王关富商务英语阅读第二版参考译文chapter10.docx

《王关富商务英语阅读第二版参考译文chapter10.docx》由会员分享,可在线阅读,更多相关《王关富商务英语阅读第二版参考译文chapter10.docx(14页珍藏版)》请在冰豆网上搜索。

王关富商务英语阅读第二版参考译文chapter10

U10

Thealchemistsoffinance

金融魔法点石成金

May17th2007

FromTheEconomistprintedition

(本文由ECO论坛dtchengxc翻译,原文版权归经济学人集团(TheEconomistNewspaperLimited)所有,译文版权归译者所有,XX,不得转载,谢谢合作!

)

漫画作者玛丽亚•吉夫斯(MariaJeeves)

Globalinvestmentbanksaretakingevermorerisk,andaredevisingevermoresophisticatedwaysofspreadingit,saysHenryTricks.Isthatreassuringorworrying?

亨利•特里克斯(HenryTricks)说:

“全球的投资银行正承受着越来越大的风险,也在设计着越来越复杂的分散风险的方法。

”这究竟是会让人放心还是让人担心?

ATLEASTsince1823,whenByron'sDonJuandescribed“JewRothschild,andhisfellowChristianBaring”asthe“trueLordsofEurope”,investmentbankershaveinspiredawe,envyand,rightlyorwrongly,ameasureofdisdain.Exactly100yearsagotheundisputedpatriarchofthemodernindustry,J.PierpontMorgan,stemmedthePanicof1907,afinancialcrisiscausedbyunregulatedtrusts(thehedgefundsoftheirday).Acting,ineffect,aslenderoflastresortfromhisWallStreetoffice,hewasbrieflyfetedbeforeAmericansrealisedthedangerofhavingsuchpowervestedinoneman.Cartooniststhenmercilesslymockedhim.Afterhisdeathin1913theFederalReservewassetup.

不晚于1823年——那时拜伦(Byron)在《唐璜》(DonJuan)中将“犹太人罗思柴尔德(Rothschild)和他的同伙基督徒巴林(Baring)”称为“欧洲真正的主宰”,投资银行家们博得了敬畏、羡慕以及一定程度的蔑视——不管这正确与否。

正好100年前这个现代产业无可争议的鼻祖J•皮尔庞特•摩根(J.PierpontMorgan)制止了1907年的大恐慌(thePanicof1907)——一场由非受监管信托(unregulatedtrusts)(当时的对冲基金(hedgefunds))引起的金融危机。

他在其华尔街的办公室中充当了实际上的最后贷款人的角色,受到了人们的追捧。

其后不久,美国人意识到让一个人拥有如此的权力是多么的危险。

当时的漫画家对他进行了无情的嘲弄。

在他1913年死后,美联储(theFederalReserve)就成立了。

Theinvestment-bankingindustrywasfurtherconstrainedduringtheDepressionofthe1930s,whenWallStreetfirmssuchasthatfoundedbyMorganweresplitintocommercialbanksandsecuritieshouses.Thelatter—today'sinvestmentbanks—underwritestocksandbondsandadvisecompaniesonmergersandacquisitions,ratherthancollectdepositsandmakeloans.Inthe1980sand1990stheydevelopedareputationforgluttonousexcess.Butalothaschangedsincethen.

在上个世纪30年代的大萧条(theDepressionofthe1930s)期间投资银行业受到进一步的抑制,华尔街的许多公司(比方说摩根创立的公司)被拆分为商业银行和证券交易所。

后者即今天的投资银行,它承销股票和债券,并就企业合并和收购事宜为公司提供咨询服务,而不经营存、贷款业务。

在上个世纪80和90年代它们得到了过于贪婪的名声。

但从那时以来情况发生了很大的变化。

Intenselyprivatepartnershipshavebecomepubliclytradedcompanies.CommercialbankssuchasCitigroupandJPMorganChasehavemuscledbackintoinvestmentbanking.AndEuropeanwarhorsessuchasDeutscheBank,UBSandCreditSuissehavejoinedtheraceforglobalsupremacy.Thebets,andtheprofits,havegotbigger,thoughinvestmentbanksaretryingtokeepquietaboutthat,forseveralreasons.

