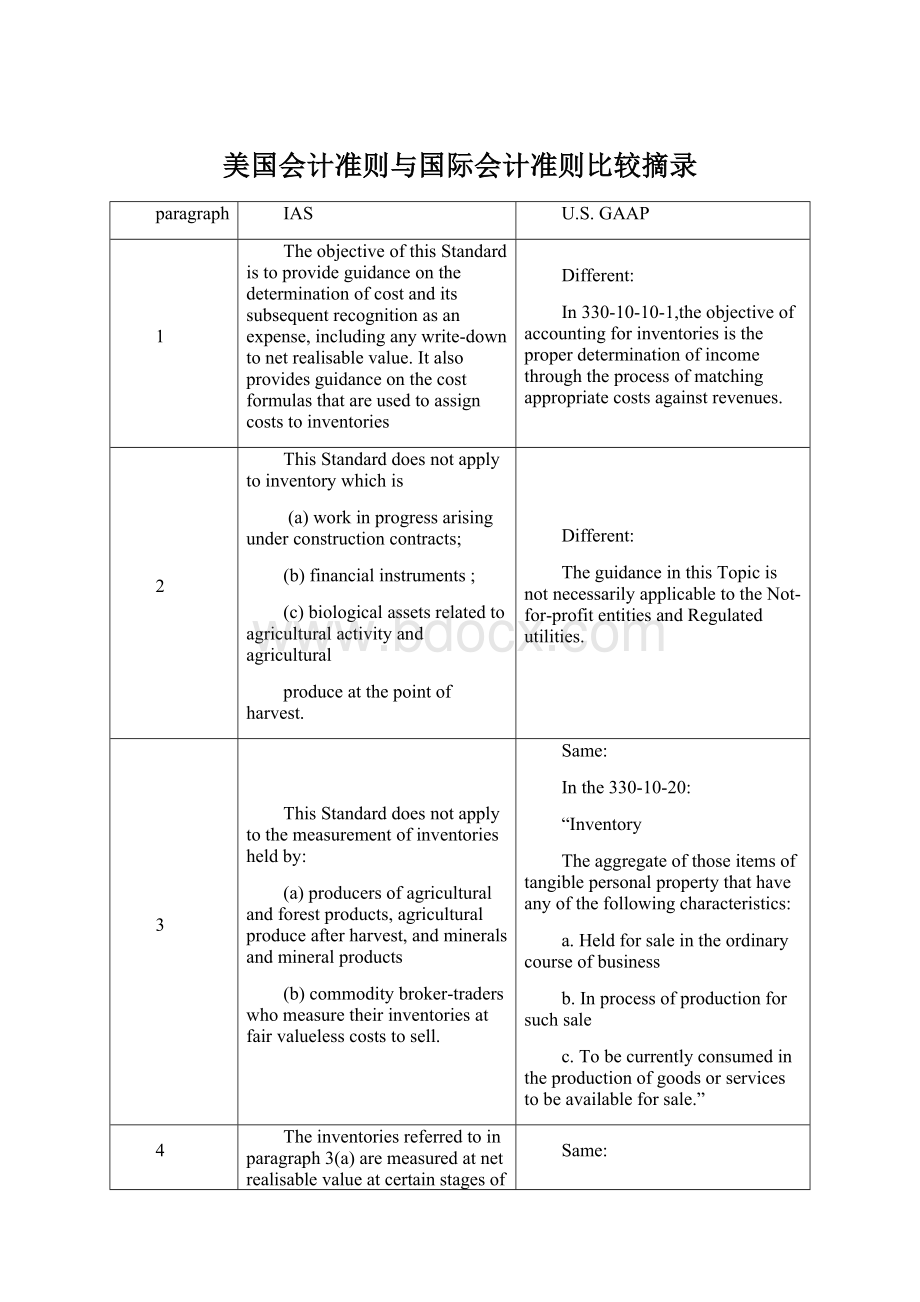

TheobjectiveofthisStandardistoprovideguidanceonthedeterminationofcostanditssubsequentrecognitionasanexpense,includinganywrite-downtonetrealisablevalue.Italsoprovidesguidanceonthecostformulasthatareusedtoassigncoststoinventories

Different:

In330-10-10-1,theobjectiveofaccountingforinventoriesistheproperdeterminationofincomethroughtheprocessofmatchingappropriatecostsagainstrevenues.

