3外文翻译.docx

《3外文翻译.docx》由会员分享,可在线阅读,更多相关《3外文翻译.docx(19页珍藏版)》请在冰豆网上搜索。

3外文翻译

Ⅲ.外文翻译

外文翻译之一

MonetaryPolicyIndependence,theCurrencyRegime,

andtheCapitalAccountinChina

Author:

EswarS.Prasad

Nationality:

America

SourseandType:

PaperpresentedattheConferenceonChina'sExchangeRatePolicyPetersonInstituteforInternationalEconomicsHttp:

//unjobs.org

Journaltime:

October19,2007,P7-13

China’scurrencypolicyhasofcoursereceivedthemostattentionoflate.Whetherthemaintenanceofafixedexchangerateispartofadeliberatemercantiliststrategytopromoteexport-ledgrowthhasbeenthesubjectofintensedebate.Ontheonehand,ChinahashadarelativelystableexchangeraterelativetotheU.S.dollarsince1995.ThispolicywassustainedeventhroughtheAsiancrisiswhenthetemptationsfordevaluingthecurrencyweregreat.Ontheotherhand,duringthisdecadetheexchangeratehasbeenkeptfromappreciatingonlybymassiveinterventionintheexchangemarket.Intandemwithsustainedhighexportgrowthandaburgeoningcurrentaccountsurplusthatnearlyhit10percentofGDPin2006,thishasbeenseenasprimafacieevidenceofagrosslyundervaluedcurrency.

Asdiscussedinmoredetailbelow,oneoftheprincipalconcernsisthatthelackofexchangerateflexibilitynotonlyreducesmonetarypolicyindependence,italsohampersbankingsectorreforms.TheinabilityofthePBCtouseinterestratesasaprimarytoolofmonetarypolicyimpliesthatcreditgrowthhastobecontrolledbyblunterandnon-market-orientedtools,includingtargets/ceilingsforcreditgrowthaswellas“non-prudentialadministrativemeasures”.

China’sapproachtoexchangeratepoliyandcapitalaccountliberalizationmaybeindicativeofadesiretomaintainstabilityonthedomesticandexternalfrontswhileopeninguptotradeandfinancialflows.Andthelargestockofforeignexchangereservesresultingfromthesepoliciesmayserveasinsuranceagainstvulnerabilitiesarisingfromaweakbankingsystem.Buttherecomesapointwhenthepolicydistortionsneededtomaintainthisapproachcouldgenerateimbalances,imposepotentiallylargewelfarecosts,andthemselvesbecomeasourceofinstability.

Tobeginwith,whyistheexchangerateregimeofsuchimportance?

Afterall,theexchangerateisjustarelativeprice.Moreover,economicmodelstellusthatmacroeconomicfundamentalswilleventuallywinoutintermsofwhatreallymatters---therealexchangerateratherthanthenominalexchangerate.Thatis,ifthenominalexchangeratedoesn’tadjustinresponsetochangesinfundamentals,relativepricelevelswilladjust.Butacombinationofpoliciessuchasfinancialrepressionandaclosedcapitalaccountcandelaythisadjustmentforasignificantperiod.Whilethiscanboostexportcompetitivenessbykeepingtheexchangerateundervalued,therecanbesubtleindirectcosts,intermsofbotheconomicwelfareandreducedpolicyflexibilityinrespondingtovariousshocks.

Whatarethecostsofaninflexibleexchangerate?

Theschematicdiagrambelowlaysoutsomeoftheconnections,althoughthisshouldofcourseberecognizedasaheuristicdiagramthatignoresmanyofthecomplexitiesintherelationshipsdepictedhere.Themainpointisthataninflexibleexchangerate,whilenottherootcauseofimbalancesintheeconomy,requiresalargesetofdistortionarypoliciesforitsmaintenanceoverlongperiods.Itisthesedistortionsthat—throughmultiplechannels—hurteconomicwelfareandcould,overtime,shiftthebalanceofrisksintheeconomy.

LackofExchangeRageFlexibilityComplicatesMacroPolicyandReforms

MakingtheRightConnections

Anindependentinterestratepolicyisakeytoolforimprovingdomesticmacroeconomicmanagementandpromotingstablegrowthandlowinflation.AstheChineseeconomybecomesmorecomplexandmarket-oriented,itwillbecomehardertomanagethroughcommandandcontrolmethodsasinthepast.And,asitbecomesmoreexposedtoglobalinfluencesthroughitsrisingtradeandfinanciallinkagestotheworldeconomy,itwillalsobecomemoreexposedtoexternalshocks.Monetarypolicyistypicallythefirstlineofdefenseagainstmacroeconomicshocks,bothinternalandexternal.Hence,havingan

independentmonetarypolicyisimportantforoverallmacroeconomicstability.