很大程度上私人合伙公司已经可以公开交易。

诸如花旗集团(Citigroup)、摩根大通(JPMorganChase)这样的商业银行又挤回了投资银行业。

欧洲老字号如:

德意志银行(DeutscheBank)、瑞银集团(UBS)、瑞士信贷(CreditSuisse),也加入了争夺全球霸权的竞争。

虽然投资银行基于几点理由试图对此保持沉默,赌注和收益却已越来越大。

First,theyareundermorescrutiny.WallStreetfirmshadtheirwingsclippedbyEliotSpitzer,NewYork'sformerattorney-general,forpluggingworthlesssharesduringthedotcomera.Beingpubliclytradedcompanieshastamedsomeegos,too.Startradersdonotenjoythesameheadroomonsalaries(albeitverylargesalaries)astheydidwhentheywerepartnersinthebusiness.AtUBS,aSwissbankwhichin2000movedintotheAmericanequitymarketsbymergingwithPaineWebber,abrokerage,“fiefs”areexplicitlybanned.RichardFuld,bossofLehmanBrothers,afast-growingWallStreetfirm,imposeda“one-firmculture”whenitwasspunofffromAmericanExpressin1994.Now,saysScottFreidheim,atopexecutive,MrFulduses“culture”inspeechesmoreoftenthananyotherwordexcept“the”.

首先,它们受到了更多的审查。

华尔街的公司被纽约州前总检察长艾略特•斯皮策(EliotSpitzer)捆住了手脚,起因是这些公司在.com时代推广垃圾股票。

成为可公开交易的公司也挫伤了些许自尊心。

尽管交易明星们的薪水仍然很高,但薪水的上升空间与他们作为业务合伙人时相比逊色不少。

瑞银集团(UBS)是一家瑞士银行,在2000年通过与经纪公司普惠(PaineWebber)合并而进入美国股票市场。

在瑞银集团,“封地”是被明确禁止的。

莱曼兄弟公司(LehmanBrothers)是华尔街一家快速成长的公司,当它在1994年从美国运通公司(AmericanExpress)分割出来时,其老板理查德•富尔德(RichardFuld)就强制推行“公司一体统筹的文化”。

斯科特•弗赖德海姆(ScottFreidheim)是一个高层管理人员,他说现在富尔德先生在演讲中使用“文化”这个词的频率比除了“the”之外的所有单词都要高。

Meanwhileanothergrouphasovertakentheinvestmentbanksintheexcessstakes:

theirmoney-spinningclientsintheprivate-equityandhedge-fundindustries.Alreadytheythrowthebiggestparties,dotheboldestdealsandlaunchthemostcelebratedinitialpublicofferings.TheIPOofpartofBlackstone,aprivate-equitygroup,mightwellraisemoremoneythanGoldmanSachs'sdidin1999,wheneventhecompany'sdoormenanddriversbecameextremelyrich.

同时,要说到过分,另一个群体已经超过了投资银行:

它们在私募股权和对冲基金业赚大钱的客户。

他们已经举行了最大规模的派对,进行了最大胆的交易,发起了最著名的首次公开招股(IPO,initialpublicoffering)。

黑石(Blackstone)是一家私募股权集团,其部分的首次公开招股所筹集的资金甚至超过高盛公司(GoldmanSachs)在1999年全年的业绩——那时即使是高盛公司的门卫和司机都赚得盆满钵满。

