intermediate accountingfifteenth edition ch01.docx

《intermediate accountingfifteenth edition ch01.docx》由会员分享,可在线阅读,更多相关《intermediate accountingfifteenth edition ch01.docx(42页珍藏版)》请在冰豆网上搜索。

intermediateaccountingfifteentheditionch01

CHAPTER1

FinancialAccountingandAccountingStandards

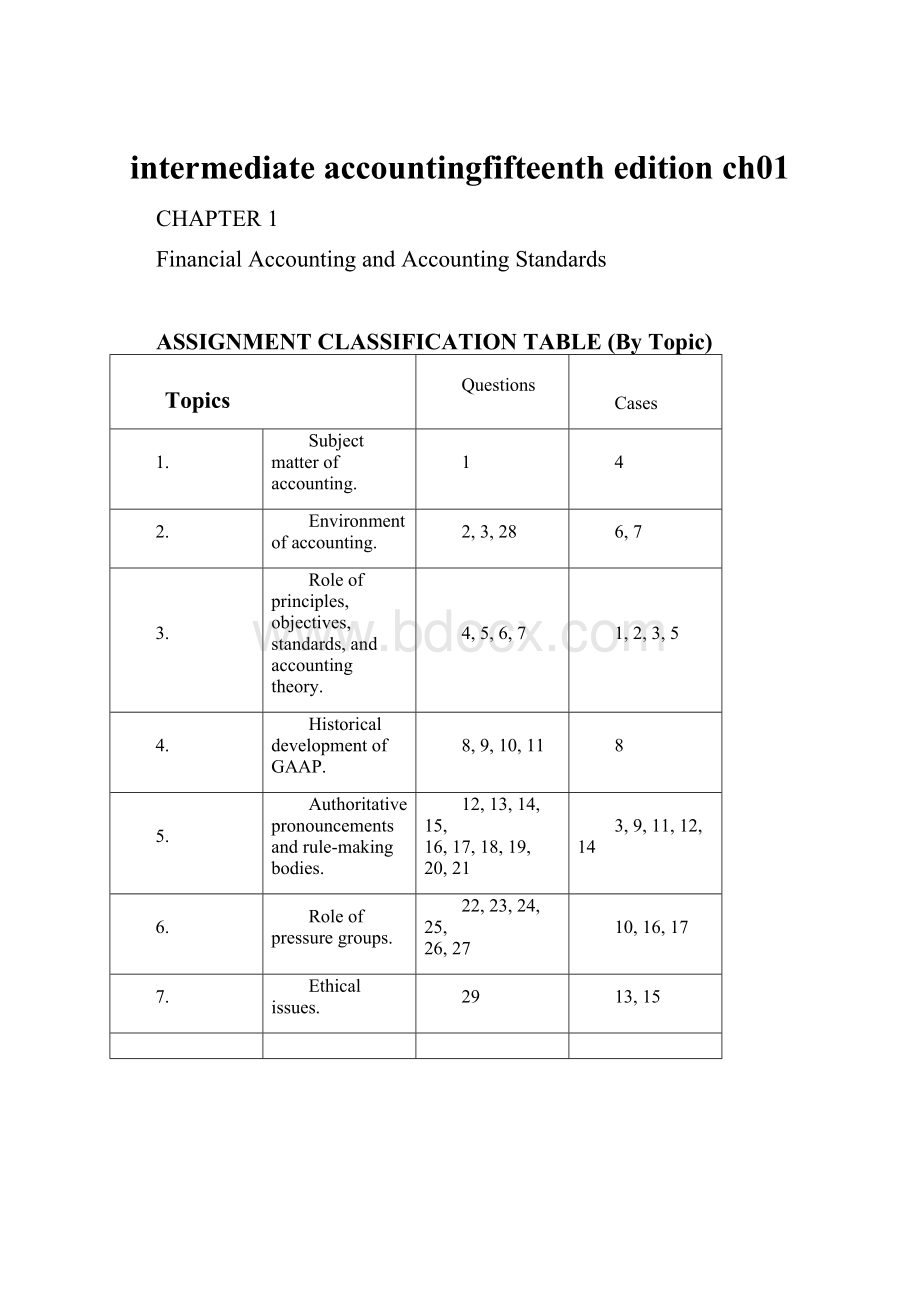

ASSIGNMENTCLASSIFICATIONTABLE(ByTopic)

Topics

Questions

Cases

1.

Subjectmatterofaccounting.

1

4

2.

Environmentofaccounting.

2,3,28

6,7

3.

Roleofprinciples,objectives,standards,andaccountingtheory.

4,5,6,7

1,2,3,5

4.

HistoricaldevelopmentofGAAP.

8,9,10,11

8

5.

Authoritativepronouncementsandrule-makingbodies.

12,13,14,15,

16,17,18,19,

20,21

3,9,11,12,14

6.

Roleofpressuregroups.

22,23,24,25,

26,27

10,16,17

7.

Ethicalissues.