Monetarypolicyindependenceis,however,amirageifthecentralbankismandatedtoattainanexchangerateobjective.Capitalcontrols,whichpreventmoneyfrommovinginanoutofaneconomyeasily,doinsulatemonetarypolicytosomeextent.Butcapitalcontrolsarenotoriouslyleaky(theunofficialflowsintoandoutofChinaitselfareampletestimonytothis)andtendtobecomeincreasinglylesseffectiveovertime.Thus,aflexibleexchangerateisaprerequisiteforanindependentmonetarypolicy.

However,openingthecapitalaccountaheadofintroducinggreaterflexibilityintheexchangeratecouldposeseriousproblemsinthefuture.Historyisrepletewithexamplesofcountriesthatopenedupthecapitalaccountwhilethingslookedgood,evenwhilekeepingtheirexchangeratesfixed,andwerethensubjecttolargeexchangeratedepreciationswhentheyweresubjecttosuddenstopsand/orreversalsofcapitalflows.

MarvinGoodfriendandIhavearguedthatChinashouldadoptanexplicitinflationobjective—along-runrangefortheinflationrateandanexplicitacknowledgementthatlowinflationisthepriorityformonetarypolicy—asanewanchorformonetarypolicy.Aninflationobjective,coupledwithexchangerateflexibility,wouldworkbesttostabilizedomesticdemandinresponsetointernalandexternalmacroeconomicshocks.Indeed,focusingoninflationstabilityisthebestwayformonetarypolicytoachievebroaderobjectivessuchasfinancialstabilityandhighemploymentgrowth.Overtime,theinflationobjectivewouldprovideabasisforcurrencyflexibility.Thus,exchangeratereformwillbeseenasakeycomponentofanoverallreformstrategythatisinChina’sshort-andlong-terminterests.

Tworelatedpointsareworthnoting.Independentinterestratepolicyrequiresaflexibleexchangerate,notaone-offrevaluationorasequenceofrevaluations.Aflexibleexchangeratebufferssomeoftheeffectsofinterestratechanges,especiallyintermsofoffsettingthetemptationforcapitaltoflowinoroutinresponsetosuchchanges.Aone-offrevaluationcansolvethisproblemtemporarily,butcouldcreateevenmoreproblemssubsequentlyifinterestrateactionsinadifferentdirectionbecomenecessary,orifinvestorsentimentandthepressuresforcapitalinflowsoroutflowsshift.Thisiswhythe

focusonalargeone-timerevaluationtoatoneforpastsinsdoesn’tgetusanywhere,eitherintermsofthepolicydebateorintermsofeffectingreformsthatreallymatter.

Anothercrucialpointisthatexchangerateflexibilityshouldnotbeconfusedwithfullopeningofthecapitalaccount.Anopencapitalaccountwouldallowthecurrencytofloatfreelyandbemarket-determined.Buttheexchangeratecanbemadeflexibleandtheobjectiveofmonetarypolicyindependenceachievedevenifthecapitalaccountisnotfullyopen.Indeed,asnotedabove,therearegoodreasonswhyitispreferabletomovemoregraduallyoncapitalaccountopeningthanonexchangerateflexibility.Afreefloatwithanopencapitalaccountisausefullong-termobjective,butisnotahighpriorityintheshortrun.

中国独立的货币政策,汇率制度和资本帐户

作者:

普拉萨德

国籍:

美国

出处及类别:

在彼得森国际经济研究所关于中国人民币汇率政策的会议上提交的论文Http:

//unjobs.org

发表时间及页码:

2007年10月19日,P7-13

中国的货币政策当然是最近以来最受瞩目的。

维持固定汇率是否是部分重商主义者蓄意的战略以促进出口导向型增长,一直受到激烈的辩论。

一方面,自1995年以来中国一直采取相对美元较为稳定的汇率。

甚至在亚洲(金融)危机时期人民币有巨大的贬值诱惑时这项政策也仍然维持。

另一方面,这十年期间汇率一直保持升值,而仅仅通过大规模干预外汇市场。

随着出口的持续高速增长和经常帐户盈余的不断膨胀,在2006年几乎达到国内生产总值的10%,这一直被视为严重低估货币的初步证据。

正如下文更加详细的讨论,(我们)关注的主要问题之一是:

汇率灵活性的缺失不仅降低了货币政策的独立性,而且阻碍了银行业的改革。

中国人民银行无法把利率作为一个主要的货币政策工具,这意味着,信贷增长将由粗放和非以市场为导向的工具所控制,包括信贷增长的目标/上限以及“非审慎的行政措施”。

中国对汇率政策和资本帐户自由化的方式可能表明了一个愿望,即在贸易开放和资本流动时维护国内、外的稳定。

而由此带来的大量的外汇储备积累可能是作为由脆弱的银行体系造成的漏洞的保险。

但有一点,当扭曲的政策需要维持时,这种方式会产生不平衡,潜在地强加了巨大的福利代价,自己也成为不稳定的根源。

首先,为什么汇率制度如此重要?