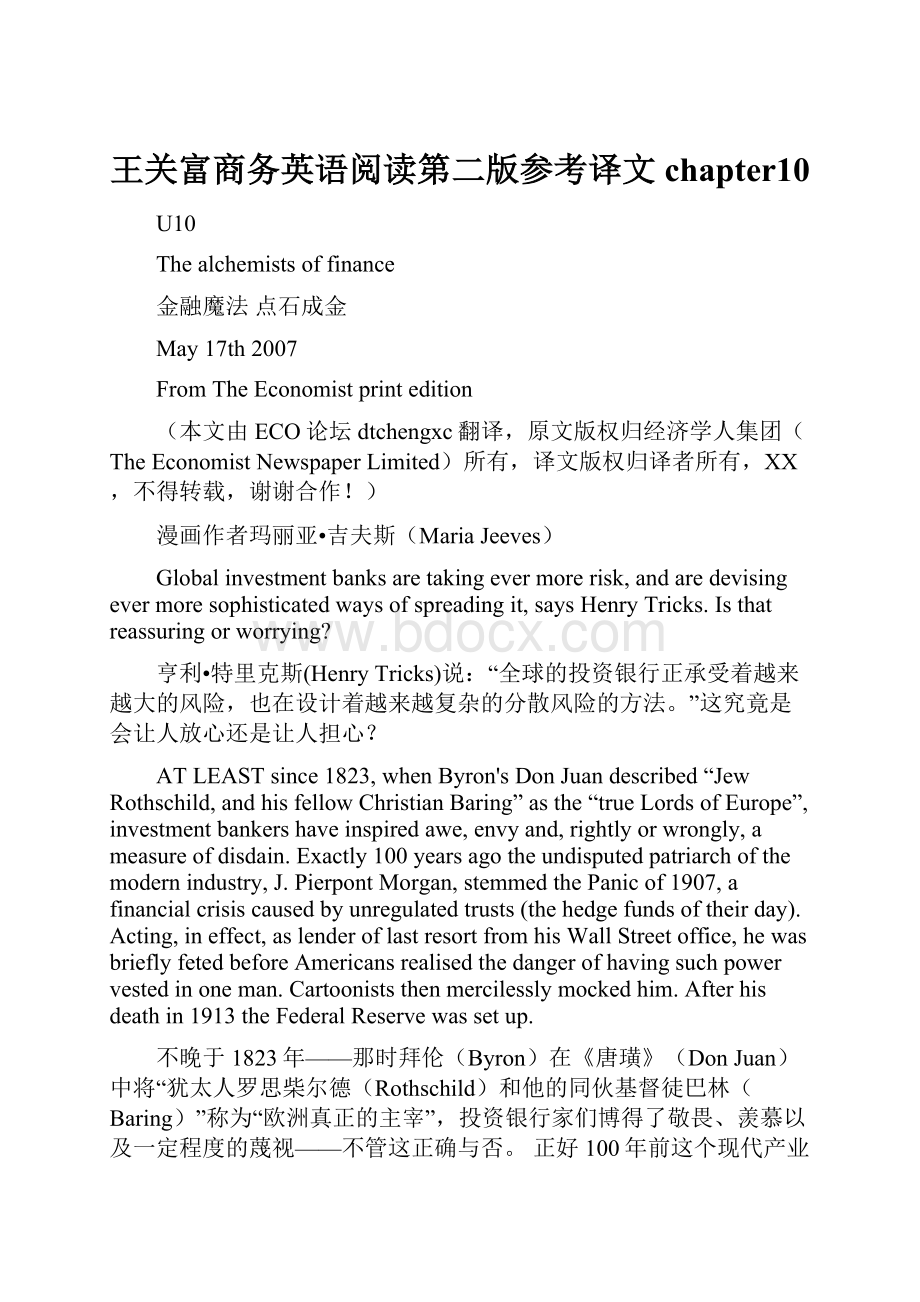

(图表说明:

Richlist财富榜

Investment-bankingrevenue,byactivity投资银行收入,按活动分类

2006,$bn年度:

2006年,单位:

十亿美元

Advisory咨询业务Debtunderwriting债务承销业务Equityunderwriting股票承销业务

GoldmanSachs高盛

MorganStanley摩根士丹利

JPMorgan摩根大通银行

CreditSuisse*瑞士信贷*

Citigroup花旗集团

MerrillLynch美林

DeutscheBank德意志银行

LehmanBrothers莱曼兄弟公司

BankofAmerica美国银行

*Annualisedusing01-03以2001-2003年的收入折算年度收入

Source:

DominionBondRatingService资料来源:

多美年债券评级服务公司)

Yetwheninvestmentbankersdiscussthefabulousfortunesaccruingtothesefirms'founders,theydosowithoutenvy.“Theirsisatrulypioneeringrole,”saysAnshuJain,headofglobalmarketsatDeutscheBank,oneoftheworld'stoptradingbanks.“Pioneersinanyindustrygetadisproportionateshareofthespoils.”

但当投资银行家们谈到这些公司创始人所积累的巨大财富时,他们一点也不嫉妒。

德意志银行(DeutscheBank)是世界顶级的贸易银行之一,其全球市场业务总裁安苏•贾殷(AnshuJain)说:

“他们扮演的是一个真正的先驱者的角色,任何行业的先驱者都会得到一份不成比例的战利品。

”

Eveniftheyarenolongerthepioneers,theinvestmentbankshaveplayedacrucialpartinbringingabouttheextraordinarychangesseeninthefinancialmarkets,startinginthe1980sandacceleratingdramaticallyinthepastfiveyears.Technologyandinnovationhavebroughtunprecedentedbreadth,depthandrichnesstofinancialinstruments.AccordingtoMcKinsey,aconsultancy,thestockofsharesandpublicandprivatedebtsecuritiesheldinAmericagrewfrom2.4timesGDPin1995to3.3timesin2004.InEuropetheincreasewasevenmoredramatic,albeitfromalowerbase.Thesefiguresdonotincludederivatives,notionalamountsofwhichtradedprivately,or“over-the-counter”securities,whichhadsoaredto$370trillionbylastJune,from$258trillionlessthantwoyearsearlier,accordingtotheBankforInternationalSettlements(BIS).Givensuchtorridgrowth,themarketsarebecomingincreasinglyvitaltoglobalfinancialstability.