2

ThisStandarddoesnotapplytoinventorywhichis

(a)workinprogressarisingunderconstructioncontracts;

(b)financialinstruments;

(c)biologicalassetsrelatedtoagriculturalactivityandagricultural

produceatthepointofharvest.

TheguidanceinthisTopicisnotnecessarilyapplicabletotheNot-for-profitentitiesandRegulatedutilities.

3

ThisStandarddoesnotapplytothemeasurementofinventoriesheldby:

(a)producersofagriculturalandforestproducts,agriculturalproduceafterharvest,andmineralsandmineralproducts

(b)commoditybroker-traderswhomeasuretheirinventoriesatfairvaluelesscoststosell.

Same:

Inthe330-10-20:

“Inventory

Theaggregateofthoseitemsoftangiblepersonalpropertythathaveanyofthefollowingcharacteristics:

a.Heldforsaleintheordinarycourseofbusiness

b.Inprocessofproductionforsuchsale

c.Tobecurrentlyconsumedintheproductionofgoodsorservicestobeavailableforsale.”

4

Theinventoriesreferredtoinparagraph3(a)aremeasuredatnetrealisablevalueatcertainstagesofproduction.Forexample,whenagriculturalcropshavebeenharvestedormineralshavebeenextractedandsaleisassuredunderaforwardcontractoragovernmentguarantee,orwhenanactivemarketexistsandthereisanegligibleriskoffailuretosell.TheseinventoriesareexcludedfromonlythemeasurementrequirementsofthisStandard

In905-330-25-01

“Alldirectandindirectcostsofgrowingcropsshallbeaccumulateduntilthetimeofharvest.Somecropcosts,suchassoilpreparation,areincurredbeforeplantingandshallbedeferredandallocatedtothegrowingcrop."

5

Broker-tradersarethosewhobuyorsellcommoditiesforothersorontheirownaccount.Theinventoriesreferredtoinparagraph3(b)areprincipallyacquiredwiththepurposeofsellinginthenearfutureandgeneratingaprofitfromfluctuationsinpriceorbroker-traders’margin.Whentheseinventoriesaremeasuredatfairvaluelesscoststosell,theyareexcludedfromonlythemeasurementrequirementsofthisStandard.

Thesameas940-20-05-03

“Actingasanagent,abroker-dealermaybuyandsellsecuritiesonbehalfofitscustomers.Inreturnforsuchservices,thebroker-dealerchargesacommission.Eachtimeacustomerentersintoabuyorselltransaction,acommissionisearnedbythebroker-dealerforitssellingandadministrativeefforts.”

6

Inventoriesareassets:

(a)heldforsaleintheordinarycourseofbusiness;

(b)intheprocessofproductionforsuchsale;

or

(c)intheformofmaterialsorsuppliestobeconsumedinthe

productionprocessorintherenderingofservices.

Thesameas330-10-20Glossary.

“Theaggregateofthoseitemsoftangiblepersonalpropertythathaveanyofthefollowingcharacteristics:

c.Tobecurrentlyconsumedintheproductionofgoodsorservicestobeavailableforsale.“

7

Netrealisablevalueisthenetamountthatanentityexpectstorealisefromthesaleofinventoryintheordinarycourseofbusiness.Fairvaluereflectsthepriceatwhichanorderlytransactiontosellthesameinventoryintheprincipalmarketforthatinventorywouldtakeplacebetweenmarketparticipantsatthemeasurementdate.

InMasterGlossary,thenetrealizablevalueisaestimatedsellingpriceslessreasonablypredictablecostsofcompletion,disposal,andtransportation.

InMasterGlossary,thefairvalueis:

Thepricethatwouldbereceivedtosellanassetorpaidtotransferaliabilityinanorderlytransactionbetweenmarketparticipantsatthemeasurementdate.

8

Inventoriesencompassgoodspurchasedandheldforresaleincluding,alsoencompassfinishedgoodsproduced,orworkinprogressbeingproduced,bytheentityandincludematerialsandsuppliesawaitinguseintheproductionprocess.

Issameas330-10-20Glossary.

“Theterminventoryembracesgoodsawaitingsale(themerchandiseofatradingconcernandthefinishedgoodsofamanufacturer),goodsinthecourseofproduction(workinprocess),andgoodstobeconsumeddirectlyorindirectlyinproduction(rawmaterialsandsupplies).Thisdefinitionofinventoriesexcludeslong-termassetssubjecttodepreciationaccounting,orgoodswhich,whenputintouse,willbesoclassified.Thefactth

升级会员

升级会员