毕竟,汇率只是一个相对的价格。

此外,经济模型告诉我们,宏观经济基本面最终取决于真正重要的---实际汇率,而非名义汇率。

也就是说,如果名义汇率不跟随经济基本面的调整而调整,(则)相对价格水平就会调整。

但是政策的结合如金融压抑和封闭的资本帐户可以在一定时间内延迟这种调整。

虽然通过保持低估的汇率可以提高出口竞争力,(但)在应付各种冲击时会产生微妙的间接成本,以经济福利和政策灵活性的减少的形式。

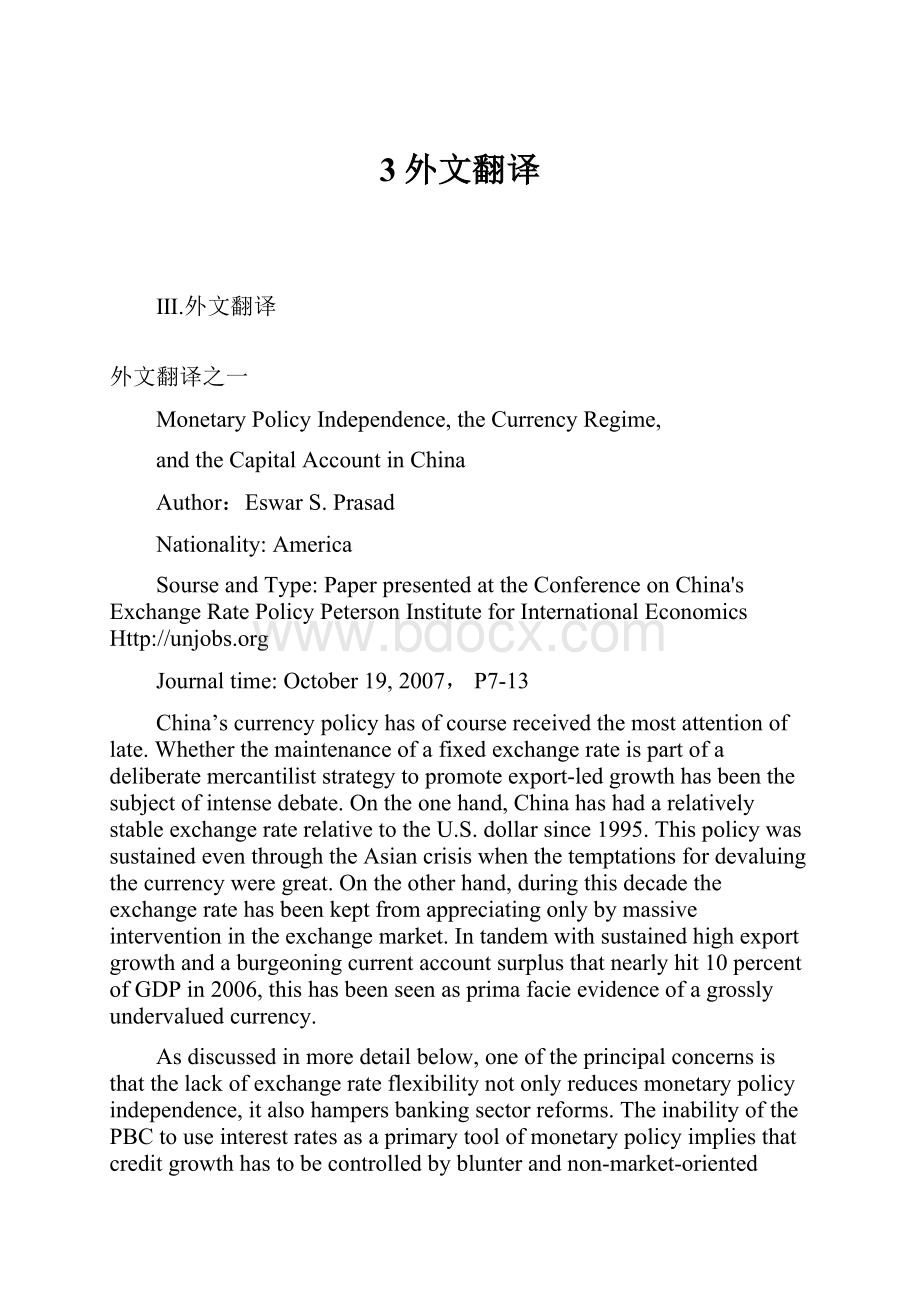

不灵活的汇率将会带来哪些代价?