投资银行即使不再是先驱者,它们在给金融市场带来显著变化的过程中仍然扮演着至关重要的角色。

这种变化始于上世纪80年代,在过去的5年里明显加速。

技术和创新使得金融工具的广度、深度和多样性达到了前所未有的水平。

根据麦肯锡(McKinsey)(一家咨询公司)的研究,美国人持有的股票和公私债券的存量在1995年是国内生产总值的2.4倍,而到了2004年则达到3.3倍。

而在欧洲,尽管起点较低,但增长的速度更快。

这些数字还不包括金融衍生品或是场外交易证券。

金融衍生品的名义金额在私下交易。

而根据国际结算银行(BankforInternationalSettlements,BIS)的报告,场外交易证券的交易金额从不到两年前的258万亿美元飙升到去年6月的370万亿美元。

鉴于市场如此快速的发展,它们对全球金融稳定愈加重要。

Therehavebeenthrillsandspillsalongtheway.Thestockmarketcrashof1987andtheseizingupofcreditmarketsafterRussiadefaultedin1998bothexposedhugeflawsintheindustry,forcingcentralbankstostepintopreventwhattheyfearedmightbelastingdamagetotherealeconomy.Evenso,regulatorsreckonthatonbalancethegrowthofmarketshasbeenagoodthing,makingthefinancialsystemsaferthanmoretraditionalformsofbanklending.Thetroubleisthatgiventhecomplexityofthenewinstrumentsandtherangeofclientsandcountriesinvolved,theycanneverbeabsolutelysurethatamonumentalcrisisisnotbrewingsomewhere.

这一路上充满了紧张刺激。

1987年的股市崩溃和1998年俄罗斯拒绝履行偿债义务后信贷市场的停摆都暴露了该行业的巨大缺陷。

这促使中央银行进行干涉,以避免可能对实际经济造成的持久伤害。

虽然如此,监管机构还是认为市场的成长使得金融系统比传统的银行贷款形式更加安全了,总的说来是一件好事。

问题就在于:

考虑到新工具的复杂性以及所涉及客户和国家的范围,监管者永远不可能绝对保证任何地方都没有酝酿中的巨大危机。

Whatworriesbothbankersandregulatorsisnotsomuchthethreatfromhedgefundsorprivate-equitygroupsbuttheimplicationsforthefinancialsystemofapossiblecollapseofaninvestmentbank(orlargecomplexfinancialinstitution,astheyclumsilycallit).AtatimewhenAmerica'shousingmarkethasexposedthedangerofoverexcitementonWallStreet,itisworthexploringhowtheseinstitutionsareevolving,howtheyhandletherisksattachedtowhattheydo,andhowwellthoserisksarespreadaroundthefinancialsystem.Thatiswhatthissurveysetsouttodo.

让银行家和监管者担心的还不仅仅是来自对冲基金或私募股权集团的威胁,还有带有投资银行(或者按照他们的笨拙叫法:

大而复杂的金融机构)崩溃可能的金融系统的可能影响。

每当美国的房地产市场暴露出华尔街过度兴奋的危险时,如下这些问题就是值得探究的:

这些机构是如何发展的?

它们如何处理自身行为所带的风险?

能否很好的在金融系统中分散风险?

这就是本期调查报告准备讨论的问题。

Risk-takersAnonymous

匿名赌徒

Investmentbankingisinastateofevolutionratherthanrevolution.Theessenceofthebusinesshasalwaysbeentakingcalculated(andsometimesmiscalculated)risks.Butnowtradersplacebetsinmoreplaces,withmoreclientsandusingmorecomplicatedgamblingdevicesthaneverbefore.

投资银行业正处在稳步的发展之中,而不可能发生革命性的变化。

一直以来,该行业的本质就是要冒可预料(有时不可预料)的风险。

但现在交易者让赌注更加分散、客户更多、使用的赌博策略也比以往任何时候都要复杂。

Brokerageusedtobedescribedasahaulagebusiness,luggingmoney,asamemberoftheRothschilddynastyonceputit,“frompointA,whereitis,topointB,whereitisneeded”.TheideaofdescribingthemselvesasglorifieddeliverymenmaywellstillappealtothecynicsonthetradingfloorwhoworkwithshirtsleevesrolledupandhaileachotherloudlyinBrooklynormockcockneyaccents.Butanyhaulagefirmwouldbeflabbergastedbythetradingprofitsandreturnsonequityseenininvestmentbankinginrecentyears,especiallyamongWallStreet'sbig“bulge-bracket”firms.SvilenIvanov,headofcapitalmarketsatBostonConsultingGroup,notesthatearningsfromcapital-market-relatedactivitiesatthetoptenglobalinvestmentbankshaverisenbyalmosttwo-thirdsintwoyears,from$55billionin2004to$90billionlastyear.ThatsortofprofitincreaseiscomparablewithApple'srewardsforinventingtheiPod,hepointsout.Yetininvestmentbankingthereisnothingnearlyso

升级会员

升级会员