29

13,15

ASSIGNMENTCLASSIFICATIONTABLE(ByLearningObjective)

LearningObjectives

Questions

Cases

1.

Identifythemajorfinancialstatementsandothermeansoffinancialreporting.

1,2

CA1-4,CA1-5

2.

Explainhowaccountingassistsintheefficientuseofscarceresources.

3,5

3.

Identifytheobjectiveoffinancialreporting.

4,7

CA1-2,CA1-3,CA1-4,CA1-5,CA1-6

4.

Explaintheneedforaccountingstandards.

6

CA1-3,CA1-7,CA1-9

5.

Identifythemajorpolicy-settingbodiesandtheirroleinthestandard-settingprocess.

8,9,10,11,13,14,15,16,19

CA1-1,CA1-2,CA1-3,CA1-7,CA1-8,CA1-9,CA1-11,CA1-14

6.

Explainthemeaningofgenerallyacceptedaccountingprinciples(GAAP)andtheroleofthecodificationforGAAP.

12,14,18,19,20,21

CA1-2,CA1-3,CA1-7,CA1-8,CA1-12

7.

Describetheimpactofusergroupsontherule-makingprocess.

17,22,23,24,25,26,27

CA1-10,CA1-11,CA1-13,CA1-16,CA1-17

8.

Describesomeofthechallengesfacingfinancialreporting.

28

9.

Understandissuesrelatedtoethicsandfinancialaccounting.

16,17,29

CA1-6,CA1-13,CA1-15

ASSIGNMENTCHARACTERISTICSTABLE

Item

Description

LevelofDifficulty

Time

(minutes)

CA1-1

FASBandstandard-setting.

Simple

15–20

CA1-2

GAAPandstandard-setting.

Simple

15–20

CA1-3

Financialreportingandaccountingstandards.

Simple

15–20

CA1-4

Financialaccounting.

Simple

15–20

CA1-5

Objectiveoffinancialreporting.

Moderate

20–25

CA1-6

Accountingnumbersandtheenvironment.

Simple

10–15

CA1-7

NeedforGAAP.

Simple

15–20

CA1-8

AICPA’sroleinrule-making.

Simple

20–25

CA1-9

FASBroleinrule-making.

Simple

20–25

CA1-10

PoliticalizationofGAAP.

Complex

30–40

CA1-11

ModelsforsettingGAAP.

Simple

15–20

CA1-12

GAAPterminology.

Moderate

30–40

CA1-13

Rule-makingIssues.

Complex

20–25

CA1-14

SecuritiesandExchangeCommission.

Moderate

30–40

CA1-15

Financialreportingpressures.

Moderate

25–35

CA1-16

Economicconsequences.

Moderate

25–35

CA1-17

GAAPandeconomicconsequences.

Moderate

25–35

SOLUTIONSTOCODIFICATIONEXERCISES

CE1-1

TheinformationatthislinkdescribestheelementsofferedinTheFASBAccountingStandardsCodification.Asindicated,thewebsiteoffersseveralresourcestoenhanceyourworkingknowledgeoftheCodificationandtheCodificationResearchSystem.ThispageincludeslinkstohelppageswhichdescribespecificfunctionsandfeaturesoftheCodification.Linkstofrequentlyaskedquestions,theFASBLearningGuide,andtheNoticetoConstituentsarealsoavailableonthispage.

Helppages

FAQ

LearningGuide

AbouttheCodification—NoticeofConstituents

CE1-2

ThefollowinginformationisprovidedattheProvidingFeedbacklink:

TheCodificationincludesafeaturewhichcanbeusedtosubmitcontent-relatedfeedbackorgeneral,system-relatedcomments.ThefeedbacksystemisnotdesignedforcommentsonproposedAccountingStandardsUpdates.

Content-relatedfeedback

AsaregistereduseroftheFASBAccountingStandardsCodificationResearchSystemwebsite,youareableandareencouragedtoprovidefeedback,attheparagraphlevel,totheFASBaboutanycontent-relatedmatters.ForspecificinformationabouttheCodificationandthefeedbackprocess,pleasereadtheNoticetoConstituents.

Toprovidecontent-relatedfeedback:

ClicktheSubmitfeedbackbuttonbeneaththeparagraphforwhichyouwanttoprovidefeedback.Enterorcopy/pasteyourcommentsinthetextbox.Notethatformatting(lists,bold,etc.)isnotretainedandthereisa4,000characterlimitonfeedbacksubmissions.

ClickSUBMIT.YourcommentsaresenttotheFASBandreviewedbyFASBstaff.Youcanalsosubmitmultiplecommentsforanygivenparagraph,if,forexample,youdeterminethatmoreinformationwouldbeusefultotheFASBstaff.

Generalfeedback

ClickheretoprovidegeneralfeedbackontheCodificationingeneral,theCodificationResearchSystemwebsite,andothersystem-relateditemsthatarenotcontentspecific.