下面的示意图列出了一些联系,尽管这应当被认为是启发式图,因为这里的描述忽略了许多复杂的关系。

主要的一点是一个非灵活性的汇率,而不是经济中不平衡的根源,需要大量的扭曲性政策来长时间的维护。

正是这些扭曲---通过多种渠道---损害经济福利并可能随着时间的推移转移经济中风险的平衡。

汇率缺乏灵活性使宏观调控政策和改革复杂化

资源分配不当,出口,投资带动不平衡增长

国内宏观管理更困难

利率政策不独立

风险

1.短期通胀和经济过热

2.中期通货紧缩+新增不良贷款

3.资产价格泡沫

4.如果贸易顺差加大,将受到贸易制裁

非灵活的汇率

经常项目巨大盈余,更多的资本流入

金融业改革更复杂

建立正确的联系

更好的宏观经济管理

货币政策具有独立性

均衡稳定的增长

金融业发展和改革

灵活的汇率

安全的资本账户开放

一个独立的利率政策是改善国内宏观经济管理、促进稳定增长和低通货膨胀的一个重要工具。

随着中国经济变得更加复杂、更加以市场为导向,和过去一样通过指挥和控制的方法去管理将变的更加困难。

通过贸易的增加和与世界经济加强金融联系,使它更容易受到全球影响,也将更容易受到外部冲击。

货币政策通常是对宏观经济冲击的第一道防线,包括内部和外部冲击。

因此,拥有独立的货币政策对于整个宏观经济的稳定性是非常重要的。

如果中央银行的任务是实现汇率目标,那么货币政策的独立性却是一种幻想。

资本管制可以防止资金自由地在一个经济体进进出出,在一定程度上为货币政策(起到)隔绝(作用)。

但资本管制有明显的渗漏(非官方的流入和流出中国本身就充分证明了这一点),而且随着时间的推移往往变得越来越不那么有效。

因此,灵活的汇率机制是建立一个独立的货币政策的先决条件。

然而,开放资本帐户先于引入更具灵活性的汇率可能对将来会造成严重问题。

历史上有许多国家开放资本帐户,看上去情况很好,甚至同时保持了固定汇率,当受到资本突然停止和/或逆转时,汇率就会面临大幅的贬值。

马文·古德弗兰德和我都认为中国应采取一个明确的通货膨胀目标---在长期范围内的通货膨胀率和对低通货膨胀率是货币政策优先选择的明确认识---作为一种新的货币政策支柱。

通货膨胀目标,再加上汇率的灵活性,将是稳定国内需求来应对内外部宏观经济冲击的良方。

事实上,强化通货膨胀率稳定是货币政策实现更广泛目标的最好方式,如金融的稳定和高就业增长。

随着时间的推移,通货膨胀目标将为汇率的灵活性提供一个基础。

因此,在我国的短期和长远利益中,汇率改革将被看作全面改革战略的一个关键组成部分。

两个相关点是值得注意的。

独立的利率政策需要一个灵活的汇率,而不是一次性重估或一系列地重估。

一种灵活的汇率可以缓冲一些利率变化的影响,特别是在抵消由这种变化引起的资本流进流出诱惑。

一次性重估可以暂时解决这个问题,但如果利率开始必然性地朝着另一个方向变动,或如果投资者对资本流入流出的情绪和压力发生转变,那么就会随之引起更多的问题。

这就是为什么专注于一次性重估来弥补过去的罪孽不让我们到达某种地步,无论是政策辩论的形式还是实行改革的形式都不起作用。

另一关键点是,汇率的灵活性不应该与充分的资本账户开放相混淆。

一个开放的资本帐户将允许汇率自由浮动并由市场决定。

即便资本帐户没有完全开放,利率仍然可以实现灵活,货币政策独立性目标仍然可以实现。

事实上,如上所述,为什么使资本帐户的进一步逐渐开放更合适,而不是汇率的灵活性。

资本账户的自由流动是一个有益的长期目标,但从短期来看没有

升级会员

升级会员