CE1-3

The“What’sNew”pageprovideslinkstoCodificationcontentthathasbeenrecentlyissued.Duringtheverificationphase,updatesmayresultfromeithertheissuanceofCodificationupdateinstructionsthataccompanynewStandardsorfromchangestotheCodificationduetoincorporationofconstituentfeedback.

ANSWERSTOQUESTIONS

1.Financialaccountingmeasures,classifies,andsummarizesinreportformthoseactivitiesandthatinformationwhichrelatetotheenterpriseasawholeforusebypartiesbothinternalandexternaltoabusinessenterprise.Managerialaccountingalsomeasures,classifies,andsummarizesinreportformenterpriseactivities,butthecommunicationisfortheuseofinternal,managerialparties,andrelatesmoretosubsystemsoftheentity.Managerialaccountingismanagementdecisionorientedanddirectedmoretowardproductline,division,andprofitcenterreporting.

2.Financialstatementsgenerallyrefertothefourbasicfinancialstatements:

balancesheet,incomestatement,statementofcashflows,andstatementofchangesinowners’orstockholders’equity.Financialreportingisabroaderconcept;itincludesthebasicfinancialstatementsandanyothermeansofcommunicatingfinancialandeconomicdatatointerestedexternalparties.Examplesoffinancialreportingotherthanfinancialstatementsareannualreports,prospectuses,reportsfiledwiththegovernment,newsreleases,managementforecastsorplans,anddescriptionsofanenterprise’ssocialorenvironmentalimpact.

3.Ifacompany’sfinancialperformanceismeasuredaccurately,fairly,andonatimelybasis,therightmanagersandcompaniesareabletoattractinvestmentcapital.Toprovideunreliableandirrelevantinformationleadstopoorcapitalallocationwhichadverselyaffectsthesecuritiesmarket.

4.Theobjectiveofgeneralpurposefinancialreportingistoprovidefinancialinformationaboutthereportingentitythatisusefultopresentandpotentialequityinvestors,lenders,andothercreditorsindecisionsaboutprovidingresourcestotheentitythroughequityinvestmentsandloansorotherformsofcredit.Informationthatisdecision-usefultocapitalproviders(investors)mayalsobeusefultootherusersoffinancialreportingwhoarenotinvestors.

5.Investorsareinterestedinfinancialreportingbecauseitprovidesinformationthatisusefulformakingdecisions(referredtoasthedecision-usefulnessapproach).Whenmakingthesedecisions,investorsareinterestedinassessingthecompany’s

(1)abilitytogeneratenetcashinflowsand

(2)management’sabilitytoprotectandenhancethecapitalproviders’investments.Financialreportingshouldthereforehelpinvestorsassesstheamounts,timing,anduncertaintyofprospectivecashinflowsfromdividendsorinterest,andtheproceedsfromthesale,redemption,ormaturityofsecuritiesorloans.Inorderforinvestorstomaketheseassessments,theeconomicresourcesofanenterprise,theclaimstothoseresources,andthechangesinthemmustbeunderstood.

6.Acommonsetofstandardsappliedbyallbusinessesandentitiesprovidesfinancialstatementswhicharereasonablycomparable.Withoutacommonsetofstandards,eachenterprisecould,andwould,developitsowntheorystructureandsetofpractices,resultinginnoncomparabilityamongenterprises.

7.General-purposefinancialstatementsarenotlikelytosatisfythespecificneedsofallinterestedparties.Sincetheneedsofinterestedpartiessuchascreditors,managers,owners,governmentalagencies,andfinancialanalystsvaryconsiderably,itisunlikelythatonesetoffinancialstatementsisequallyappropriateforthesevarieduses.

QuestionsChapter1(Continued)

8.TheSEChasthepowertoprescribe,inwhateverdetailitdesires,theaccountingpracticesandprinciplestobeemployedbythecompaniesthatfallwithinitsjurisdiction.BecausetheSECreceivesauditedfinancialstatementsfromnearlyallcompaniesthatissuesecuritiestothepublicorarelistedonthestockexchanges,itisgreatlyinterestedinthecontent,accuracy,andcredibilityofthestatements.FormanyyearstheSECreliedontheAICPAtoregulatetheprofessionanddevelopandenforceaccountingprinciples.Lately,theSEChasassumedamoreactiveroleinthedevelop-mentofaccountingstandards,especiallyintheareaofdisclosurerequirements.InDecember1973,inASRNo.150,theSECsaidtheFASB’sstatementswouldbepresumedtocarrysubstantialauthoritativesupportandanythingcontrarytothemtolacksuchsupport.Ittherebysupportsthedevelopmentofaccountingprinciplesintheprivatesector.

9.TheCommitteeonAccountingProcedurewasaspecialcommitteeoftheAmericanInstituteofCPAsthat,betweentheyearsof1939and1959,issued51AccountingResearchBulletinsdealingwithawidevarietyoftimelyaccountingproblems.Thesebulletinsprovidedsolutionstoimmediateproblemsandnarrowedtherangeofalternativepractices.But,theCommittee’sproblem-by-problemapproachfailedtoprovideawell-definedand

升级会员

升级会员